Country Profile – Indonesia

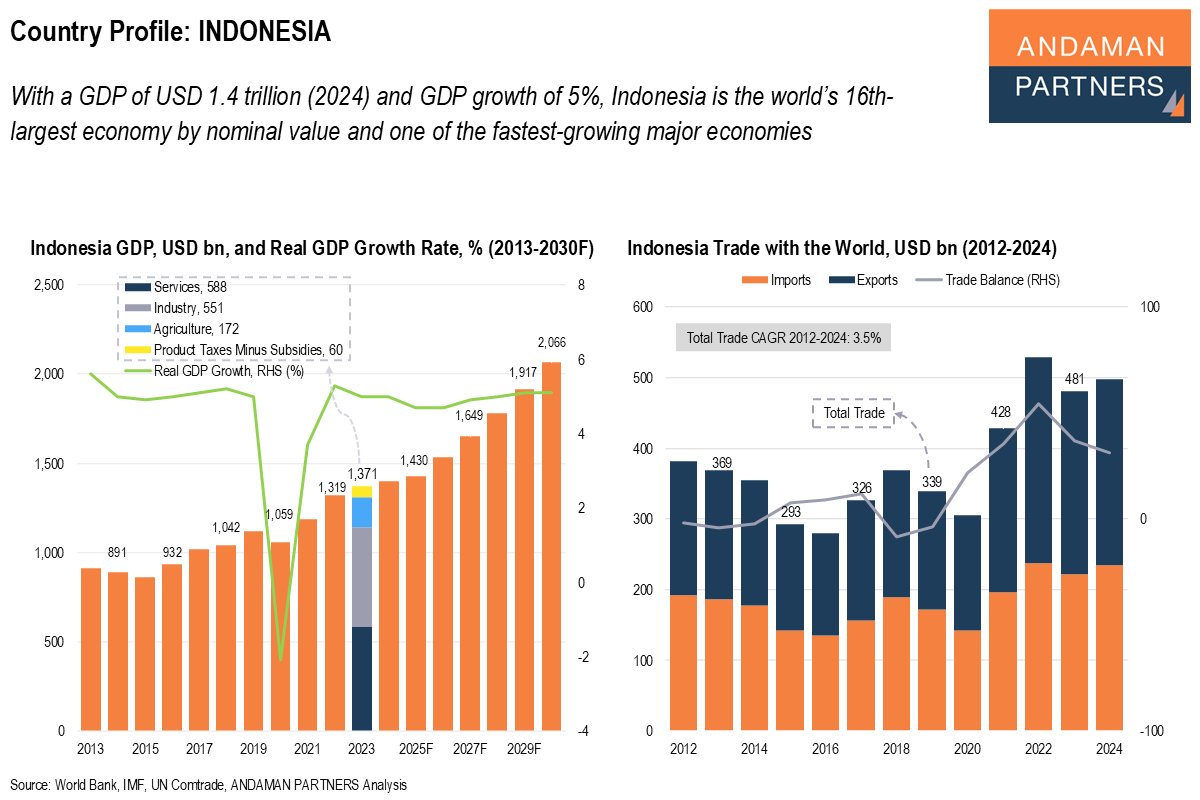

Indonesia has a USD 1.4 trillion economy (2024) and real GDP growth of 5%.

Indonesia has a USD 1.4 trillion economy (2024) and real GDP growth of 5%.

