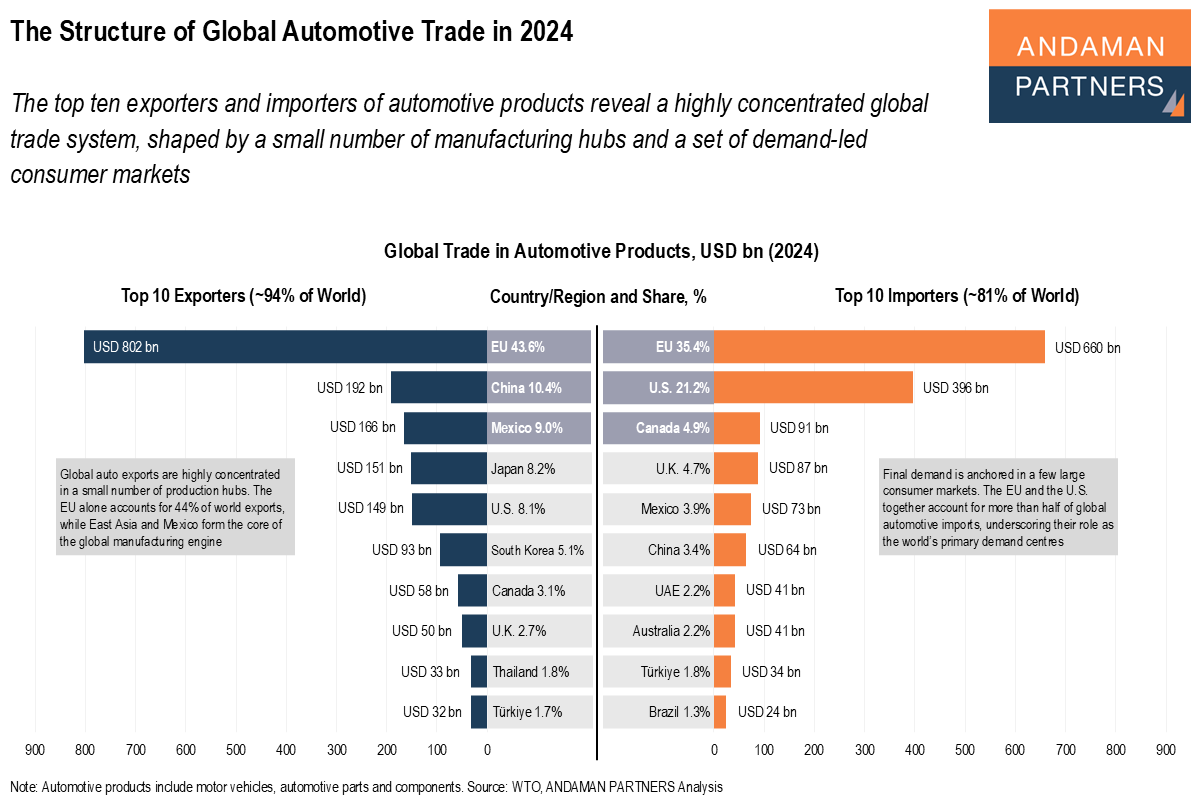

The Structure of Global Automotive Trade in 2024

The top ten exporters and importers of automotive products reveal a highly concentrated global trade system.

The top ten exporters and importers of automotive products reveal a highly concentrated global trade system.

