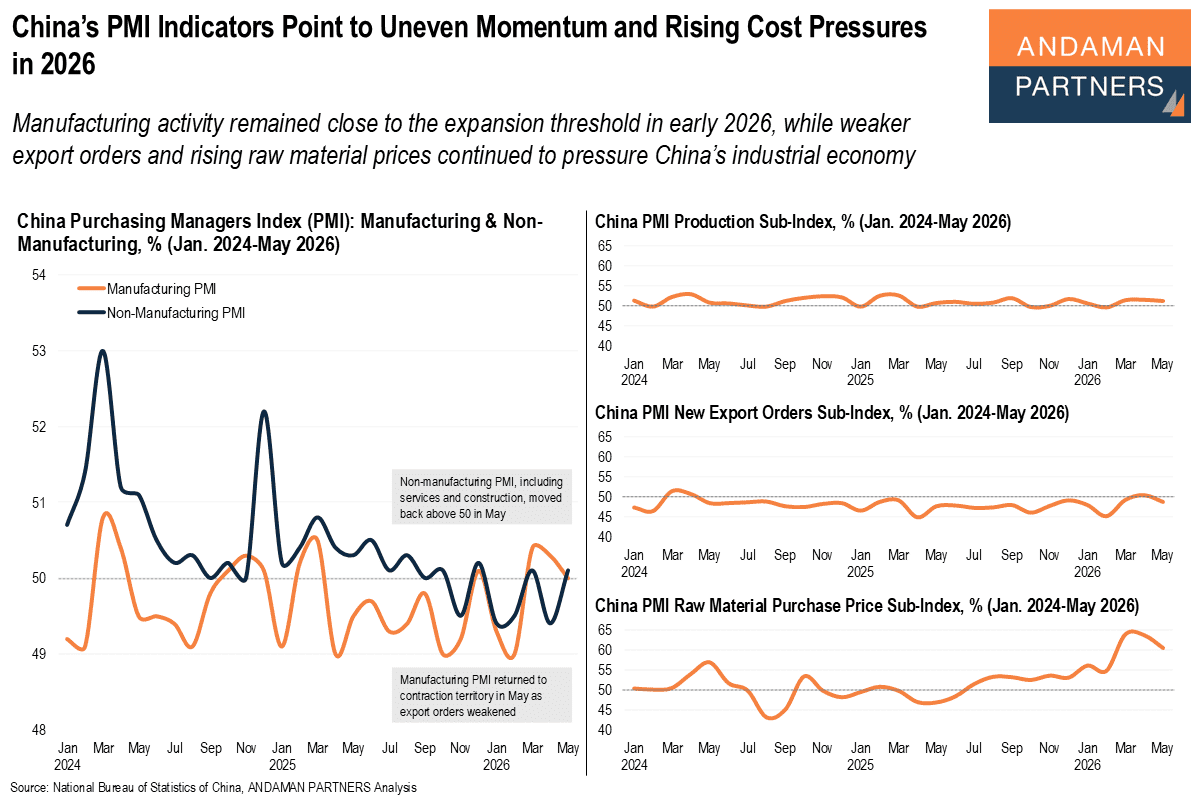

China’s PMI Indicators Point to Uneven Momentum and Rising Cost Pressures in 2026

Manufacturing activity remained close to expansion in early 2026, while weaker export orders and raw material prices pressure the economy

Manufacturing activity remained close to expansion in early 2026, while weaker export orders and raw material prices pressure the economy