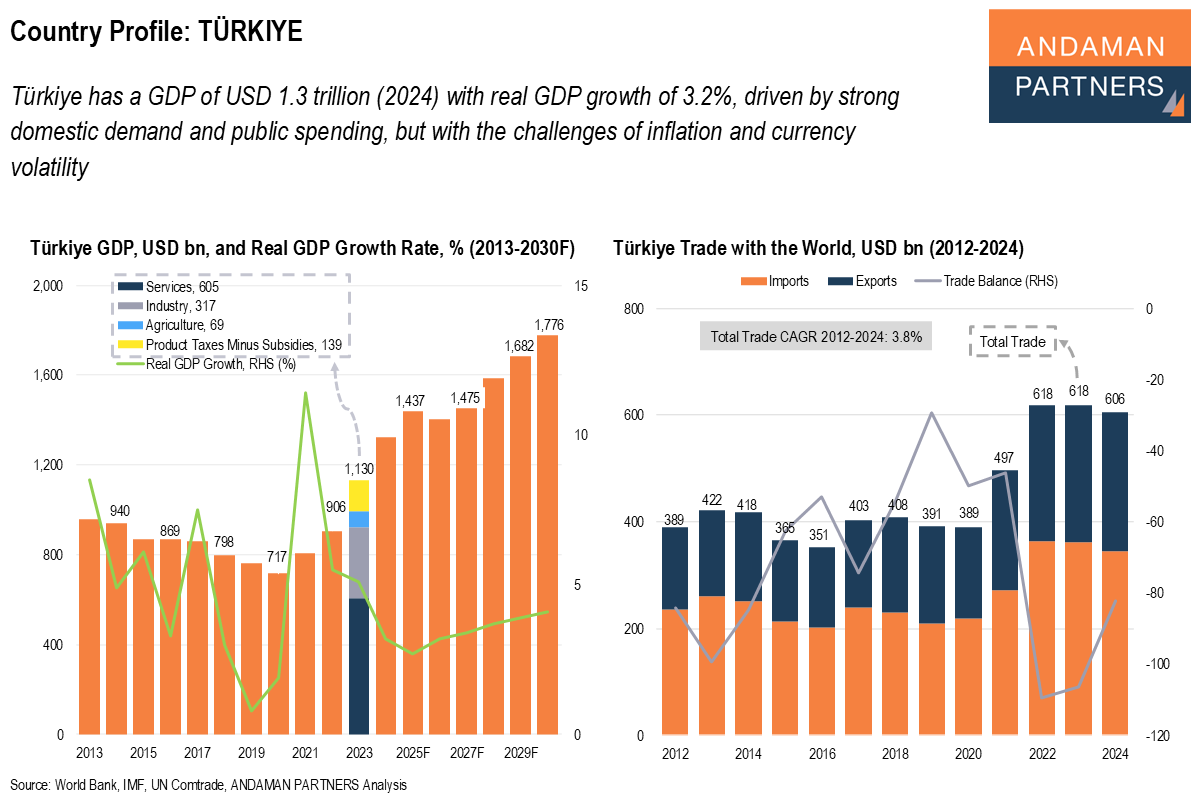

Türkiye has a GDP of USD 1.3 trillion (2024) with real GDP growth of 3.2%.

