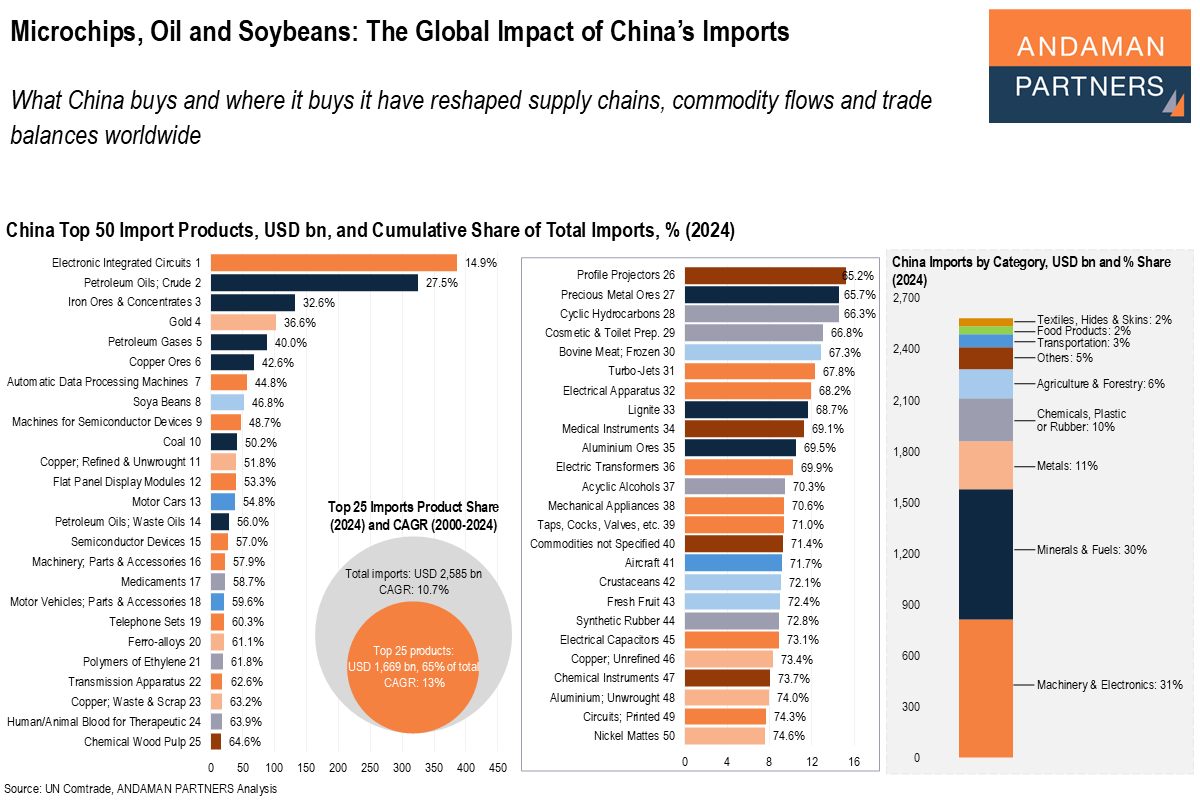

Microchips, Oil and Soybeans: The Global Impact of China’s Imports

What China buys and where it buys it have reshaped supply chains, commodity flows and trade balances worldwide.

What China buys and where it buys it have reshaped supply chains, commodity flows and trade balances worldwide.