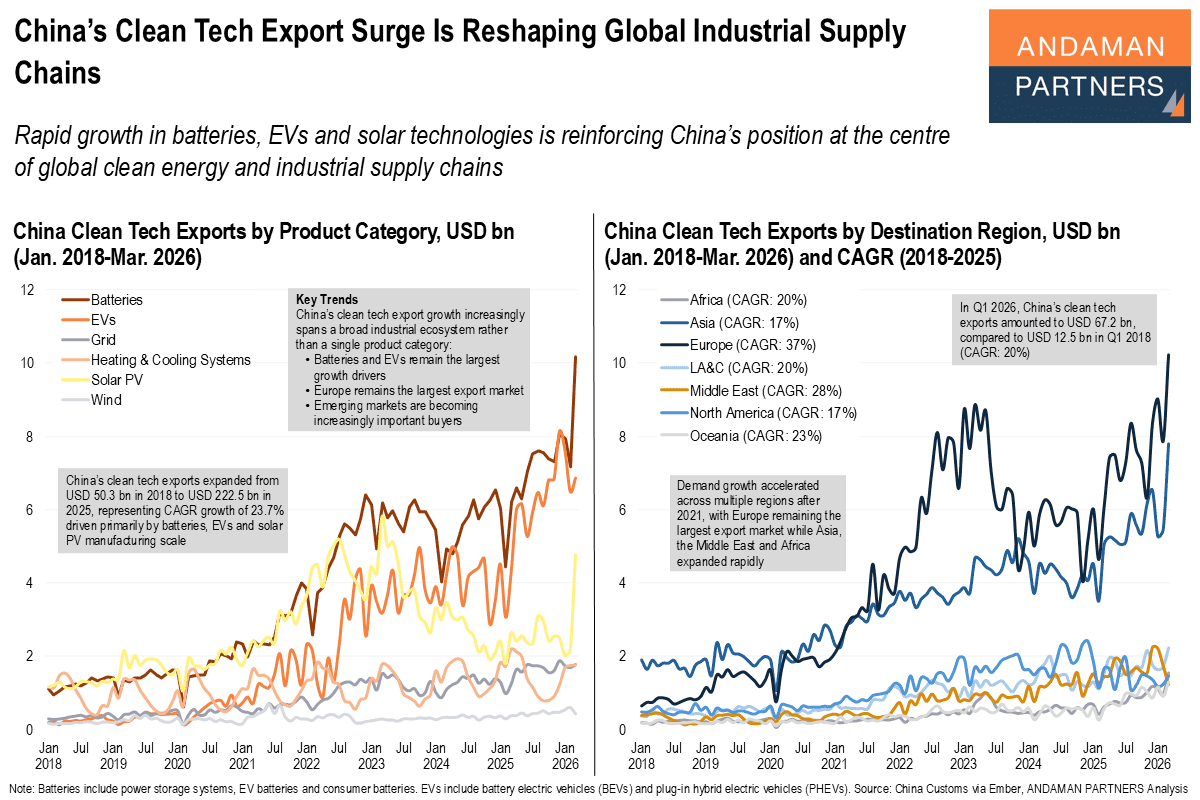

Rapid growth in batteries, EVs and solar technologies is reinforcing China’s position at the centre of global clean energy supply chains.