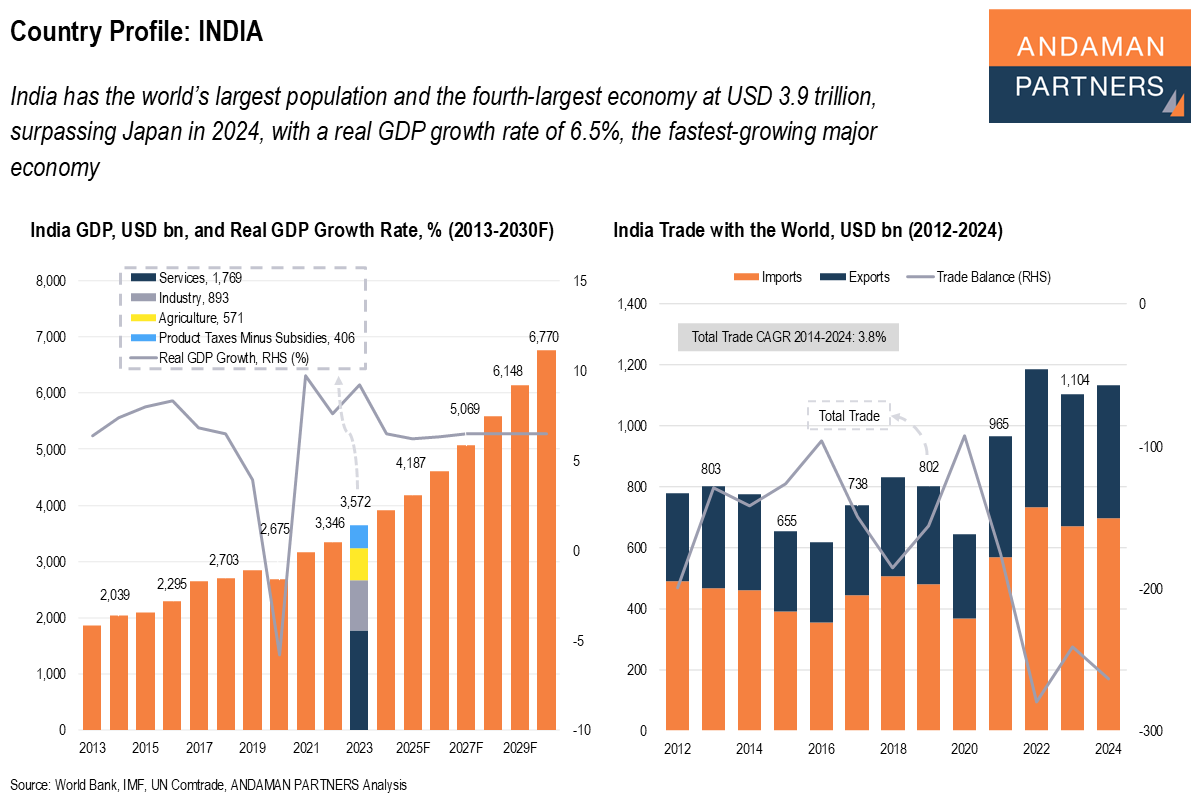

The world’s largest population and the fourth-largest economy at USD 3.9 trillion, surpassing Japan in 2024.

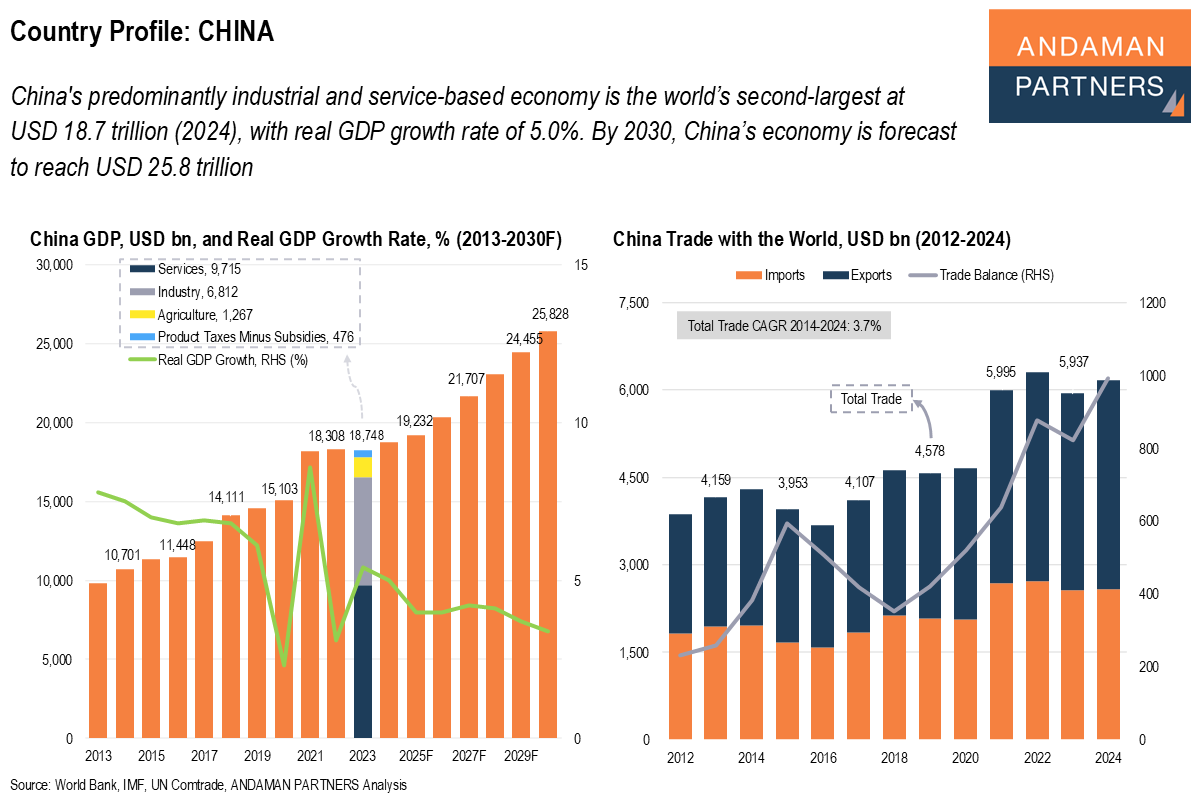

The world’s second-largest economy at USD 18.7 trillion (2024) and largest exporter.

