Transition Metal Supply Expanded in 2025, Control Remains Concentrated

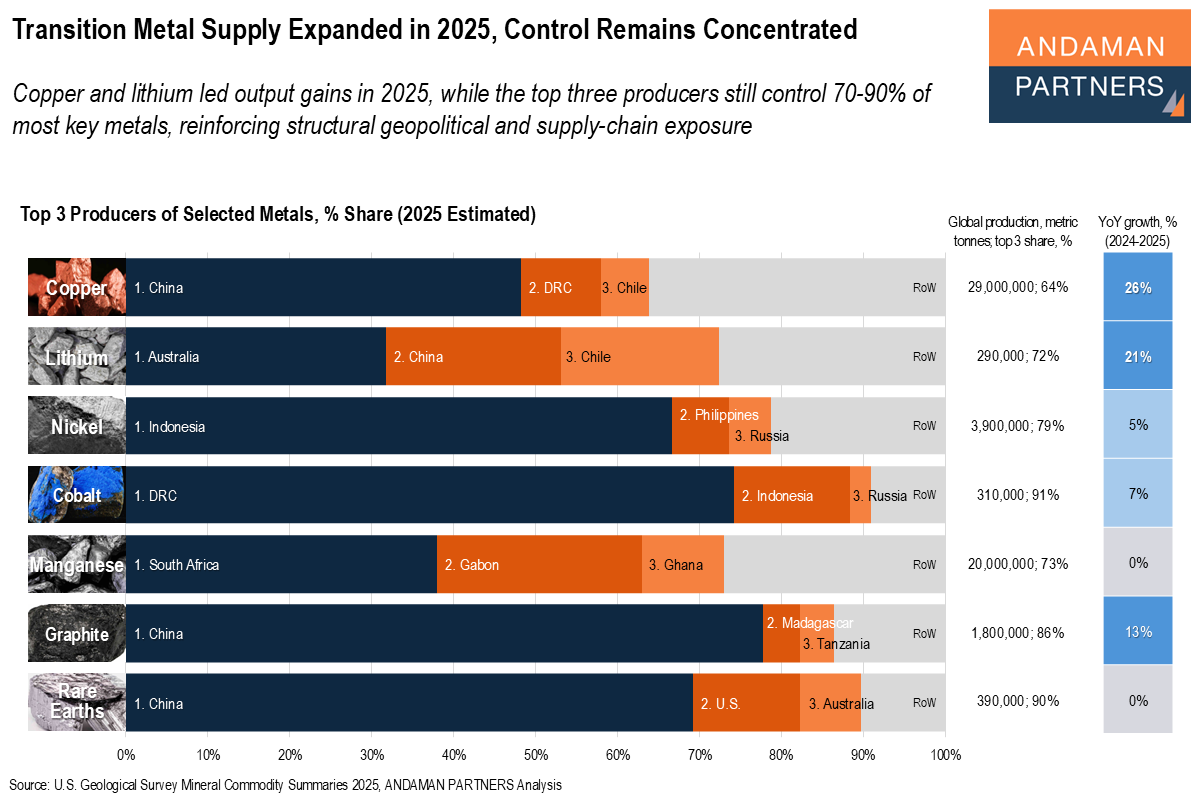

Copper and lithium led output gains in 2025, while the top three producers still control 70-90% of most key metals.

Copper and lithium led output gains in 2025, while the top three producers still control 70-90% of most key metals.