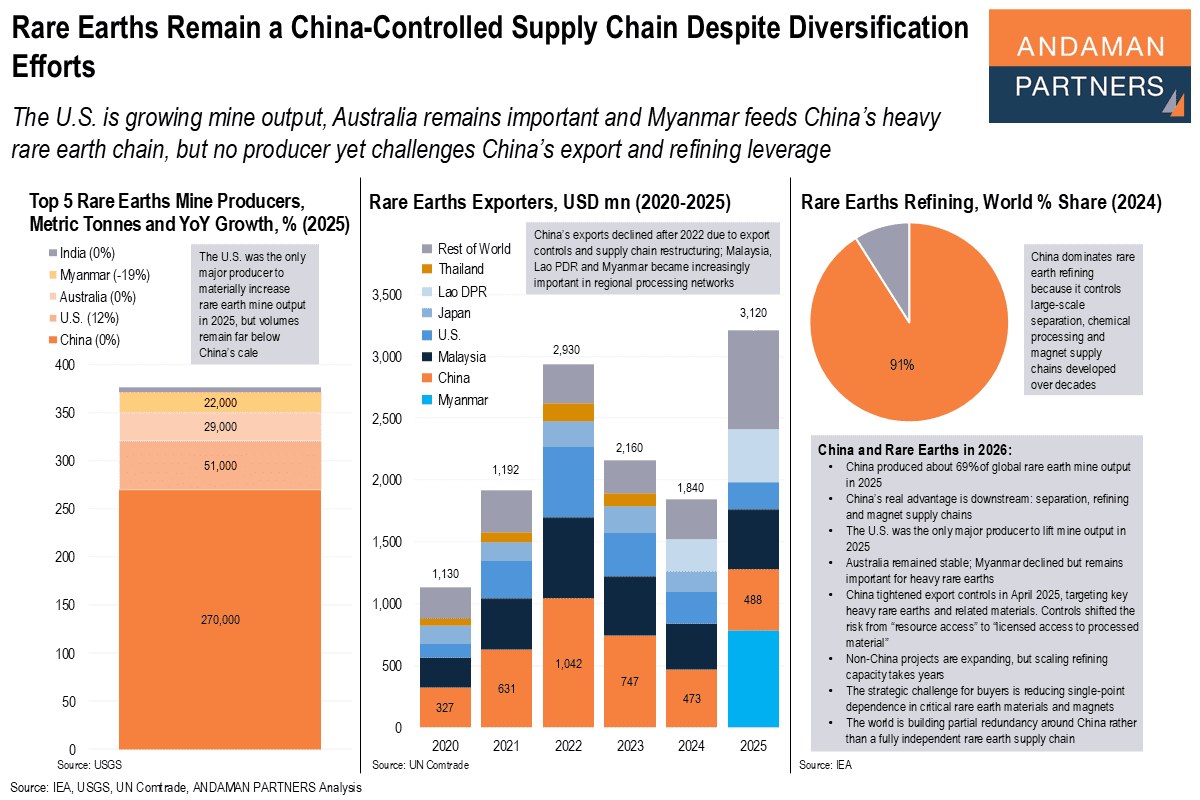

The U.S. is growing mine output, but no producer yet challenges China’s export and refining leverage.