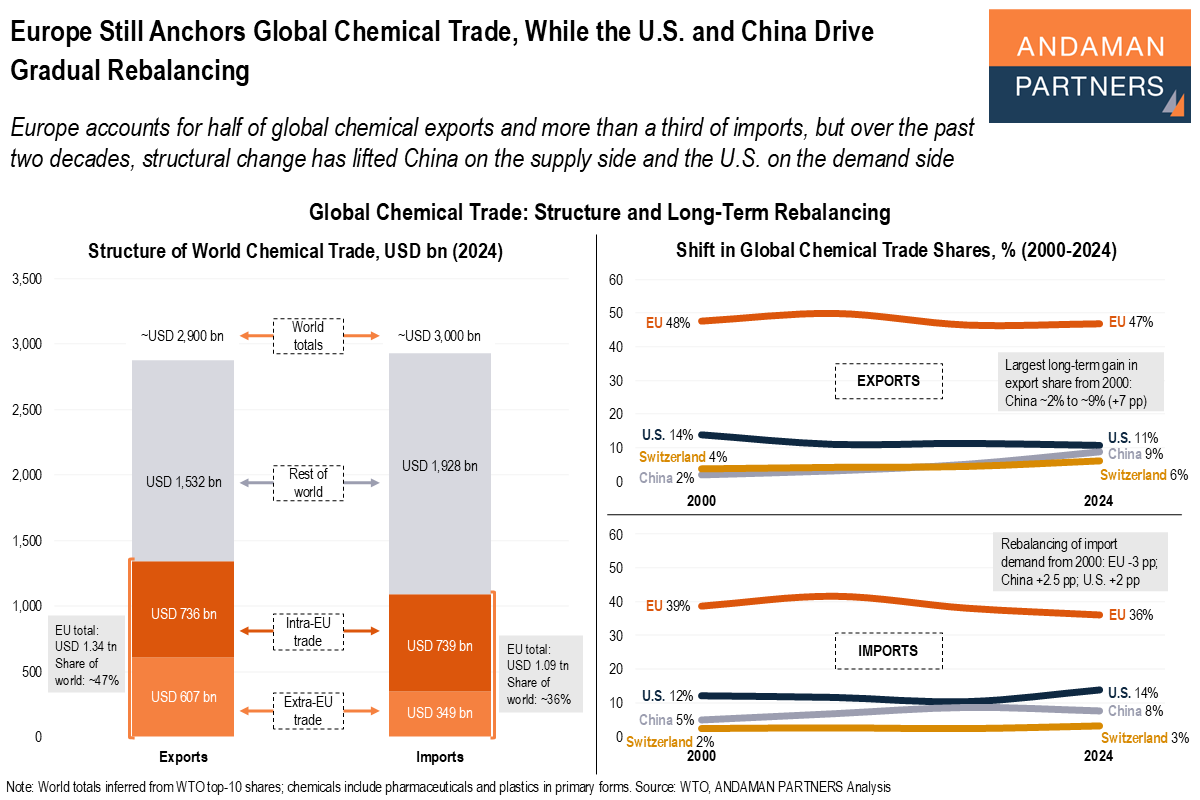

Europe accounts for half of global chemical exports and more than a third of imports, but over the past two decades, structural change has lifted China and the U.S.