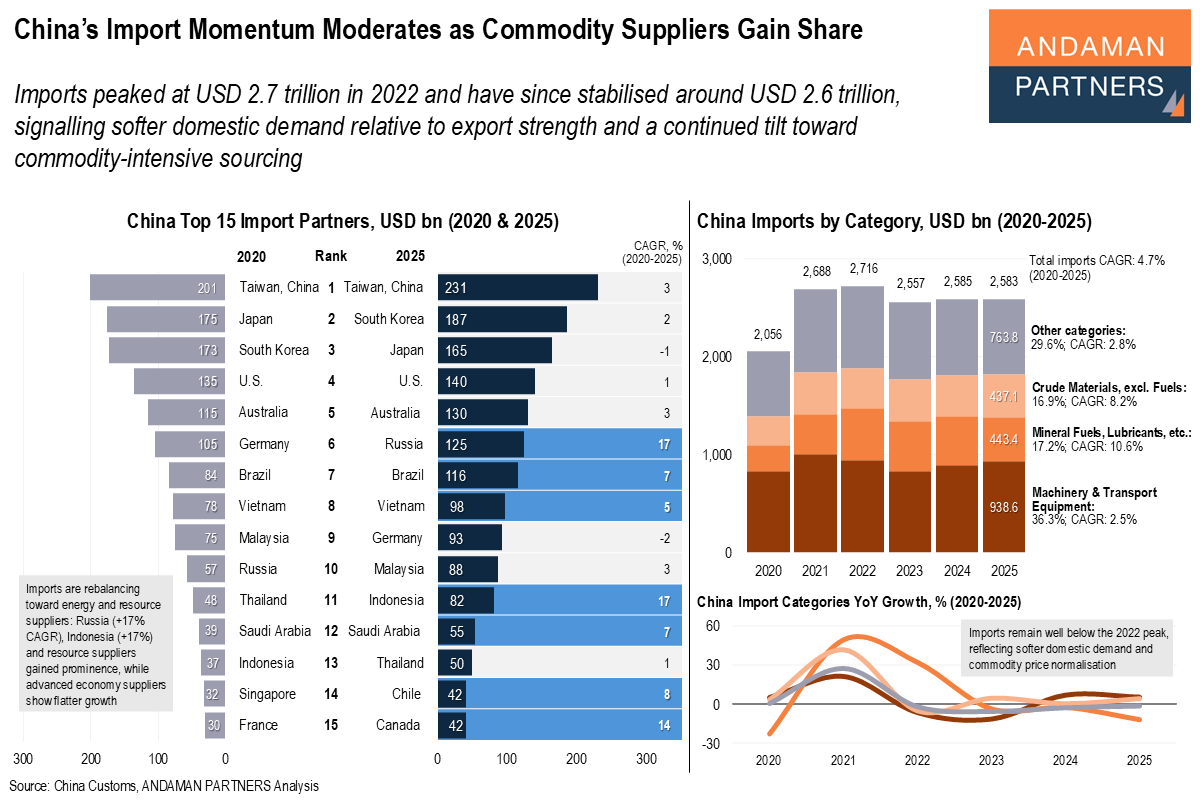

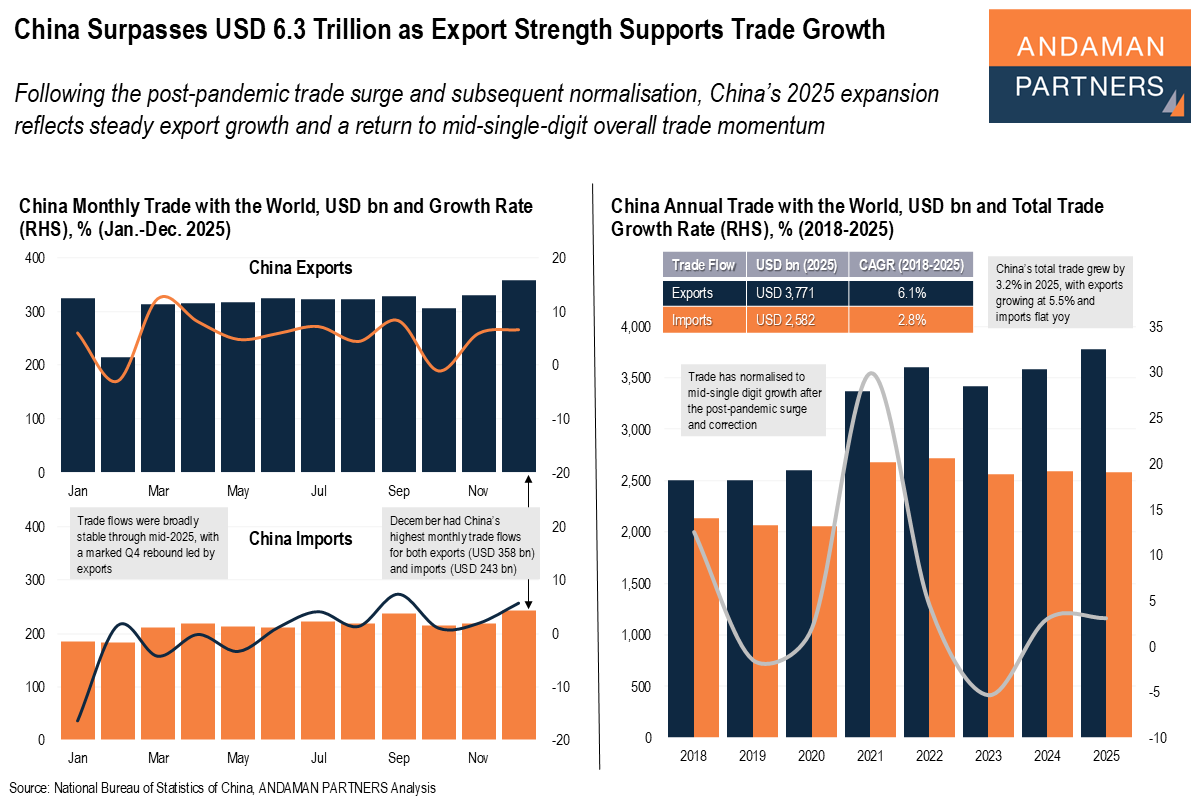

Imports have stabilised around USD 2.6 trillion, signalling softer domestic demand and a continued tilt toward commodity-intensive sourcing.