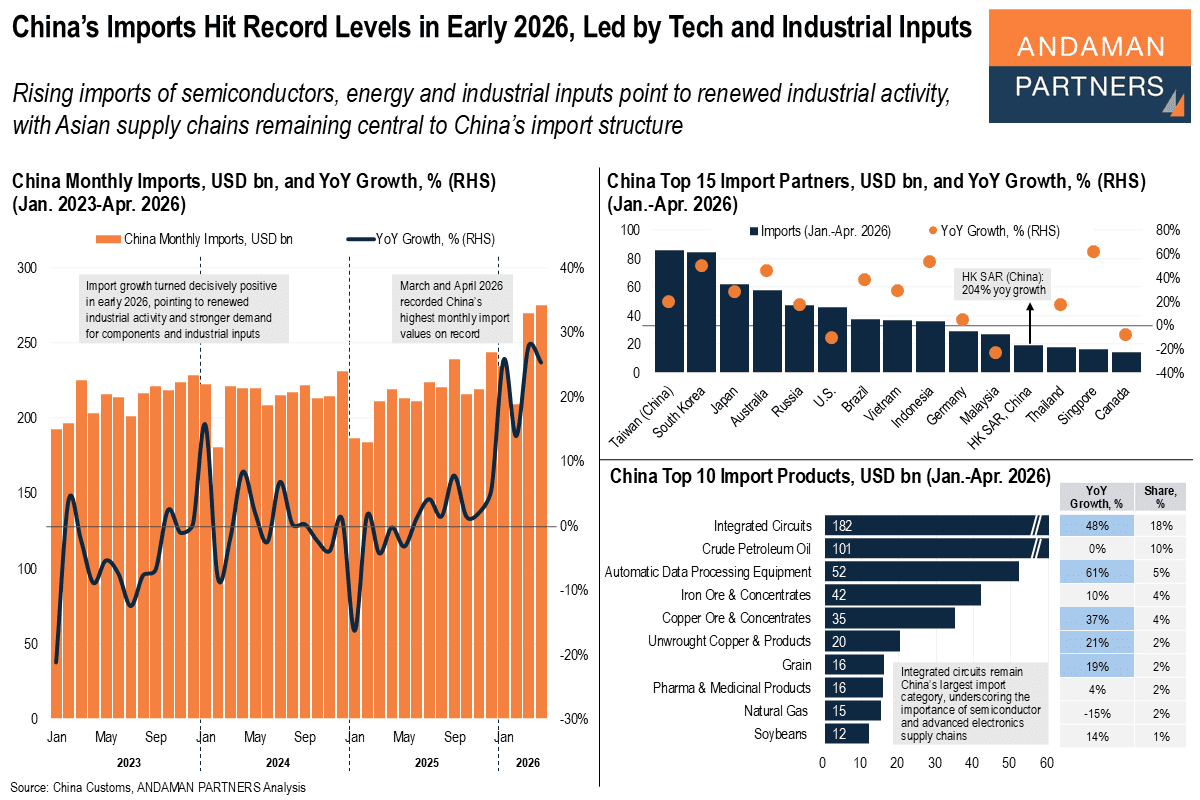

Rising imports of semiconductors, energy and industrial inputs point to renewed industrial activity.

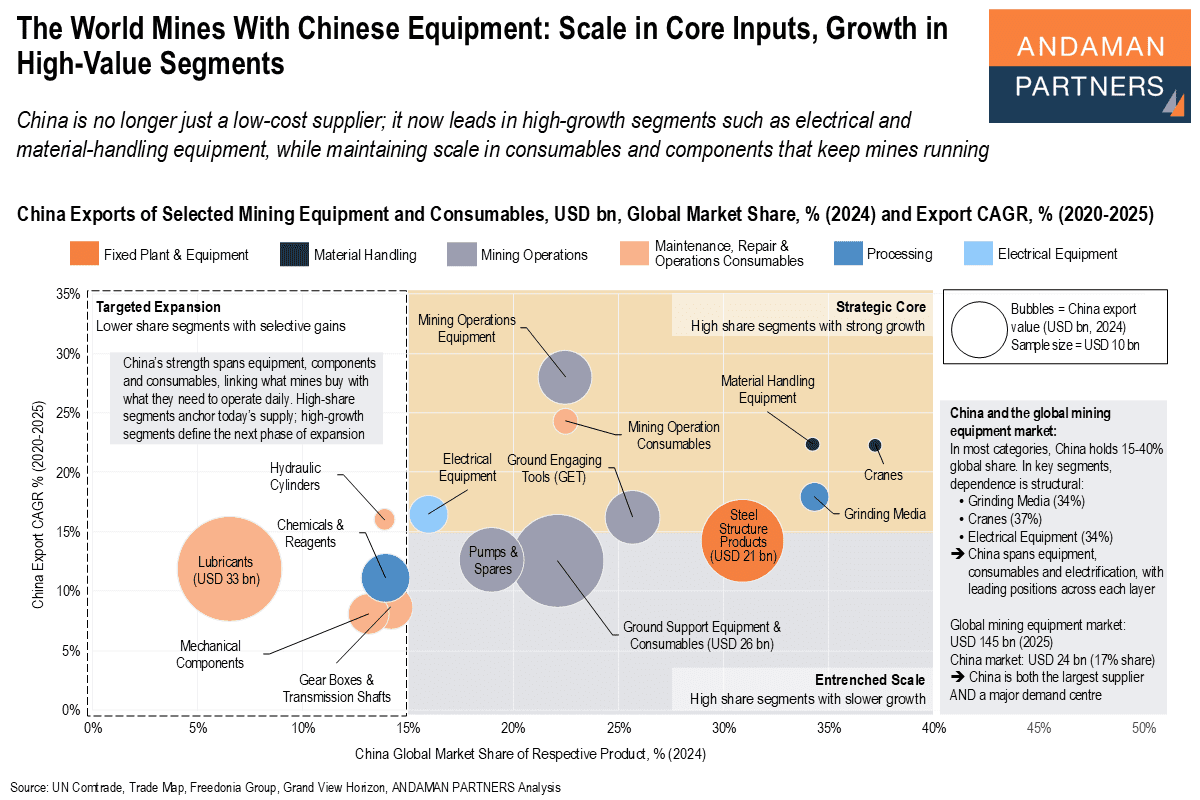

China is no longer just a low-cost supplier; it now leads in high-growth segments while maintaining scale in consumables and components.

