Global Trade Imbalances Widen in 2025 as Surpluses Strengthen and Deficits Deepen

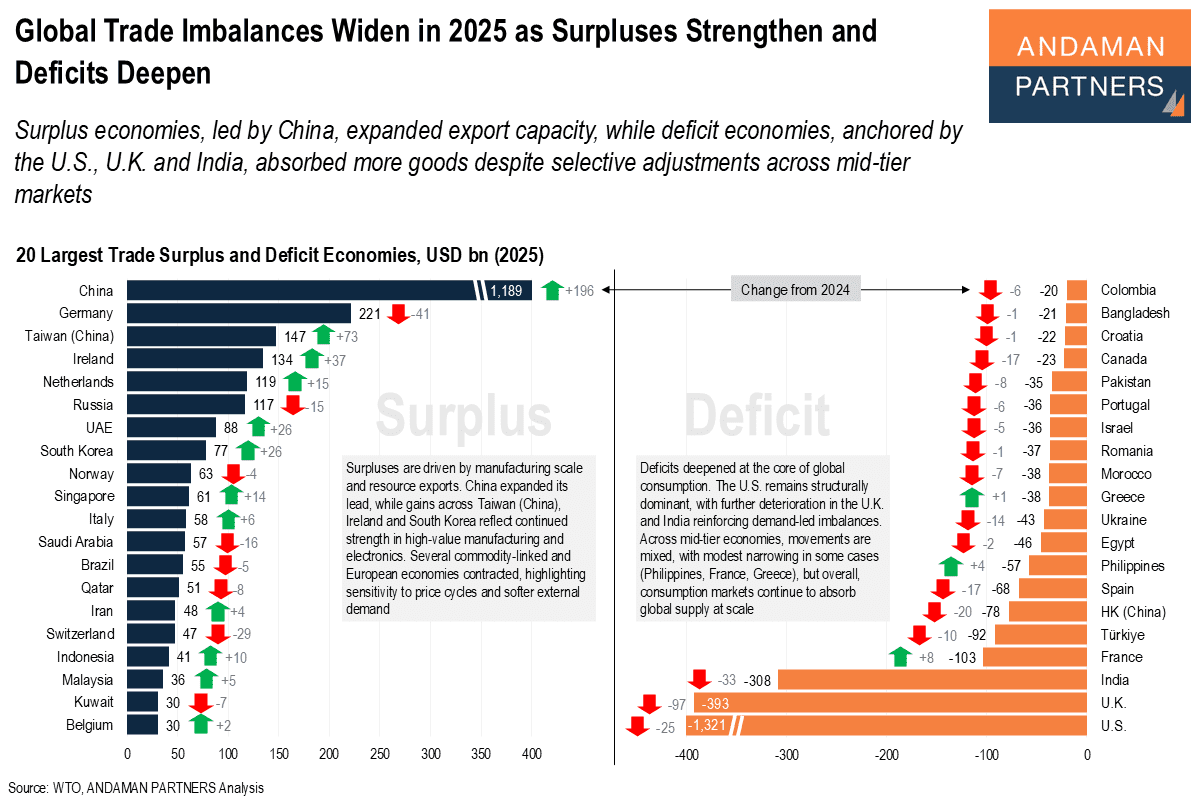

Surplus economies expanded export capacity, while deficit economies absorbed more goods despite selective adjustments across mid-tier markets.

Surplus economies expanded export capacity, while deficit economies absorbed more goods despite selective adjustments across mid-tier markets.