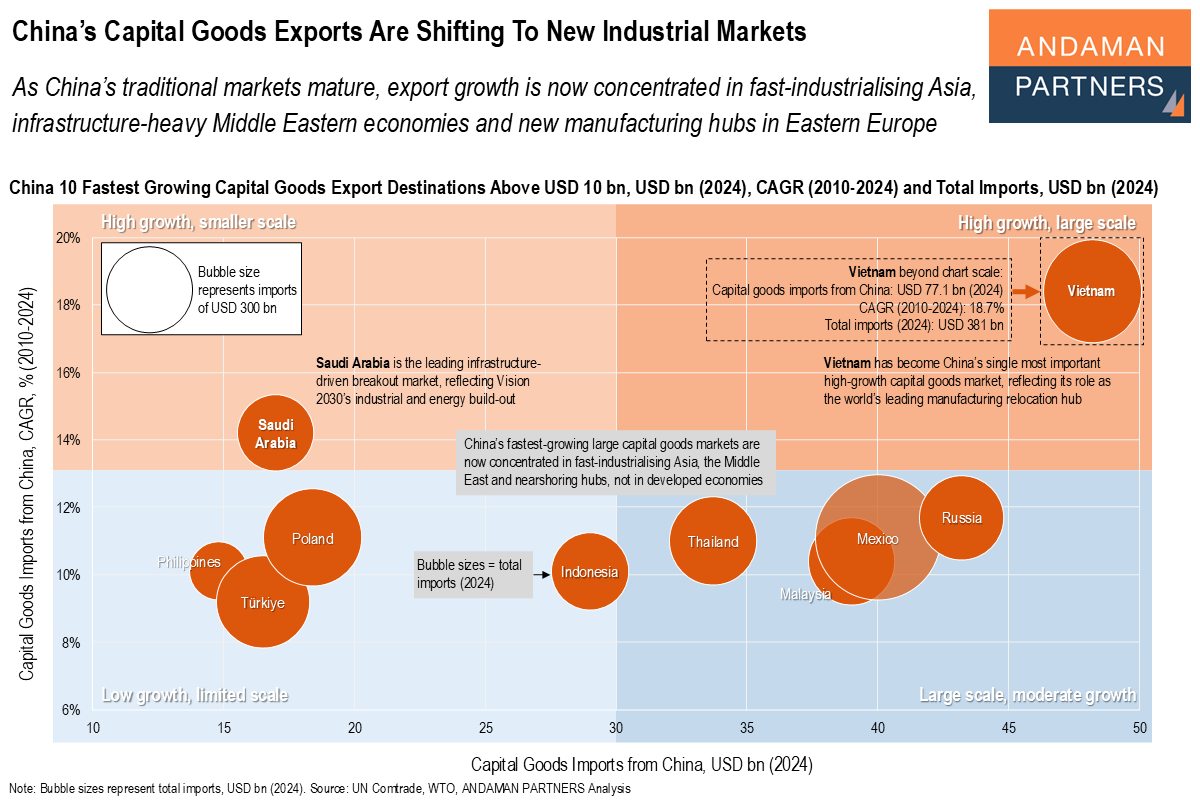

Export growth is now concentrated in fast-industrialising Asia, infrastructure-heavy Middle Eastern economies and new manufacturing hubs in Eastern Europe.