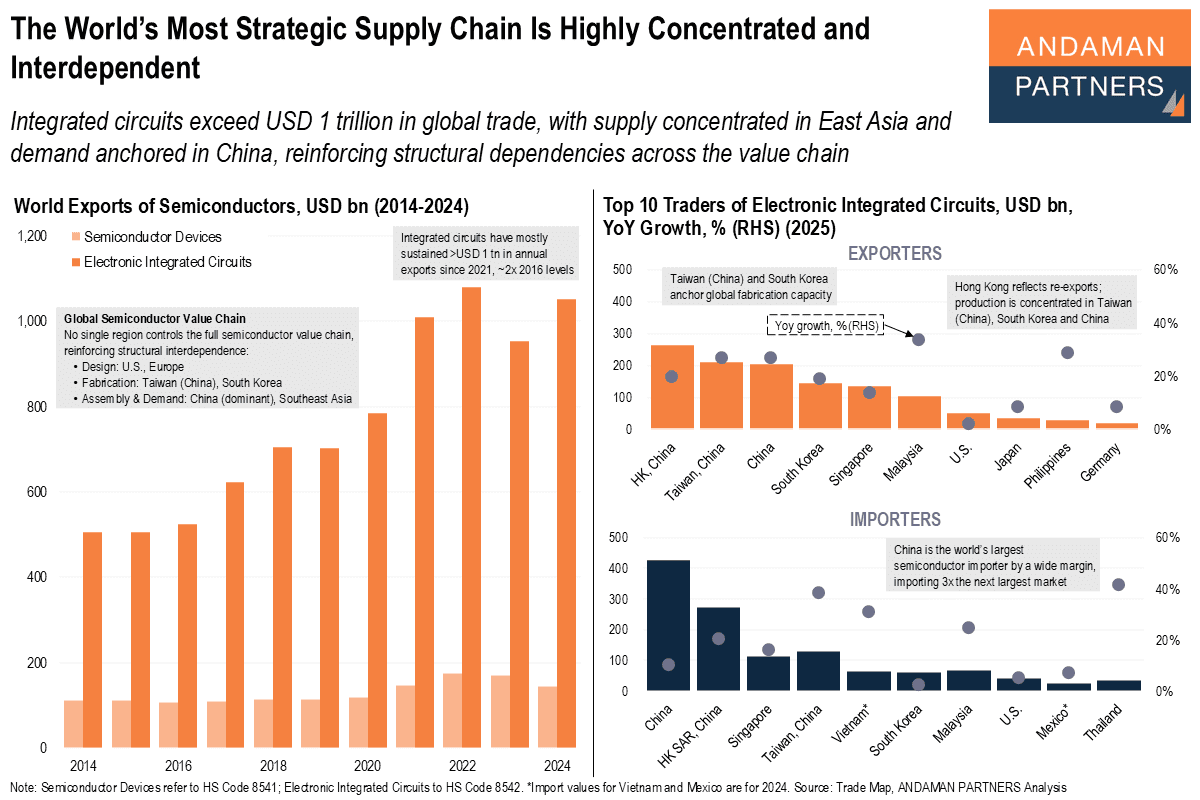

Integrated circuits exceed USD 1 trillion in global trade, with supply concentrated in Asia and demand in China, reinforcing structural dependencies.