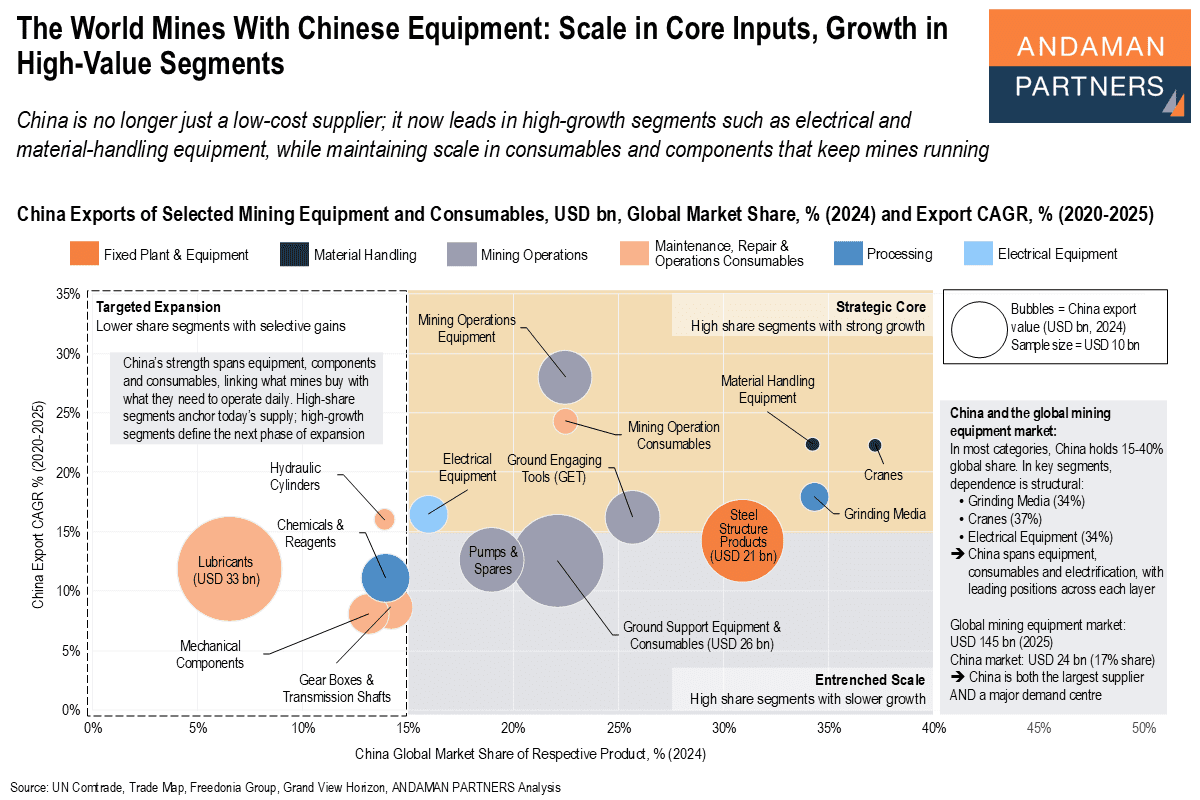

China is no longer just a low-cost supplier; it now leads in high-growth segments while maintaining scale in consumables and components.