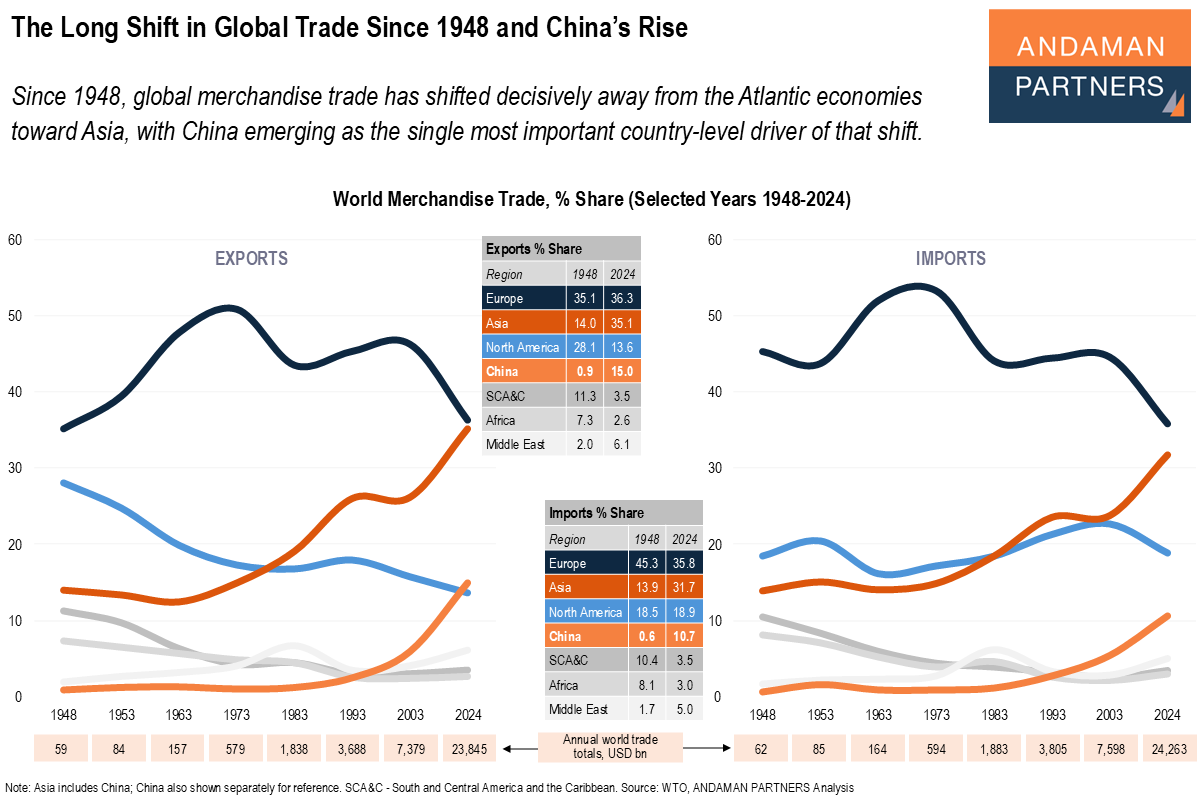

Since 1948, global merchandise trade has shifted decisively away from the Atlantic economies toward Asia.

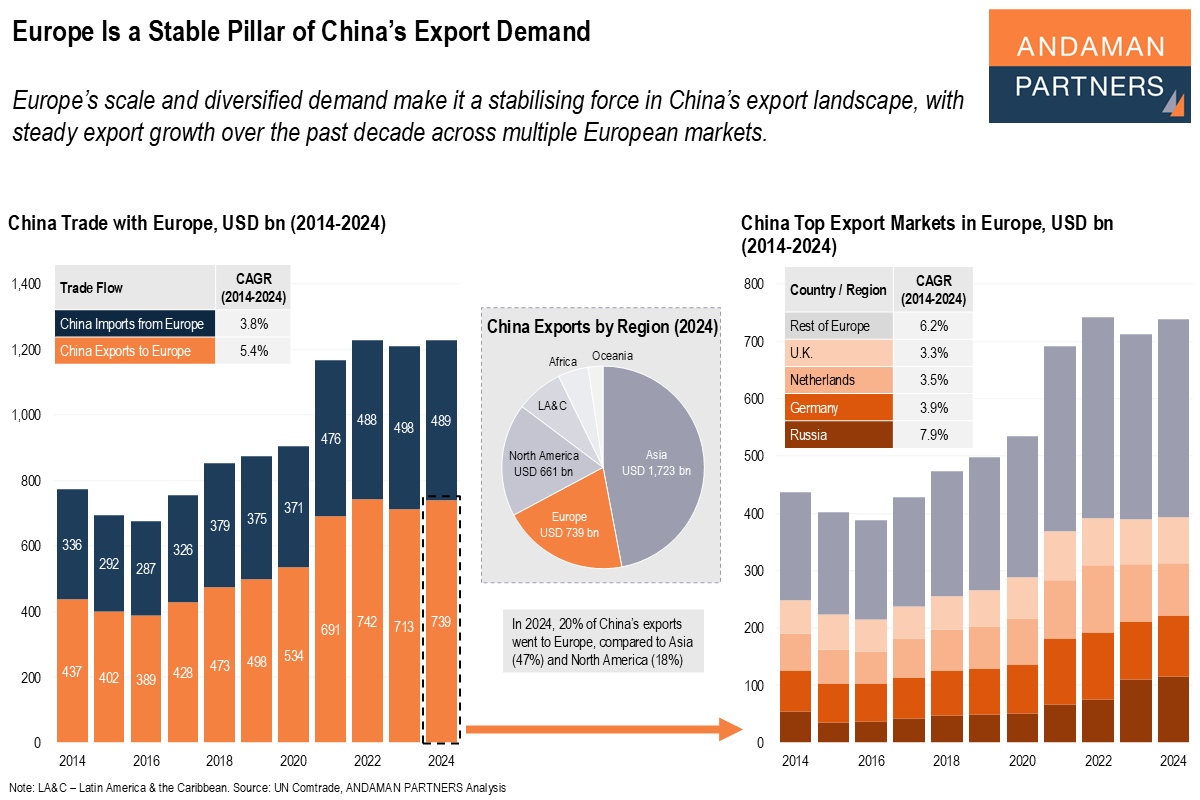

Europe’s scale and diversified demand make it a stabilising force in China’s export landscape, with steady export growth over the past decade.