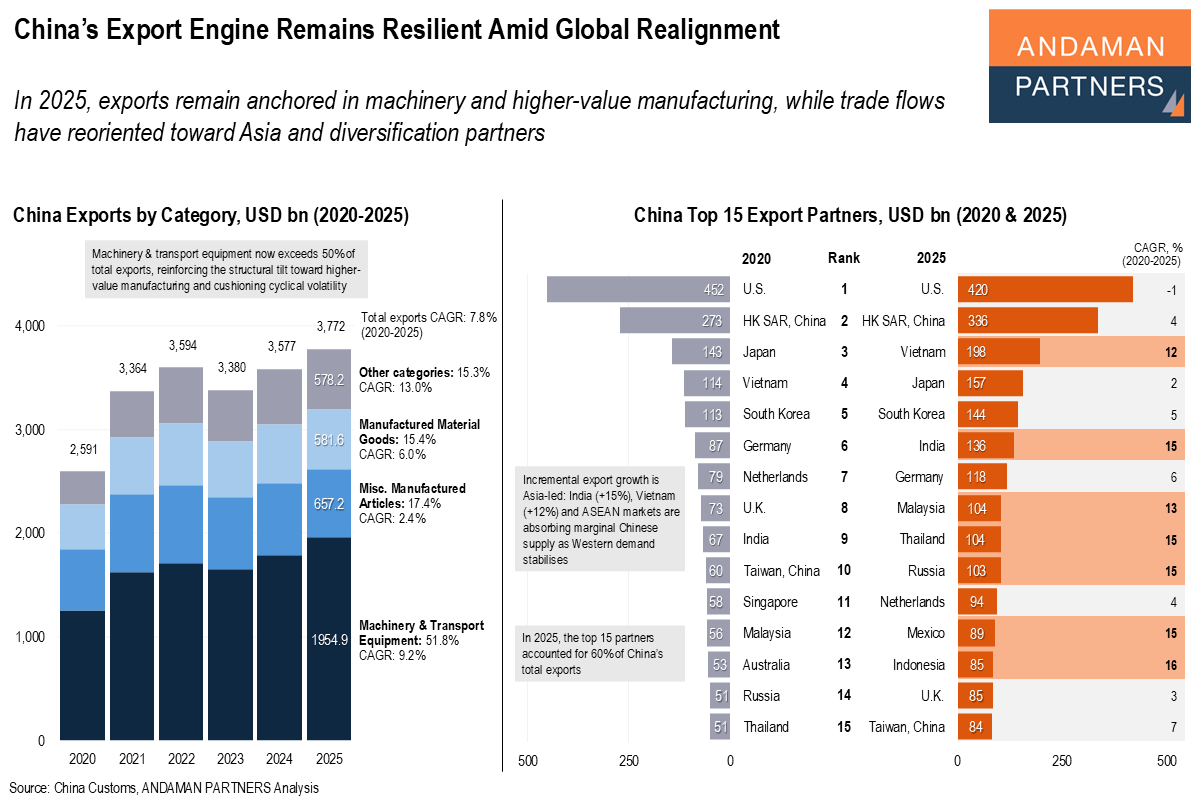

Exports remain anchored in machinery and higher-value manufacturing, while trade flows have reoriented toward Asia and diversification partners.