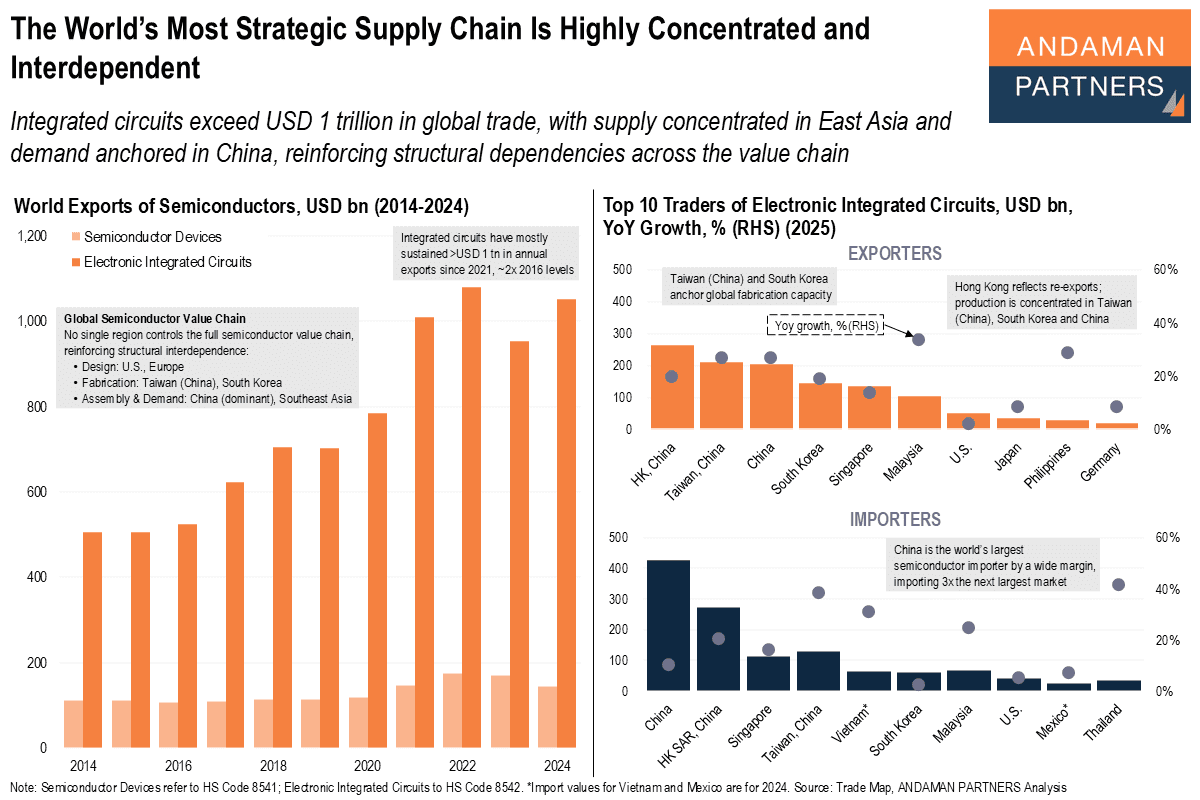

Integrated circuits exceed USD 1 trillion in global trade, with supply concentrated in Asia and demand in China, reinforcing structural dependencies.