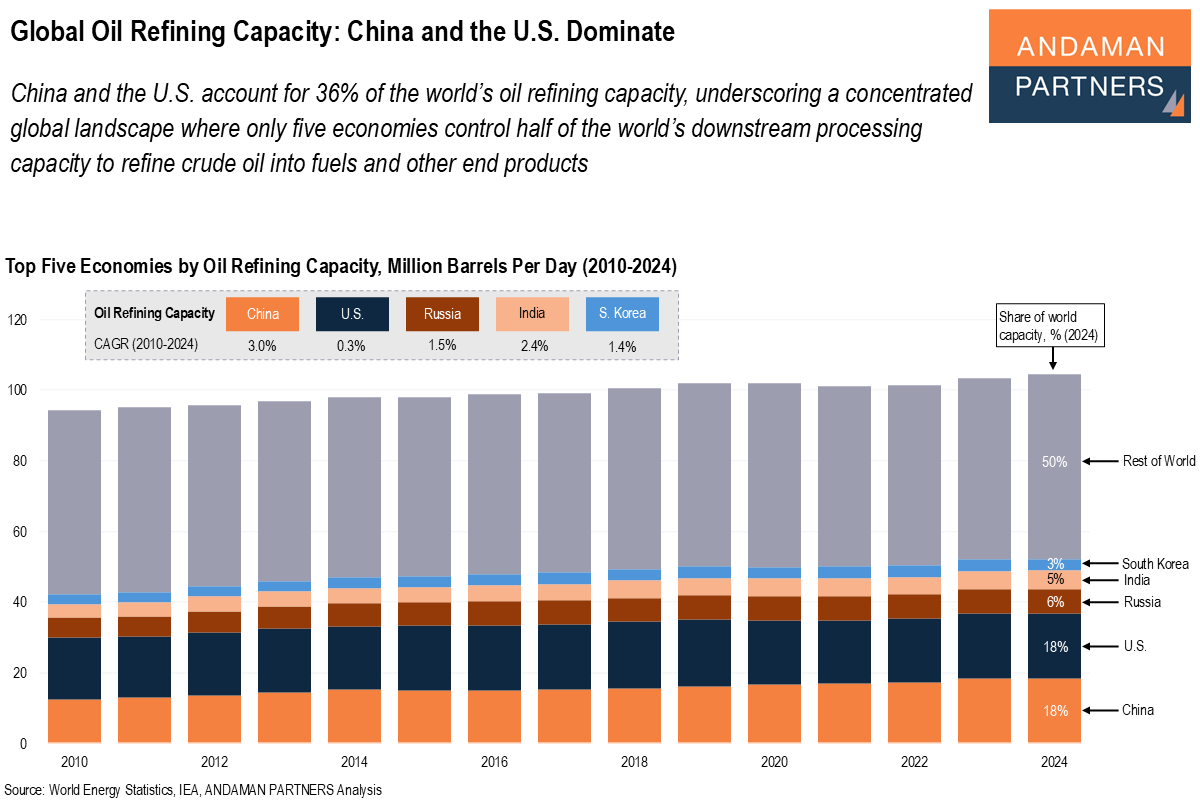

China and the U.S. account for 36% of the world’s oil refining capacity, and only five economies control half of the world’s capacity.