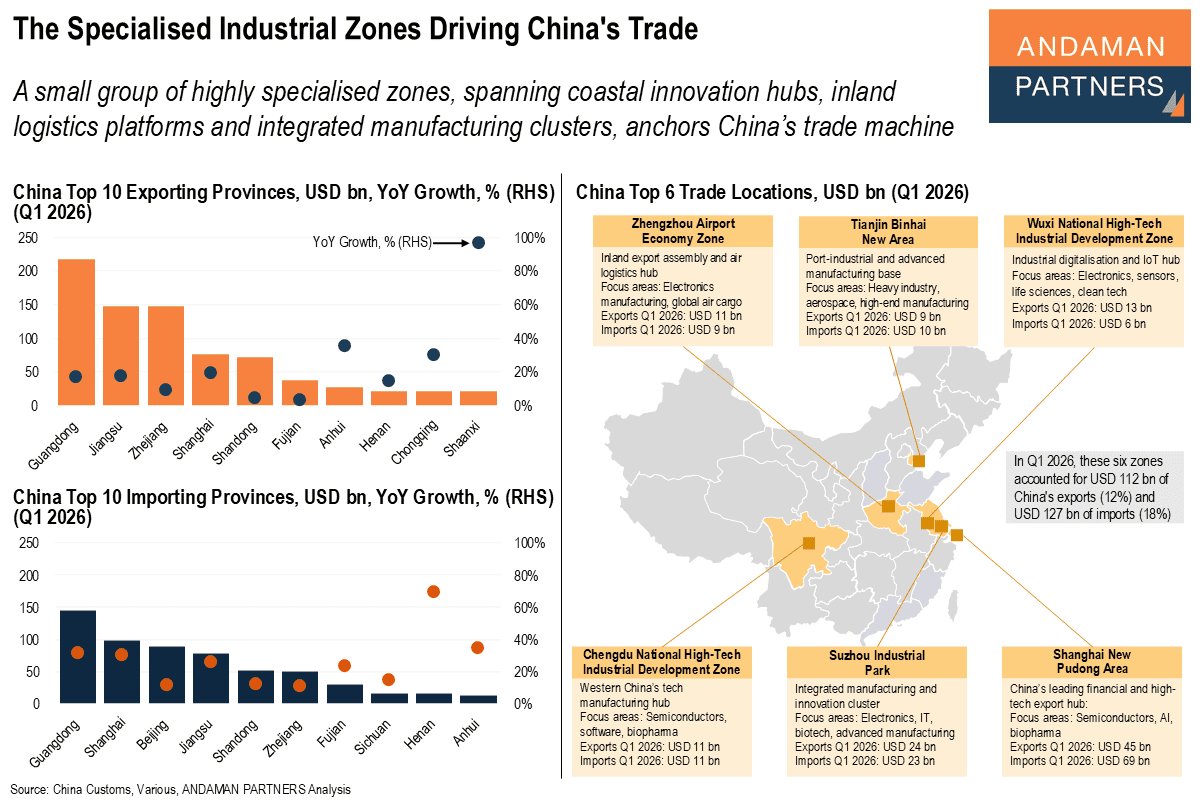

A small group of highly specialised zones anchors China’s trade machine.