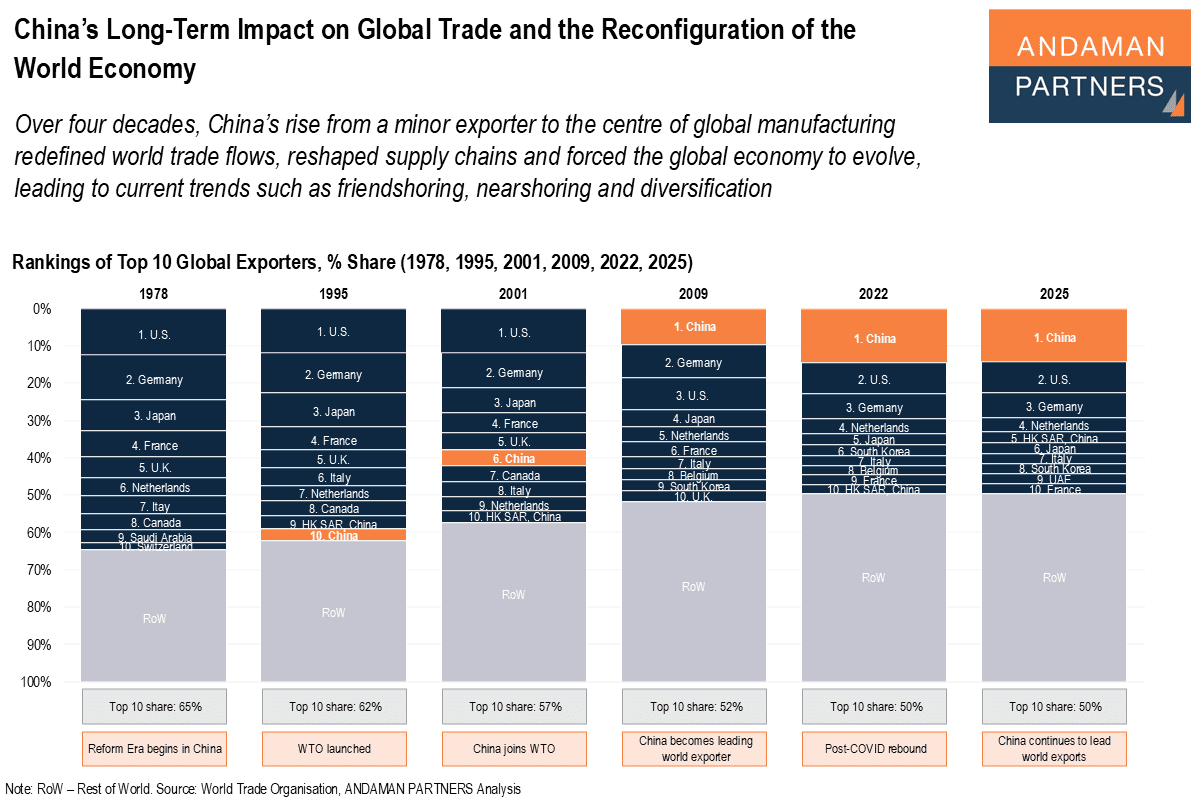

China’s rise from a minor exporter to the centre of global manufacturing redefined trade flows, reshaped supply chains and forced the global economy to evolve.

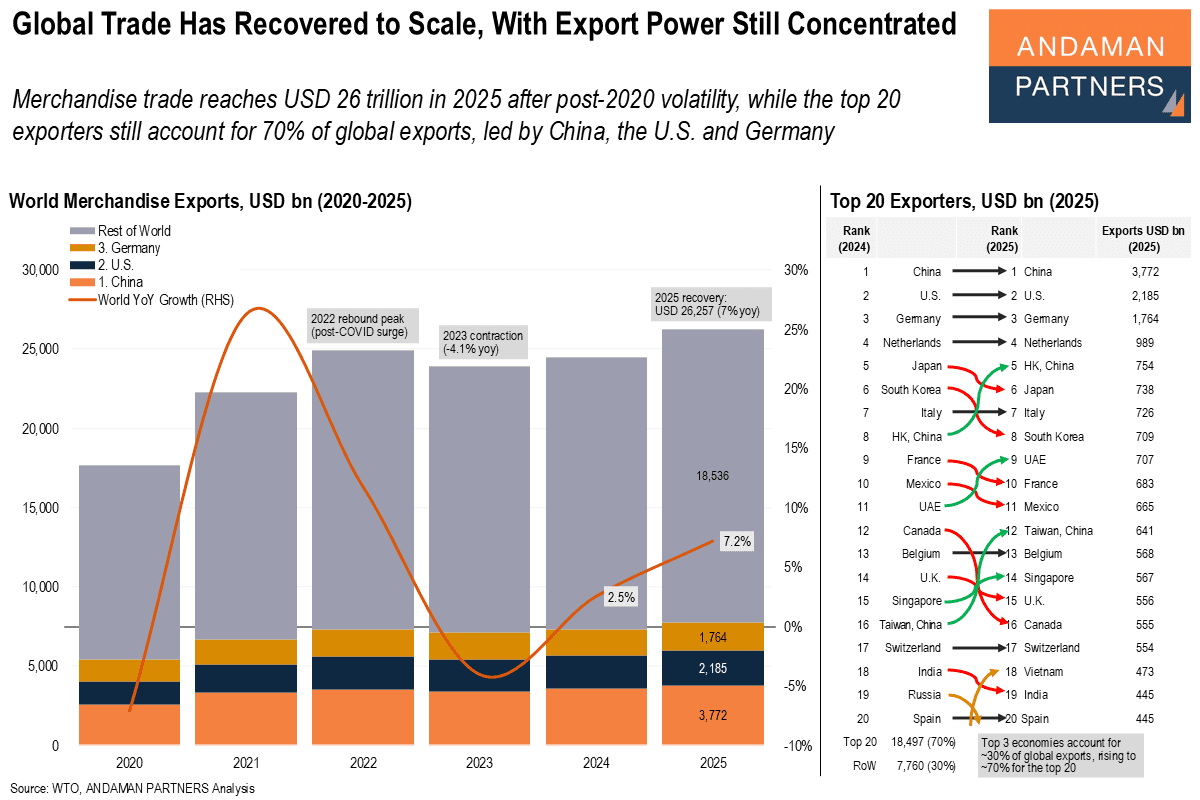

Merchandise trade reaches USD 26 trillion in 2025, while the top 20 exporters account for 70% of global exports.