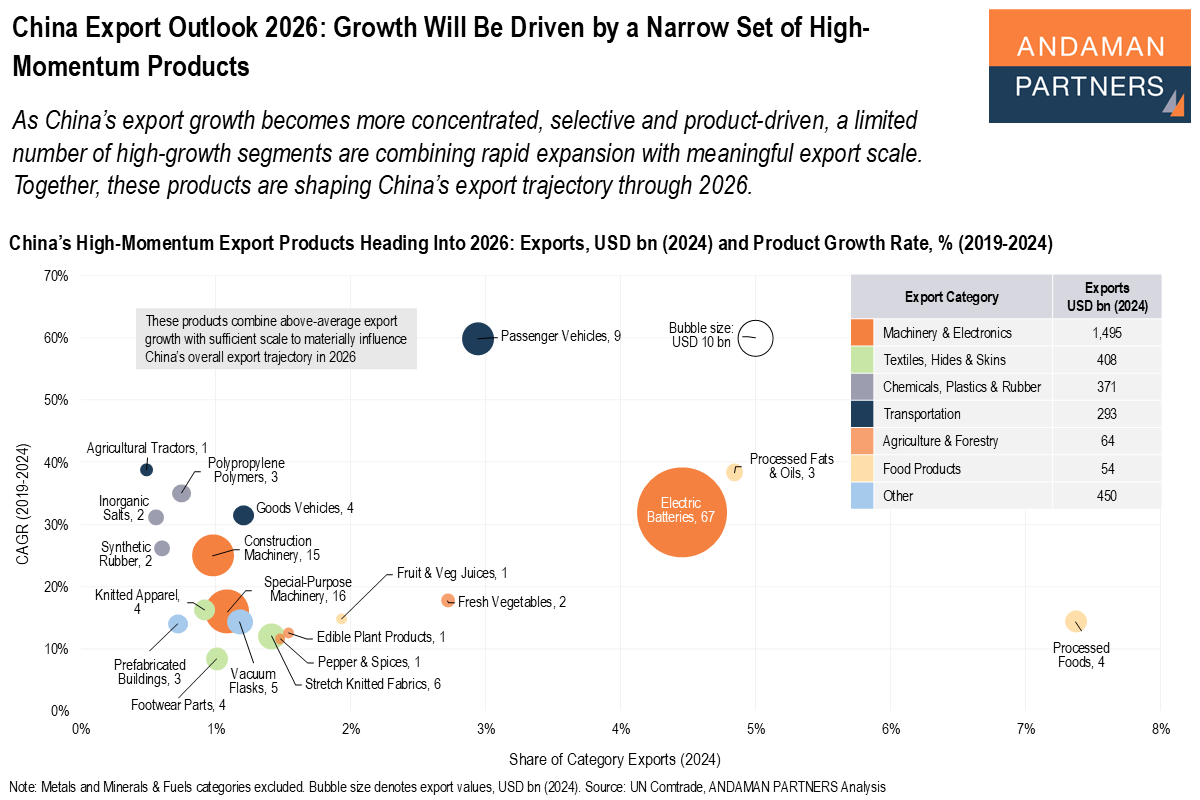

As China’s export growth becomes more concentrated, a limited number of high-growth segments are combining rapid expansion with meaningful export scale.