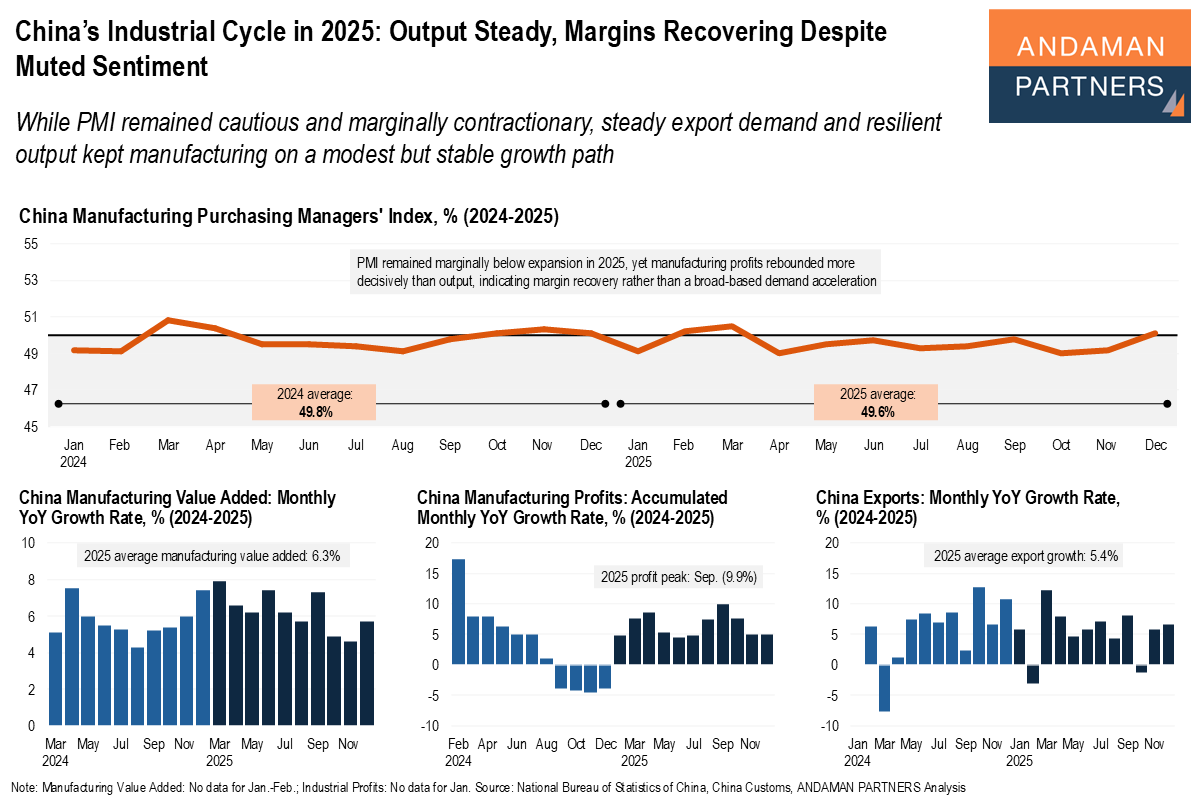

While PMI remained cautious and marginally contractionary, steady export demand and resilient output kept manufacturing on a modest but stable growth path.