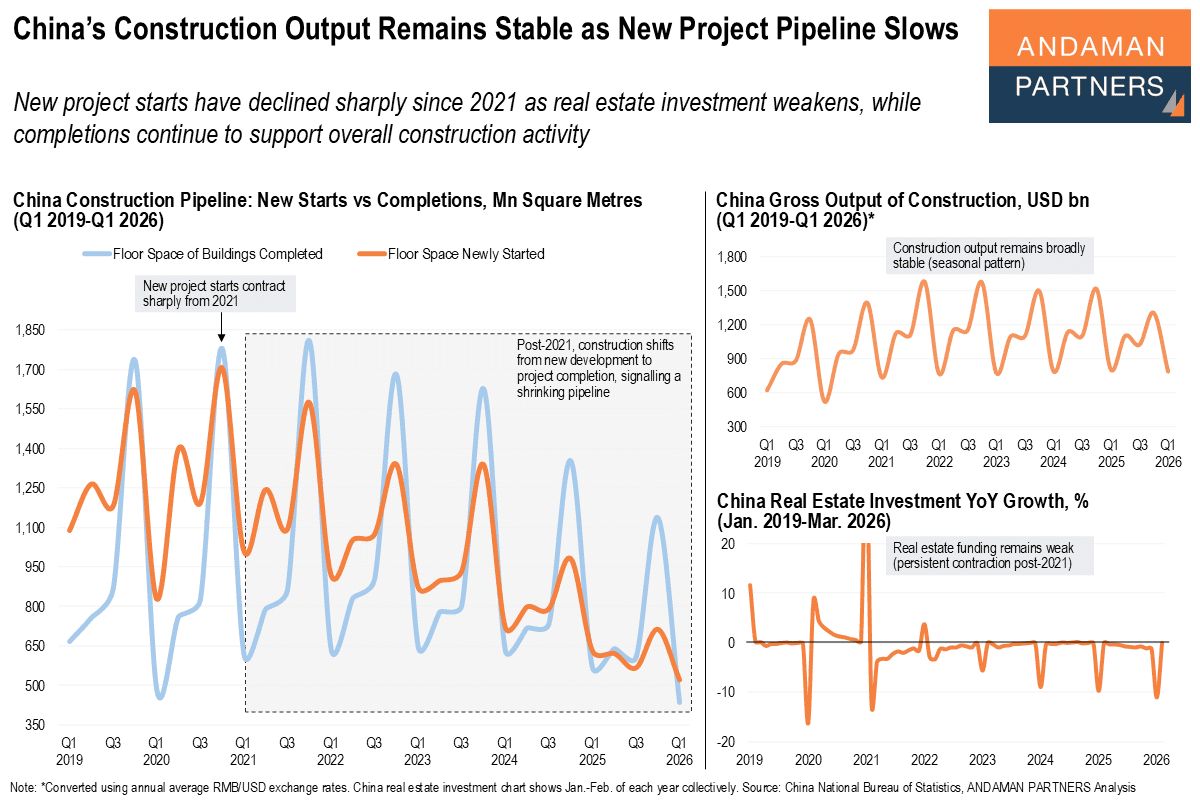

New project starts have declined sharply since 2021 as real estate investment weakens, while completions continue to support overall construction activity.