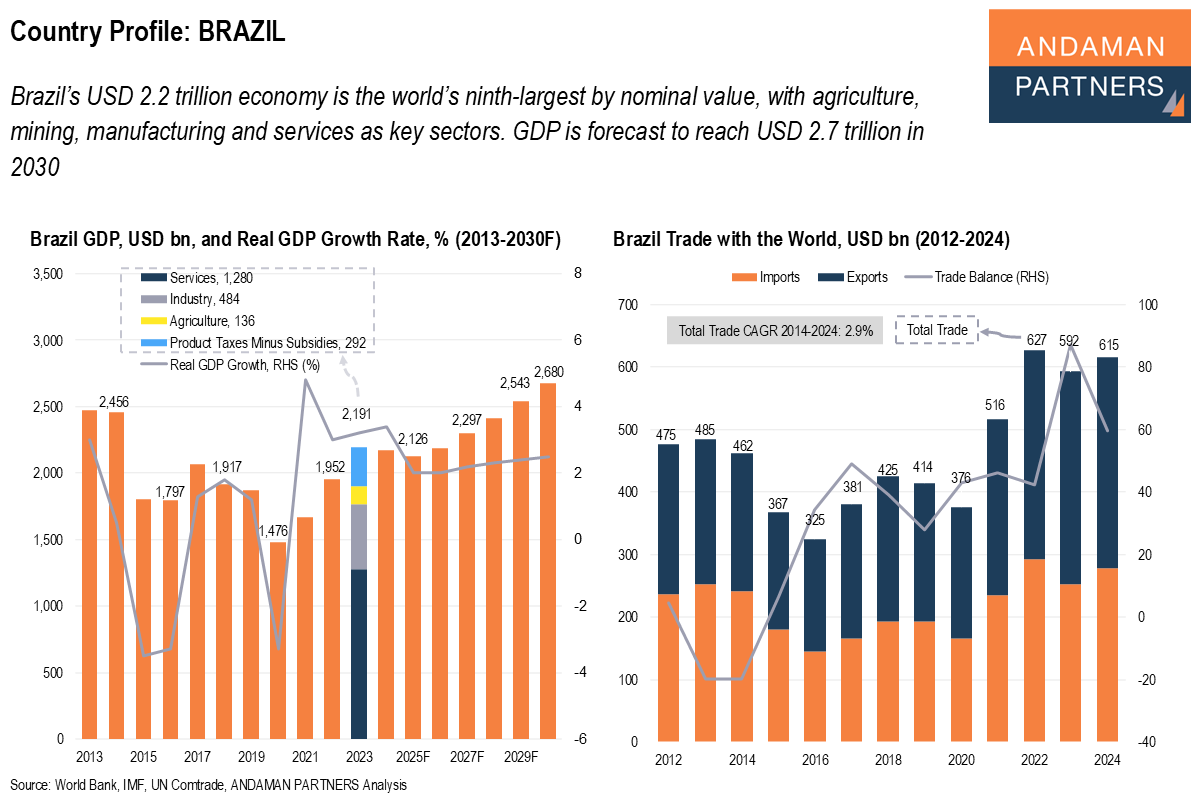

The world’s ninth-largest economy at USD 2.2 billion (2024); major agricultural goods and minerals exporter.

The total value of global agricultural exports in 2023 was USD 1.91 trillion, accounting for 8% of global merchandise trade. ANDAMAN PARTNERS presents a visualisation of global agricultural trade.