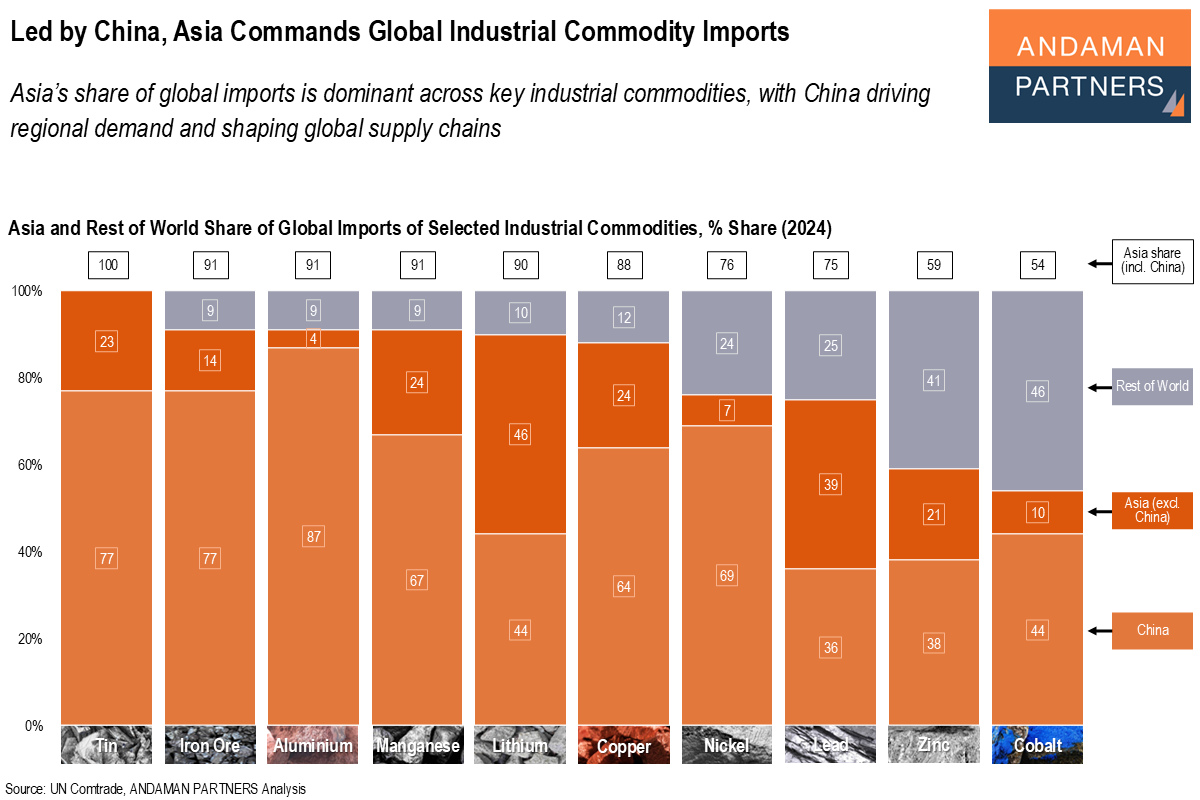

Asia’s share of global imports is dominant across key industrial commodities, with China driving regional demand and shaping global supply chains.

ANDAMAN PARTNERS maps the global metals trade, where a handful of countries dominate and China sits at the centre.

China is the world’s largest consumer of energy and runs large trade deficits for primary fuels, especially crude oil and petroleum gases.

Size and speed: Who buys the most from China, who sells the most to China and whose trade is growing the fastest?

Energy, mobility and industrial equipment—led by imports from China and strong U.S. supply—underpin Chile’s industrial and consumer economy.