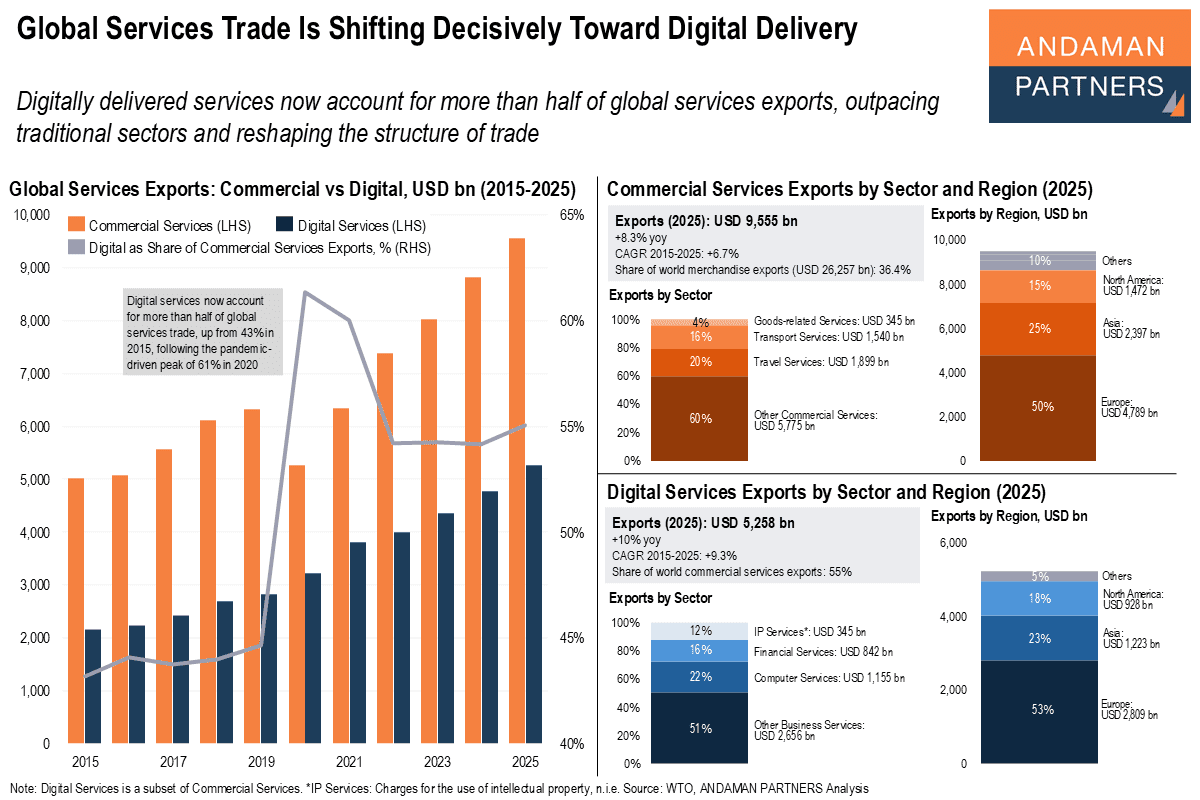

Digitally delivered services now account for more than half of global services exports, outpacing traditional sectors and reshaping the structure of trade.