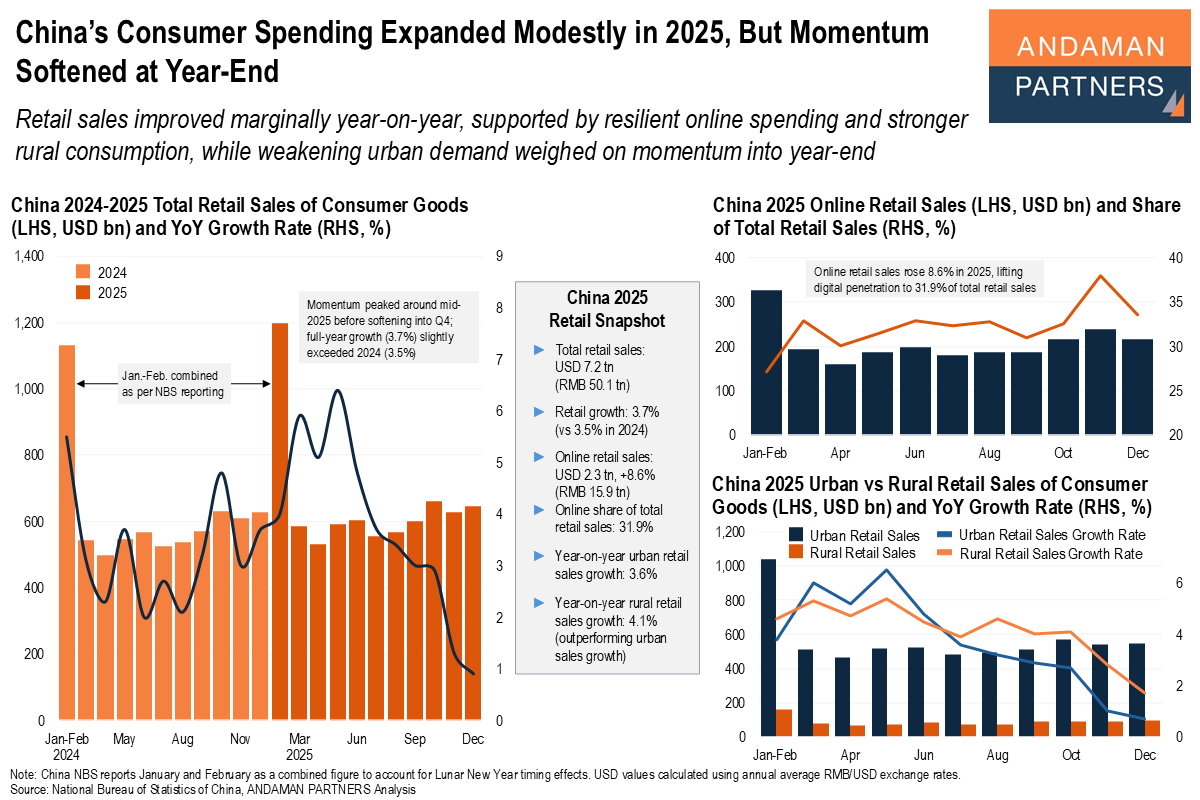

Retail sales improved marginally year-on-year, supported by resilient online spending and stronger rural consumption.

China’s 2025 expansion reflects steady export growth and a return to mid-single-digit overall trade momentum.