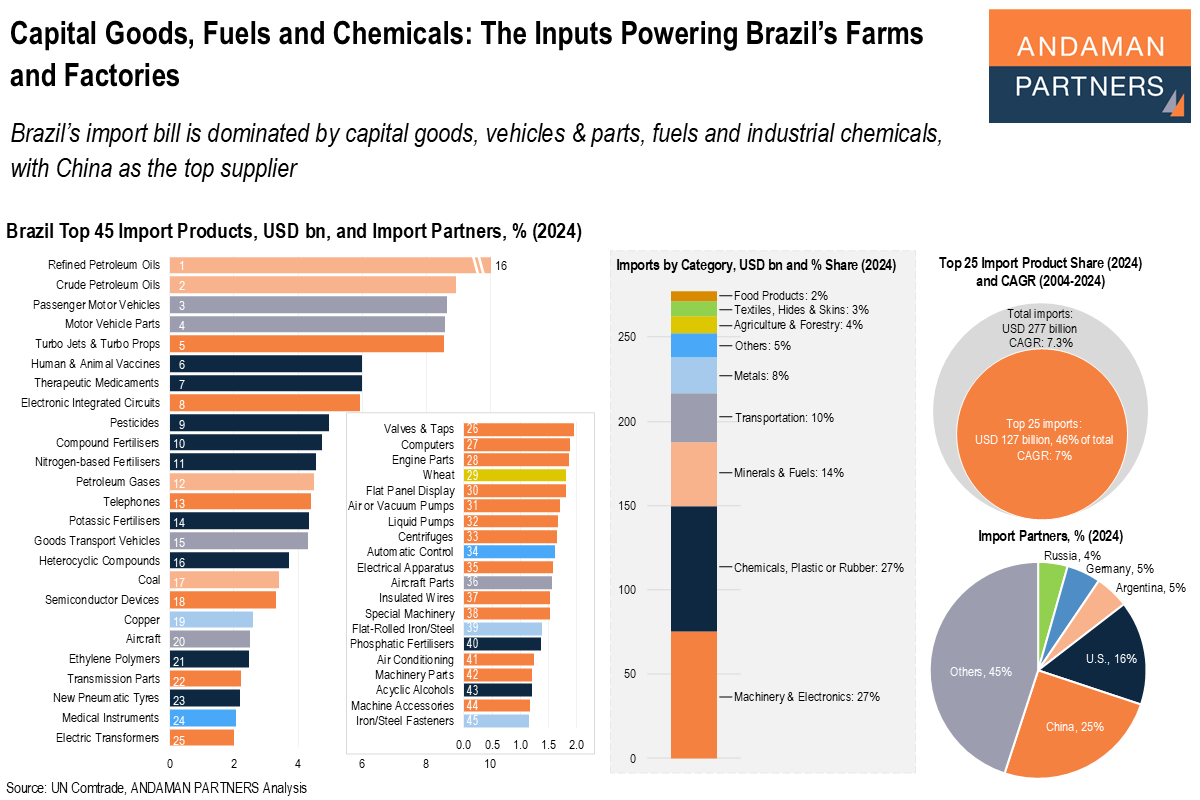

Brazil’s import bill is dominated by capital goods, vehicles & parts, fuels and industrial chemicals, with China as the top supplier.

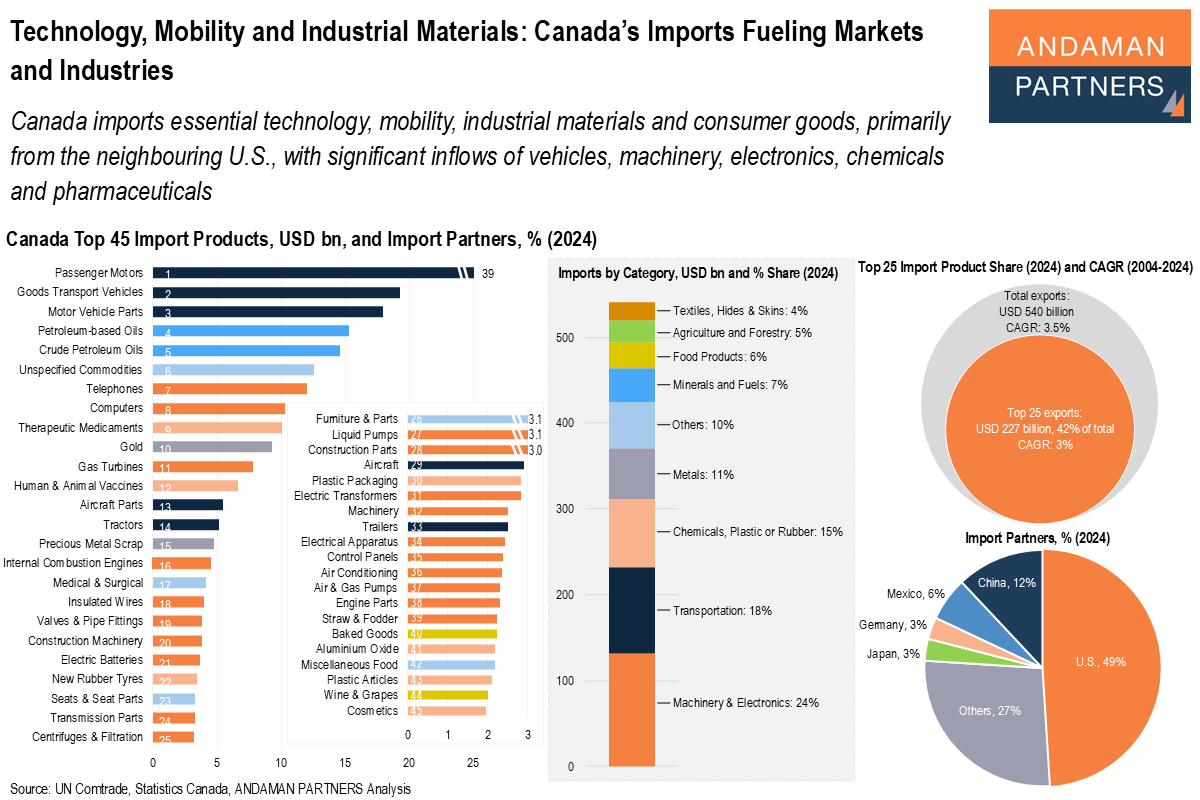

Canada imports essential technology, mobility, industrial materials and consumer goods, primarily from the neighbouring U.S.

Global trade is a mirror reflection of trade surplus economies supplying raw materials and goods, and trade deficit economies absorbing them to drive growth and consumption.