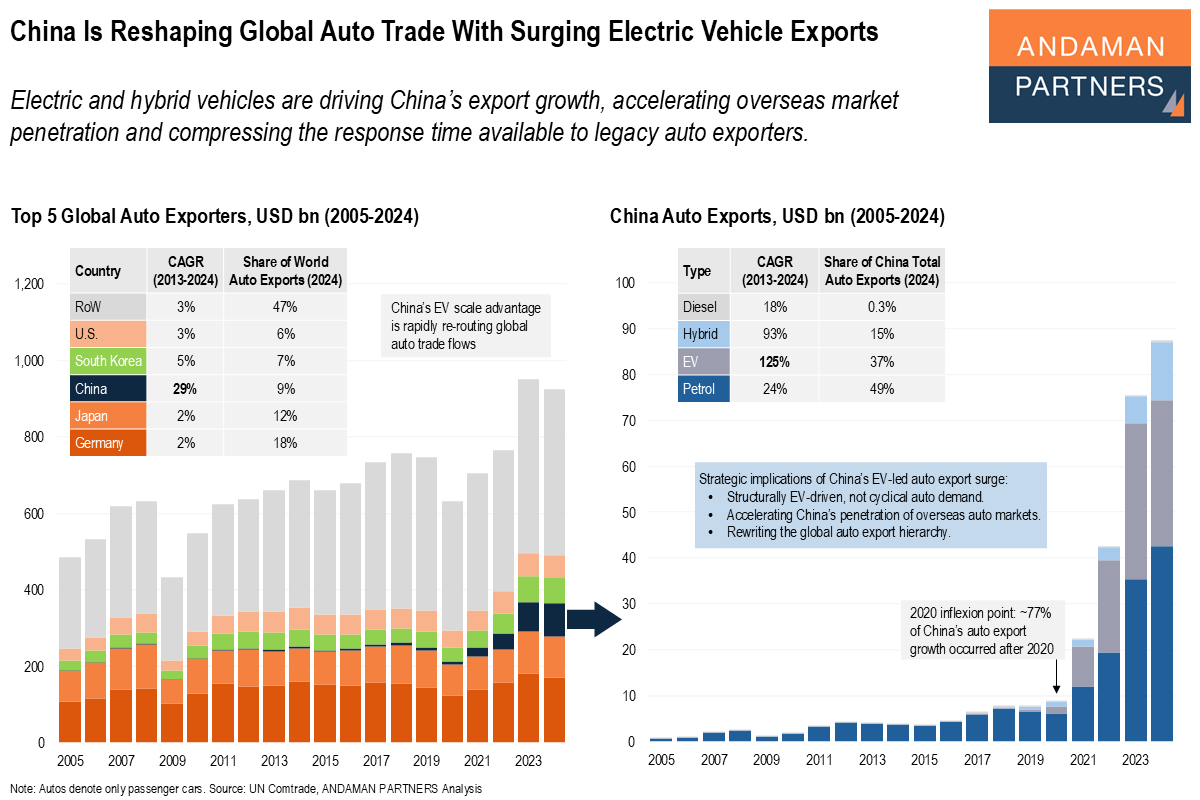

Electric and hybrid vehicles are driving China’s export growth, accelerating overseas market penetration and compressing the response time available to legacy auto exporters.