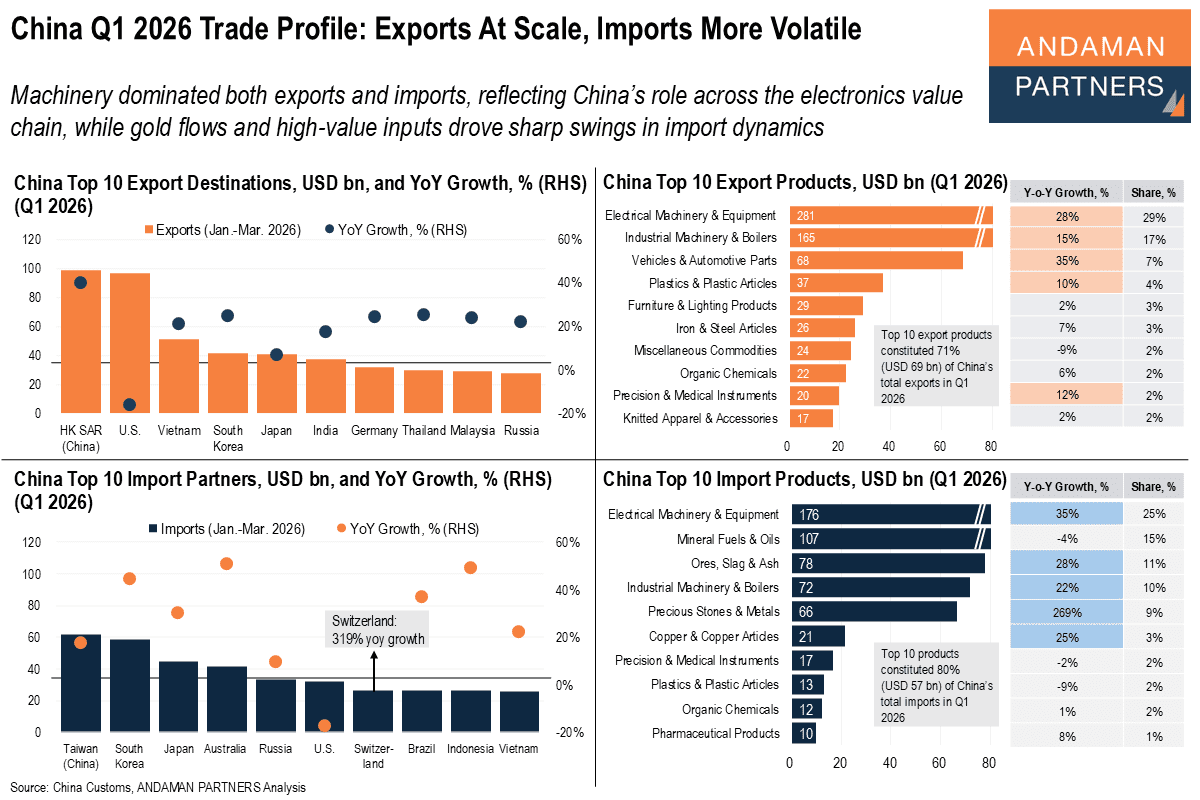

Machinery dominated exports and imports, reflecting China’s role across the electronics value chain; gold and high-value inputs drove import swings.