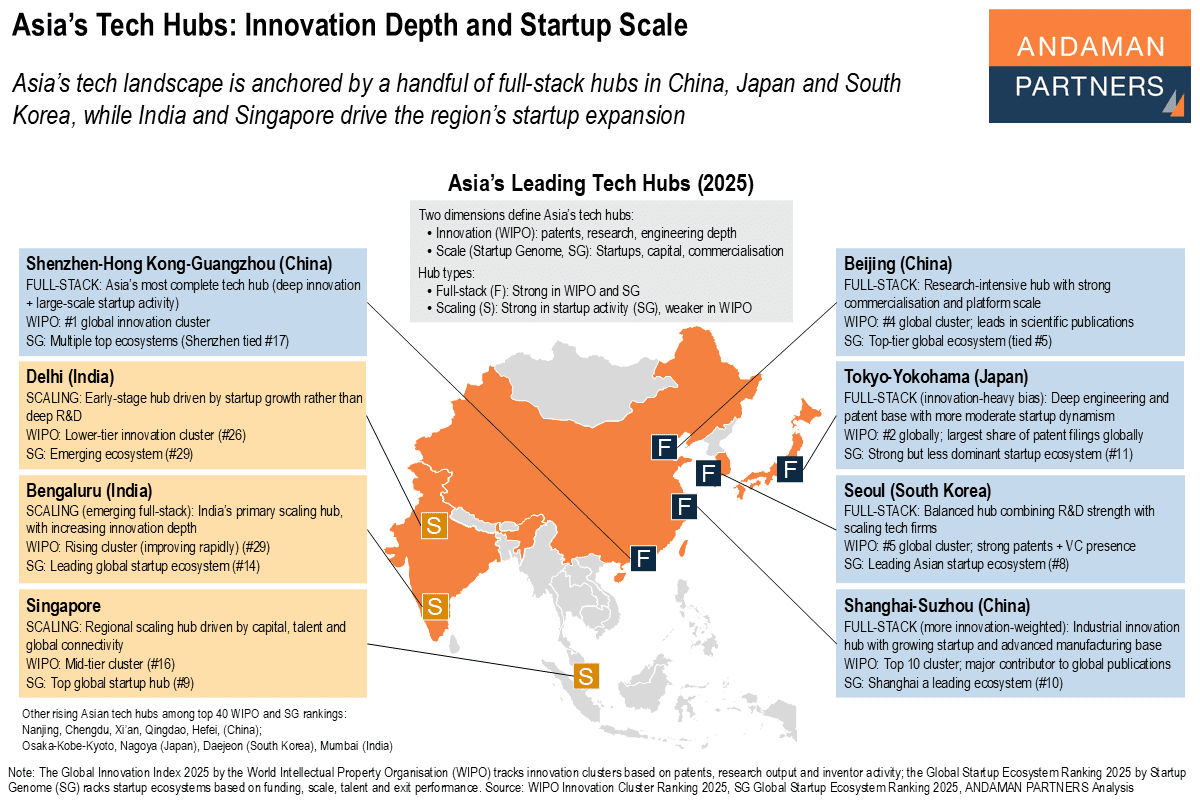

Asia’s tech landscape is anchored by a handful of full-stack hubs in China, Japan and South Korea, while India and Singapore drive startup expansion.