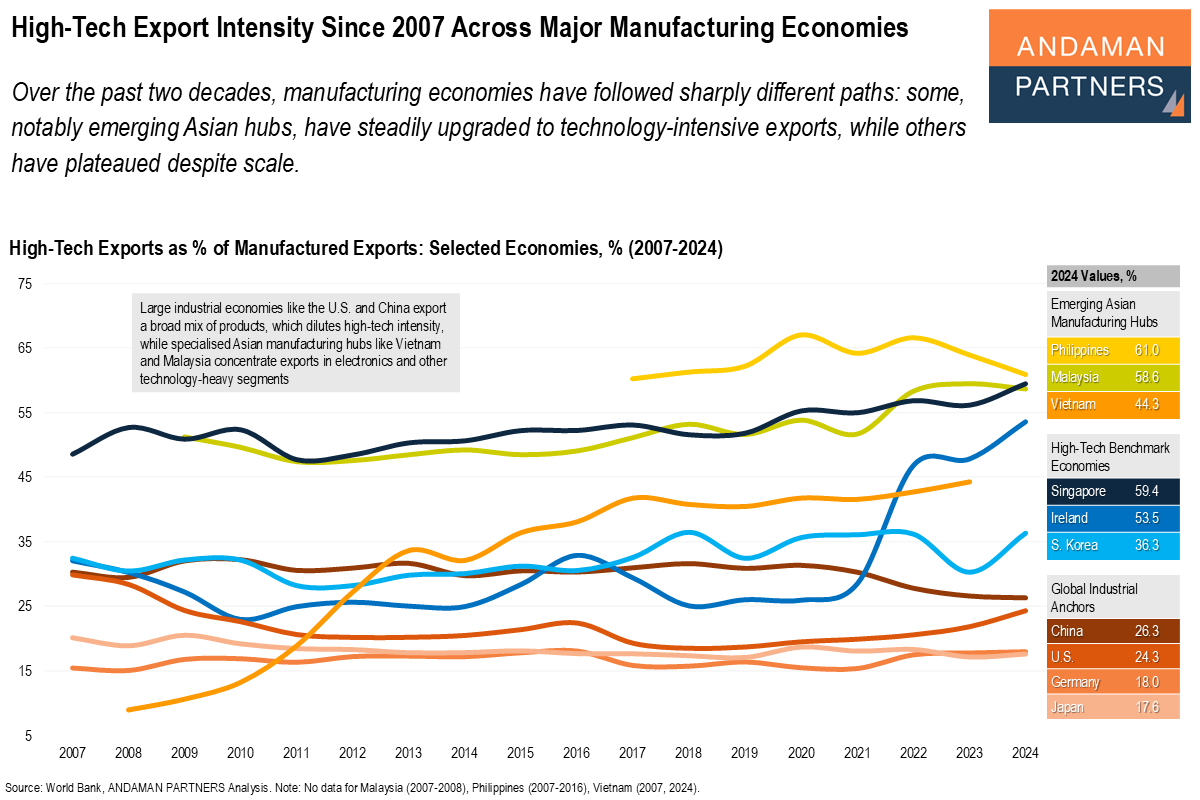

Some manufacturing economies have upgraded to tech-intensive exports while others have plateaued despite scale.