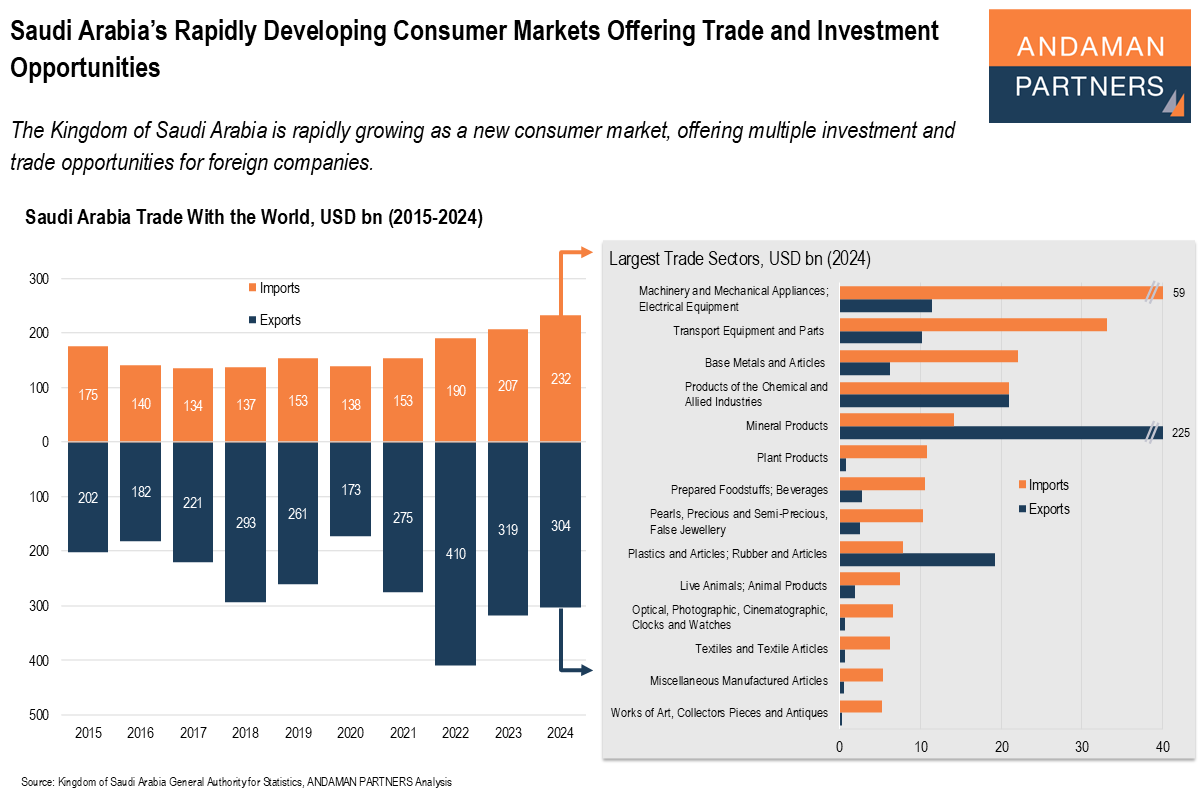

The Kingdom of Saudi Arabia's economy is undergoing government reform to diversify from a dependency on oil revenue, with vast investment devoted to developing a range of new industries.