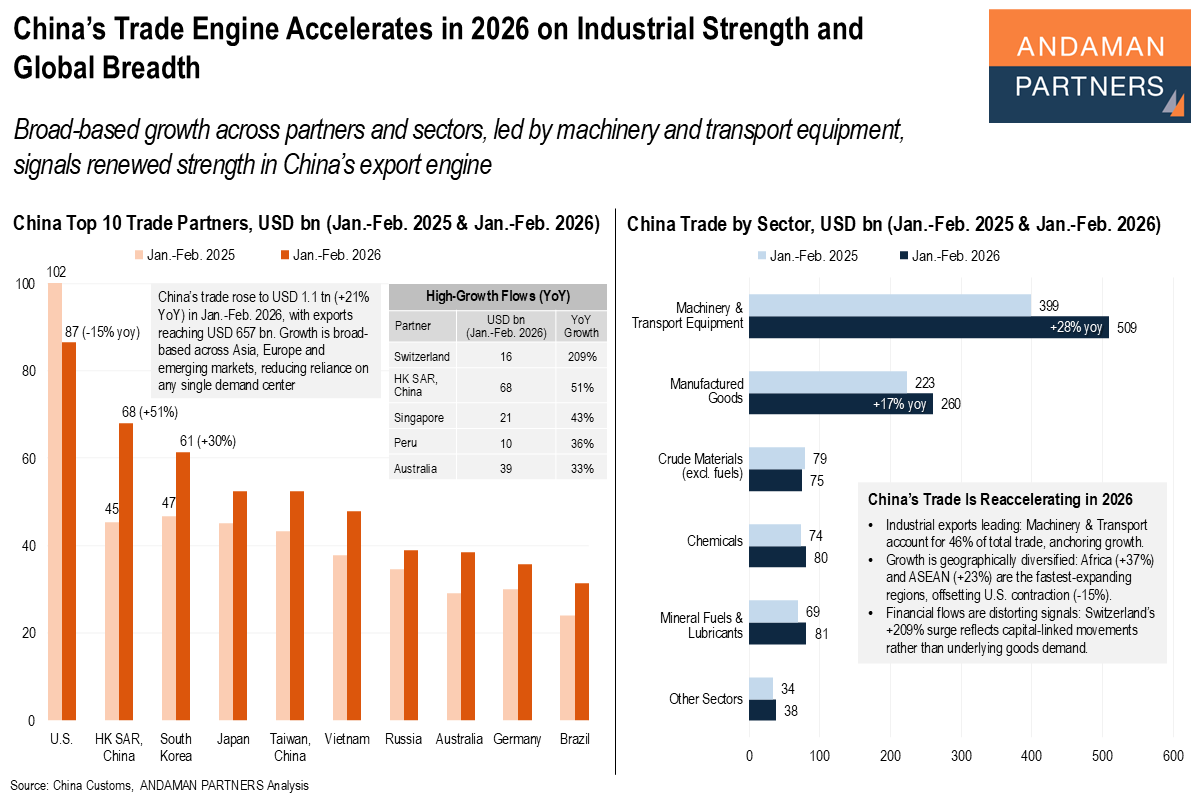

Broad-based growth across partners and sectors, led by machinery and transport equipment, signals renewed strength in China’s export engine.

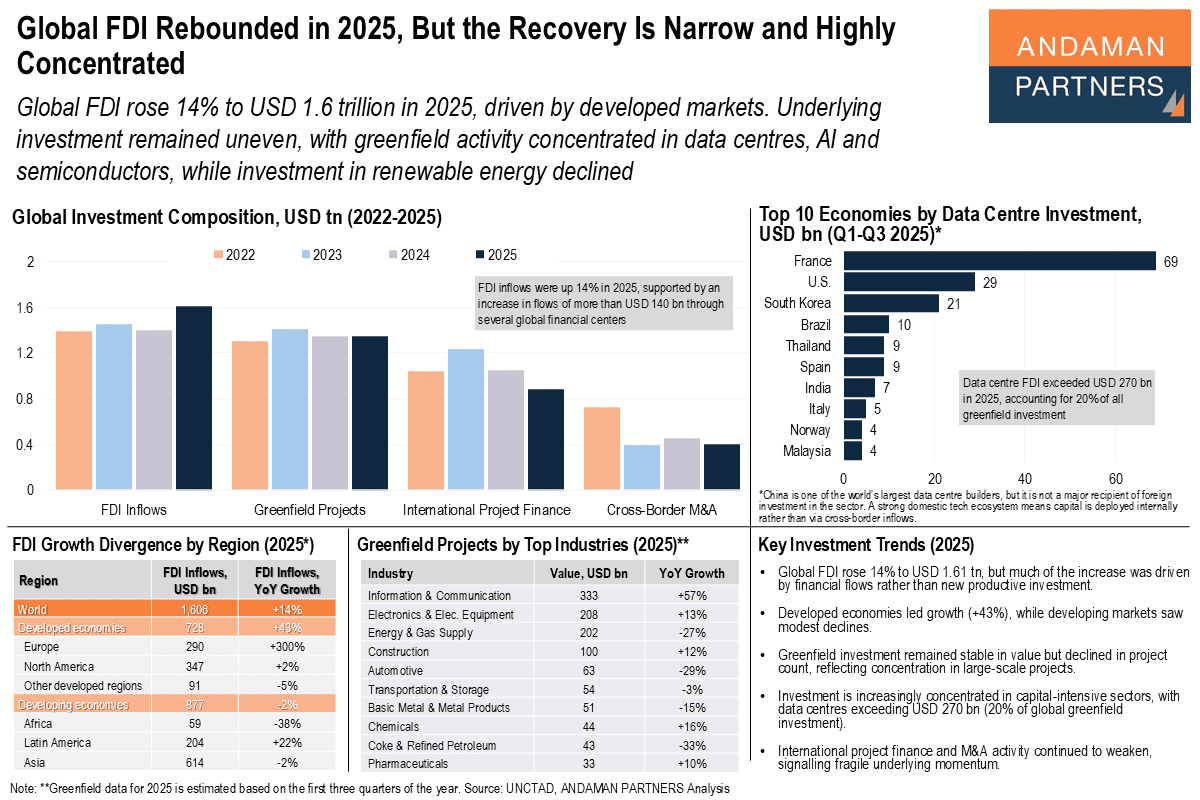

Investment remained uneven, with greenfield activity concentrated in data centres, AI and semiconductors.