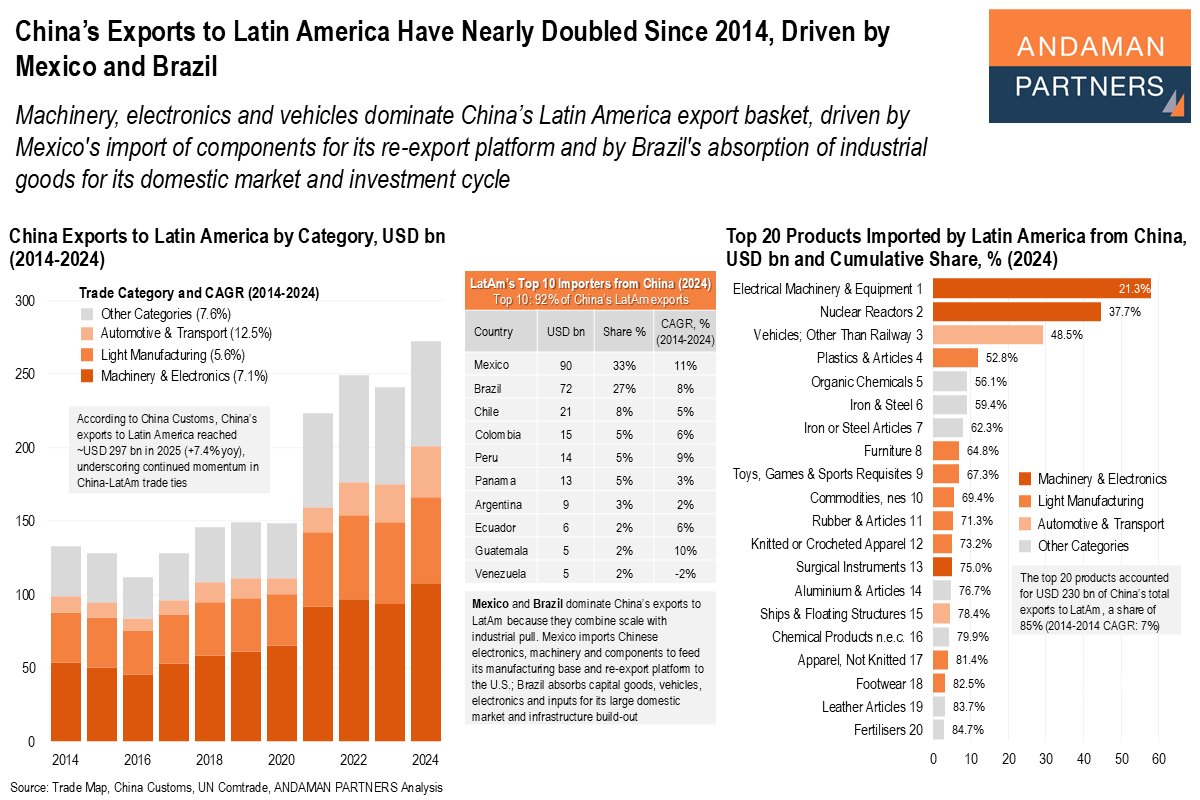

Machinery, electronics and vehicles dominate China’s Latin America export basket, driven by Mexico and Brazil.