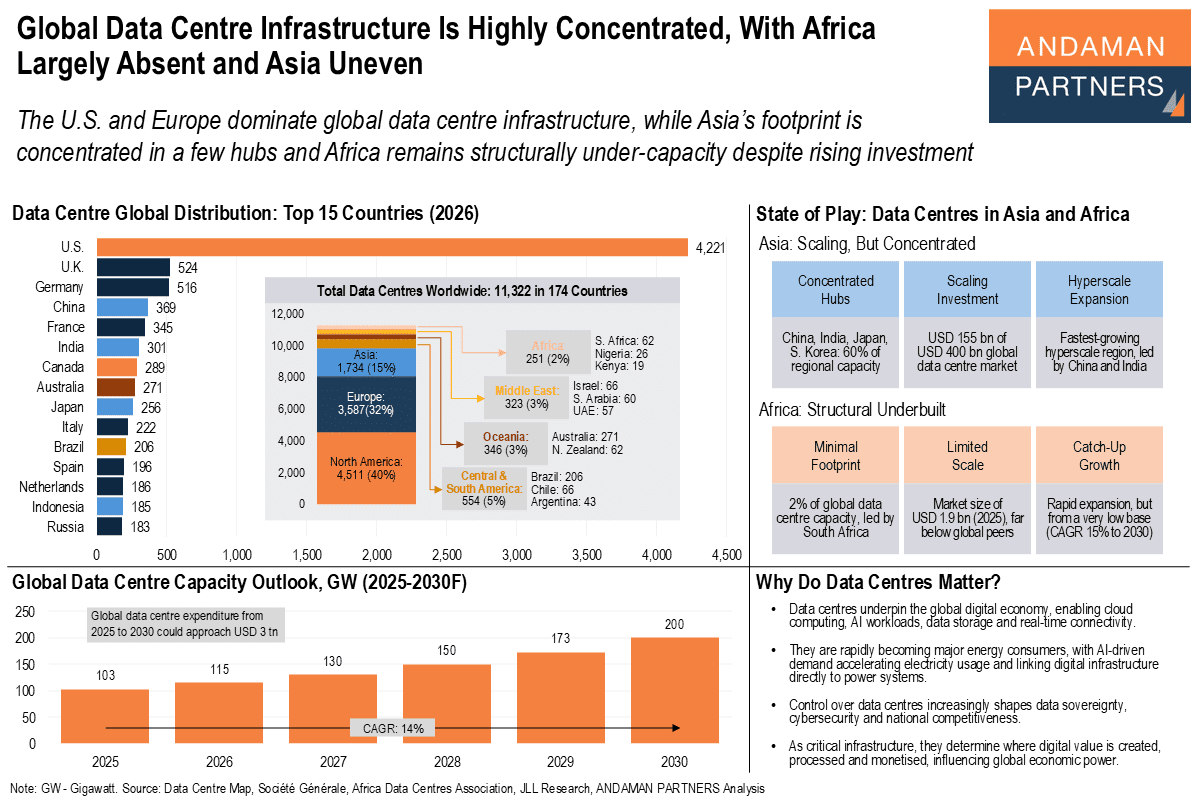

The U.S. and Europe dominate global data centre infrastructure, while Asia’s footprint is concentrated in a few hubs

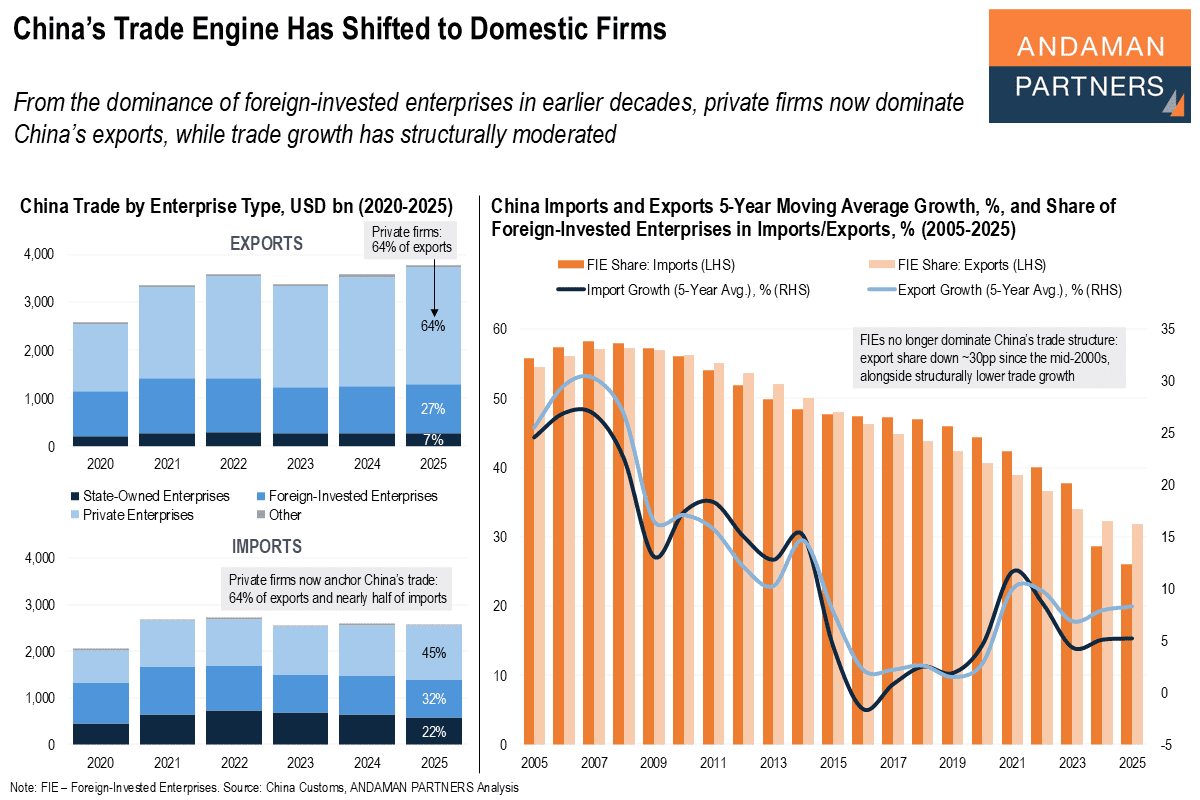

Private firms now dominate China’s exports, while trade growth has structurally moderated.