The World Mines With Chinese Equipment

The World Mines With Chinese Equipment

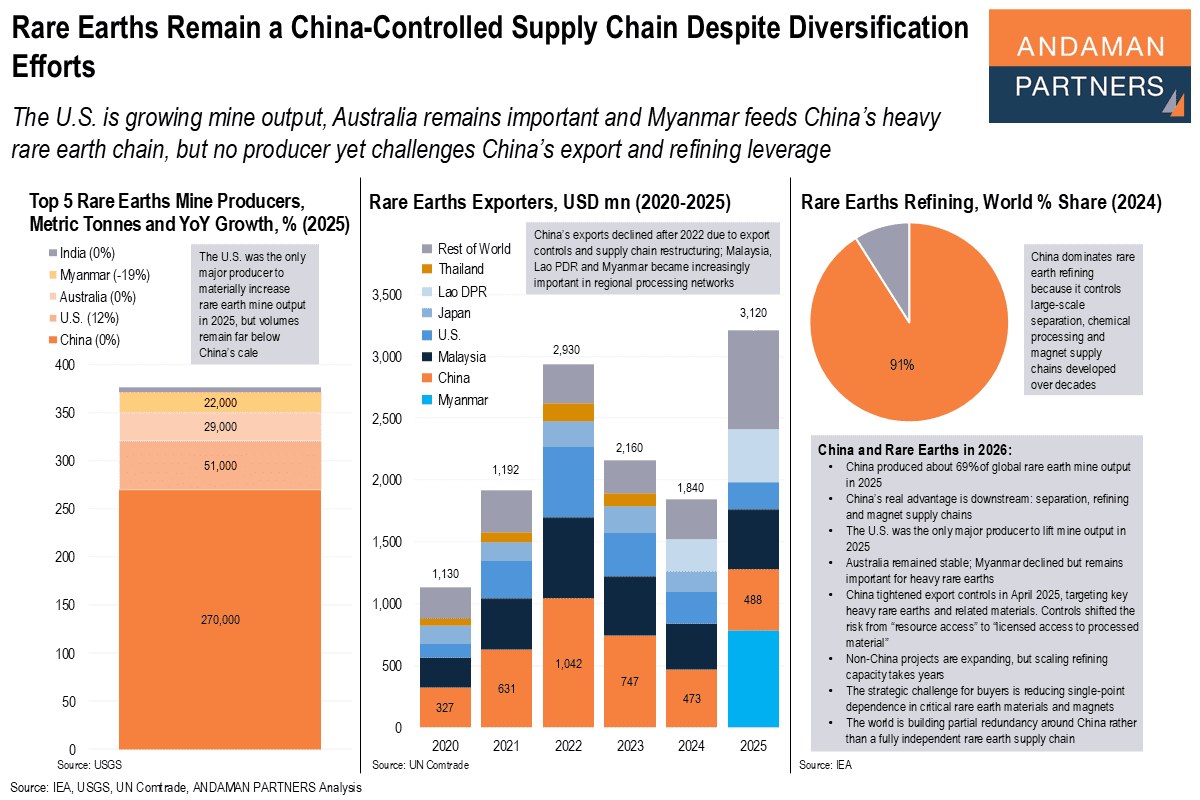

Rare Earths Supply Chain Remains China-Controlled Despite Diversification Efforts

Rare Earths Supply Chain Remains China-Controlled Despite Diversification Efforts

The U.S. is growing mine output, Australia remains important and Myanmar feeds China’s heavy rare earth chain, but no producer yet challenges China’s export and refining leverage.

Rare earth supply chains remain overwhelmingly centred on China in 2026, despite growing diversification efforts elsewhere. China accounted for roughly 69% of global mine production in 2025 and continues to dominate the far more strategic downstream stages of separation, refining and magnet manufacturing. In 2024, China accounted for 91% of global rare earth refining.

While the U.S. was the only major producer to materially increase mine output in 2025, and Australia remained an important supplier, alternative capacity is still limited relative to China’s scale. Trade flows are also shifting rather than fragmenting completely, with Malaysia, Lao PDR and Myanmar becoming increasingly important within Asia-centric processing networks linked to Chinese industry.

The broader trend is not the emergence of a fully independent global rare earth system, but the gradual development of partial redundancy around China. The strategic challenge for global manufacturers, technology firms and industrial supply chains is no longer simply access to raw materials, but exposure to highly concentrated downstream processing and export leverage.

Also by ANDAMAN PARTNERS:

- Nexus of the Mining World: China’s Share of Global Processing and Exports of Strategic Minerals and Metals

- Nexus of the Mining World: China’s Share of Global Reserves and Production of Strategic Minerals and Metals

The World Mines With Chinese Equipment: Scale in Core Inputs, Growth in High-Value Segments

ANDAMAN PARTNERS supports international business ventures and growth. We help launch global initiatives and accelerate successful expansion across borders. If your business, operations or project requires cross-border support, contact connect@andamanpartners.com.