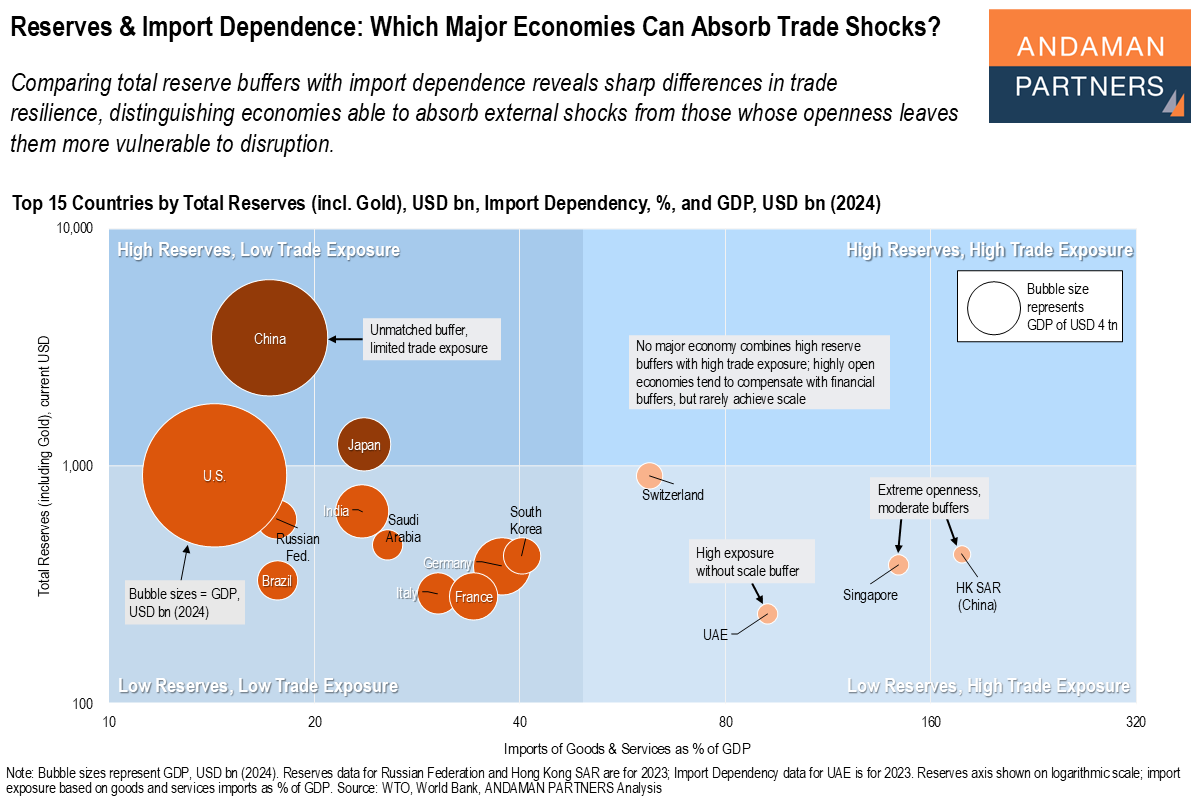

Comparing total reserve buffers with import dependence reveals sharp differences in trade resilience among major economies.

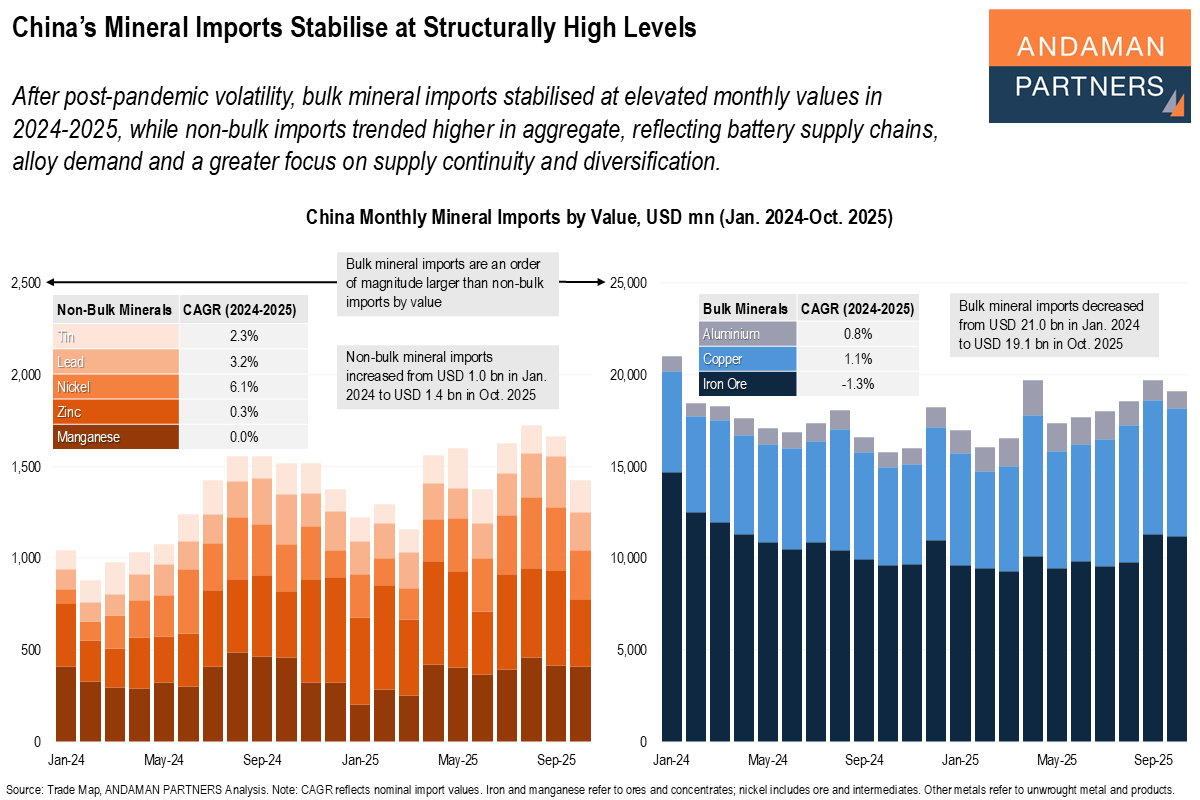

Bulk mineral imports stabilised at elevated monthly values in 2024-2025, while non-bulk imports trended higher in aggregate.