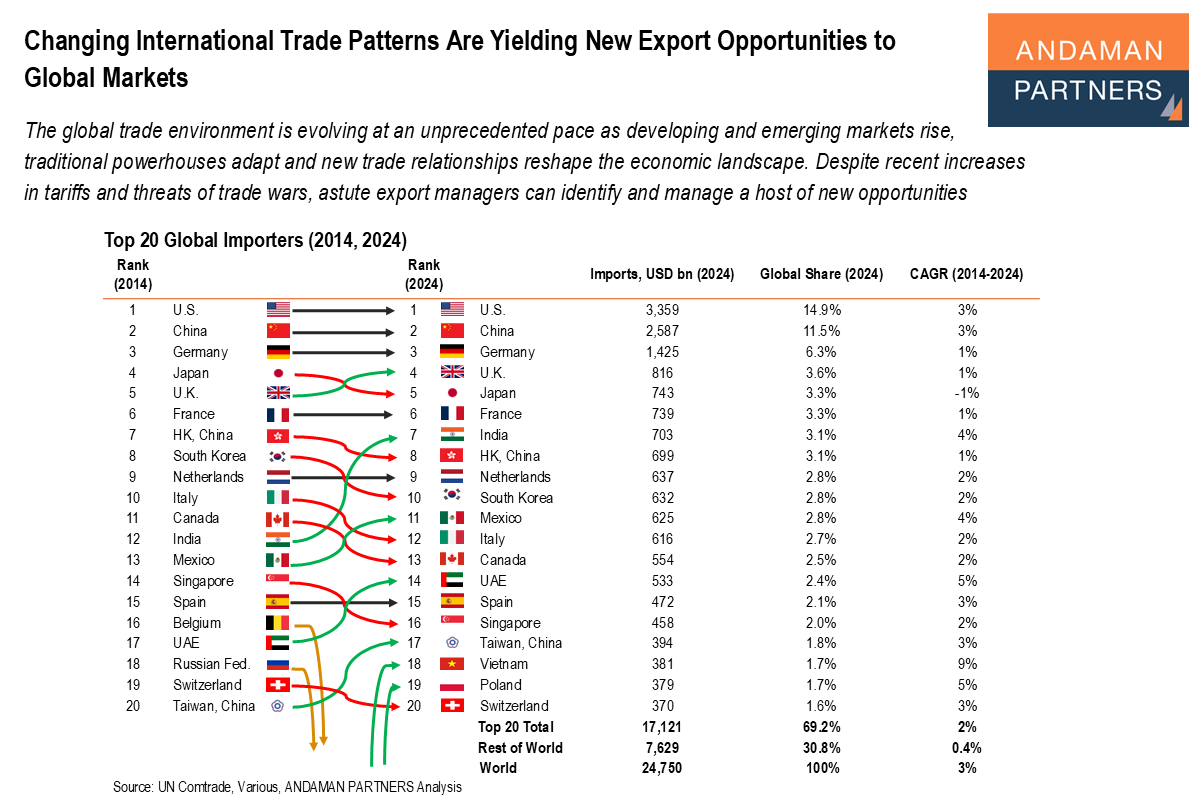

The global trade environment is evolving at an unprecedented pace. Astute export managers must identify and manage a host of new opportunities.

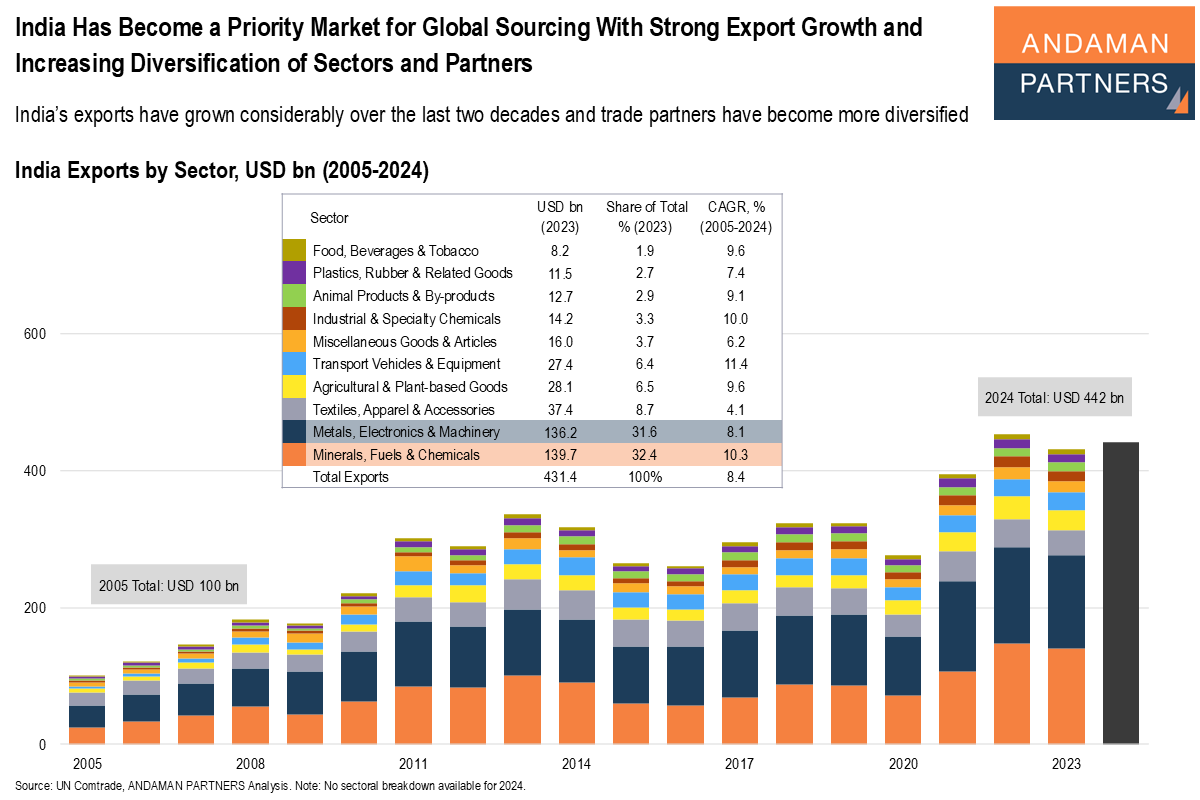

India’s export ecosystem will continue to grow and diversify, positioning the country for further export-driven economic expansion in the coming years.