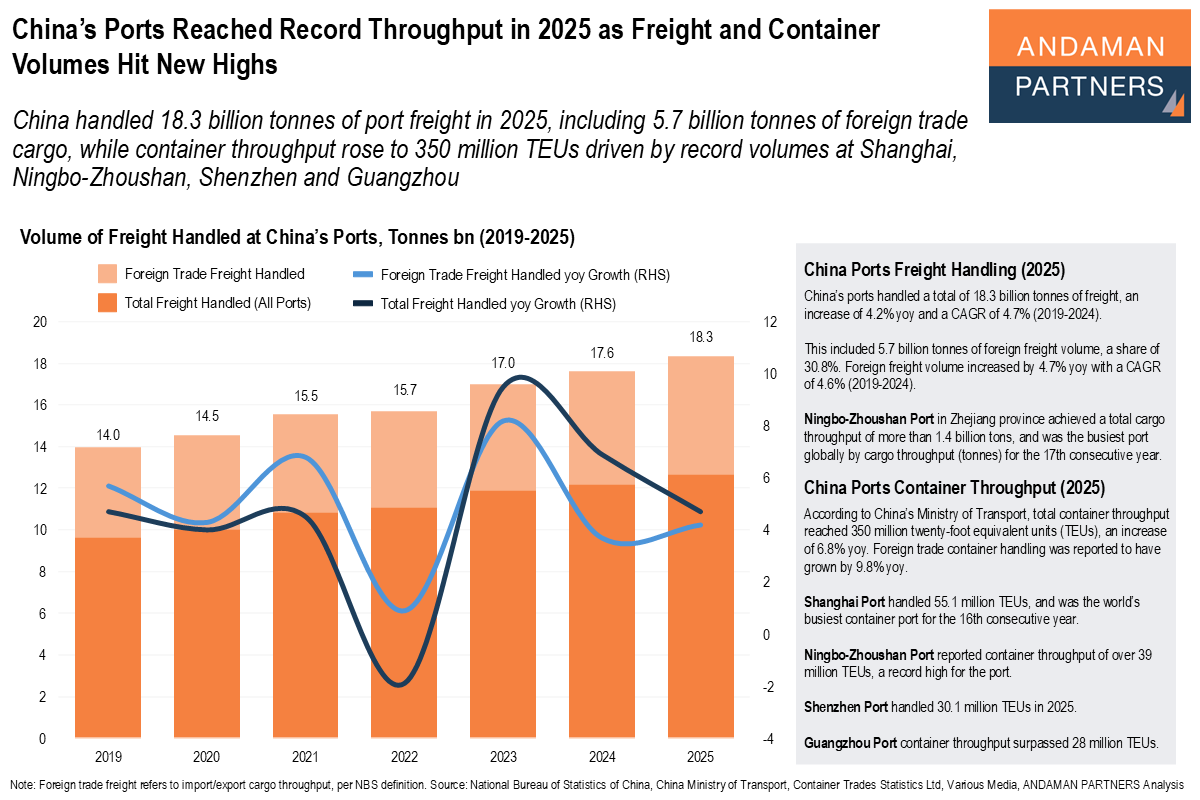

China handled 18.3 billion tonnes of port freight in 2025, including 5.7 billion tonnes of foreign trade cargo.

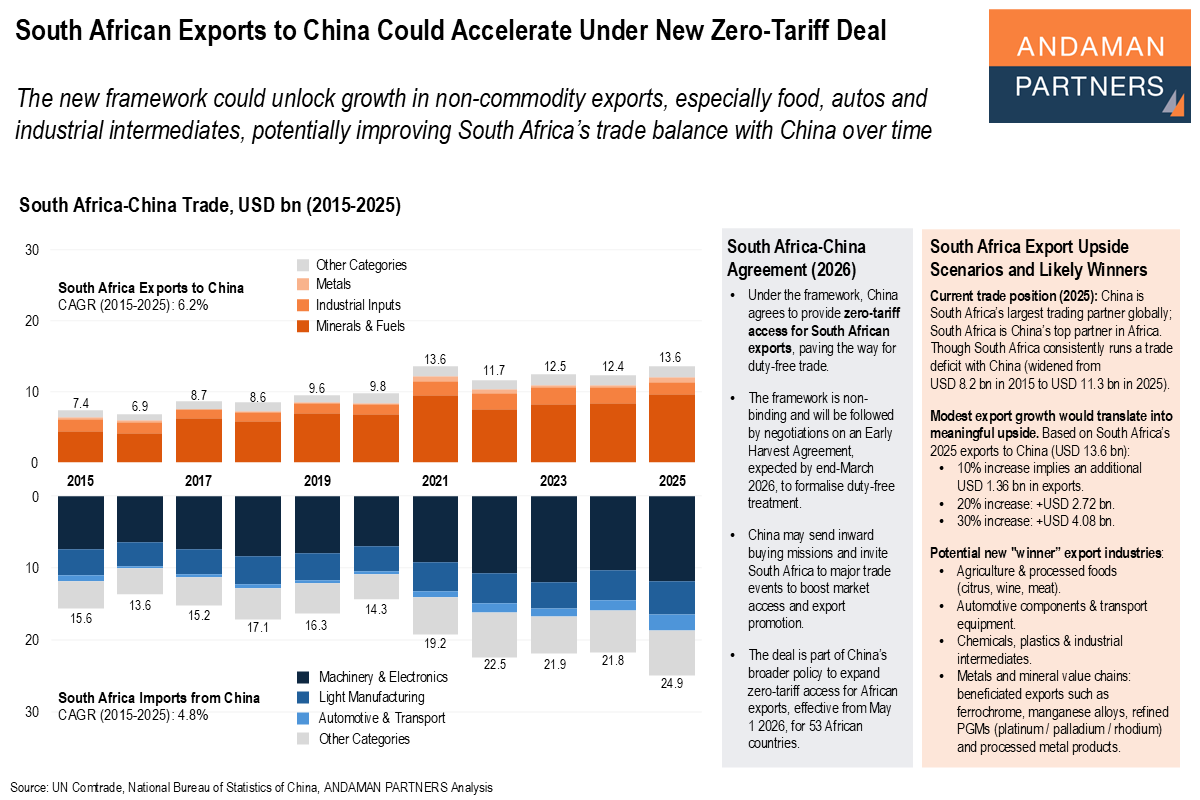

The new framework could unlock growth in non-commodity exports, especially food, autos and industrial intermediates.

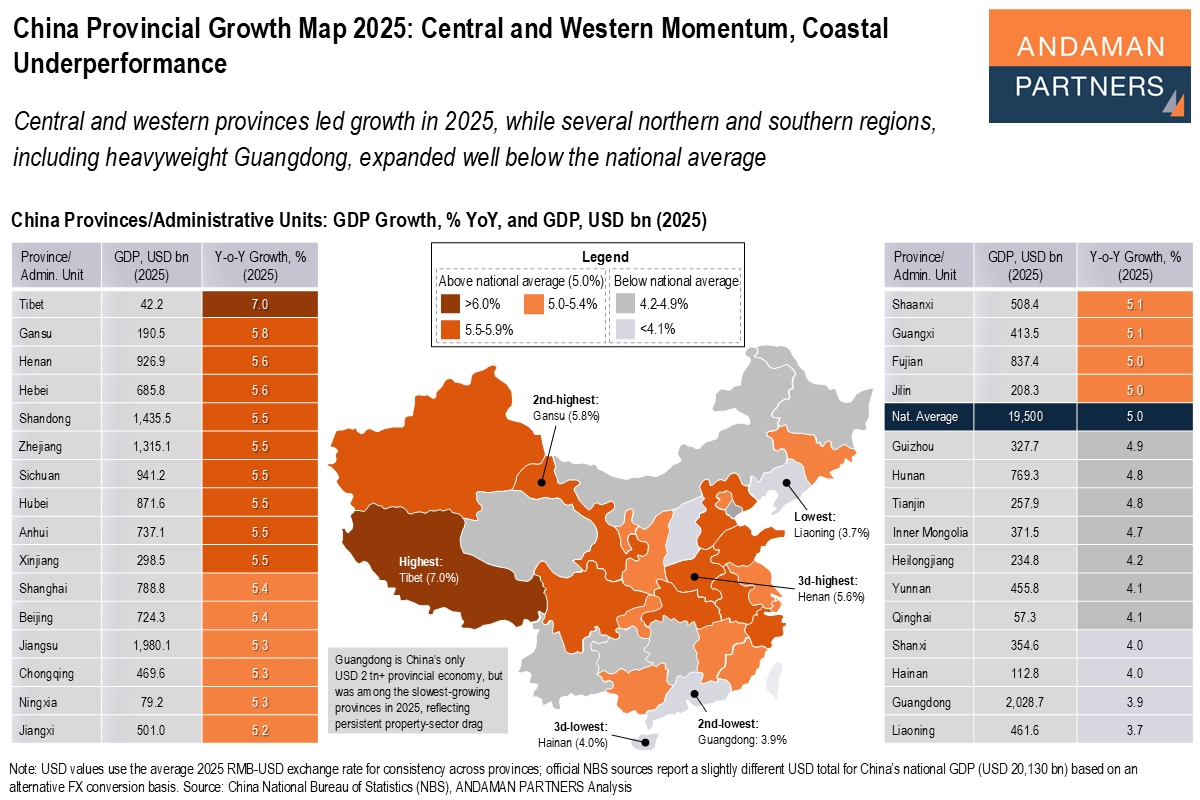

Central and western provinces led growth in 2025, while several northern and southern regions expanded well below the national average.