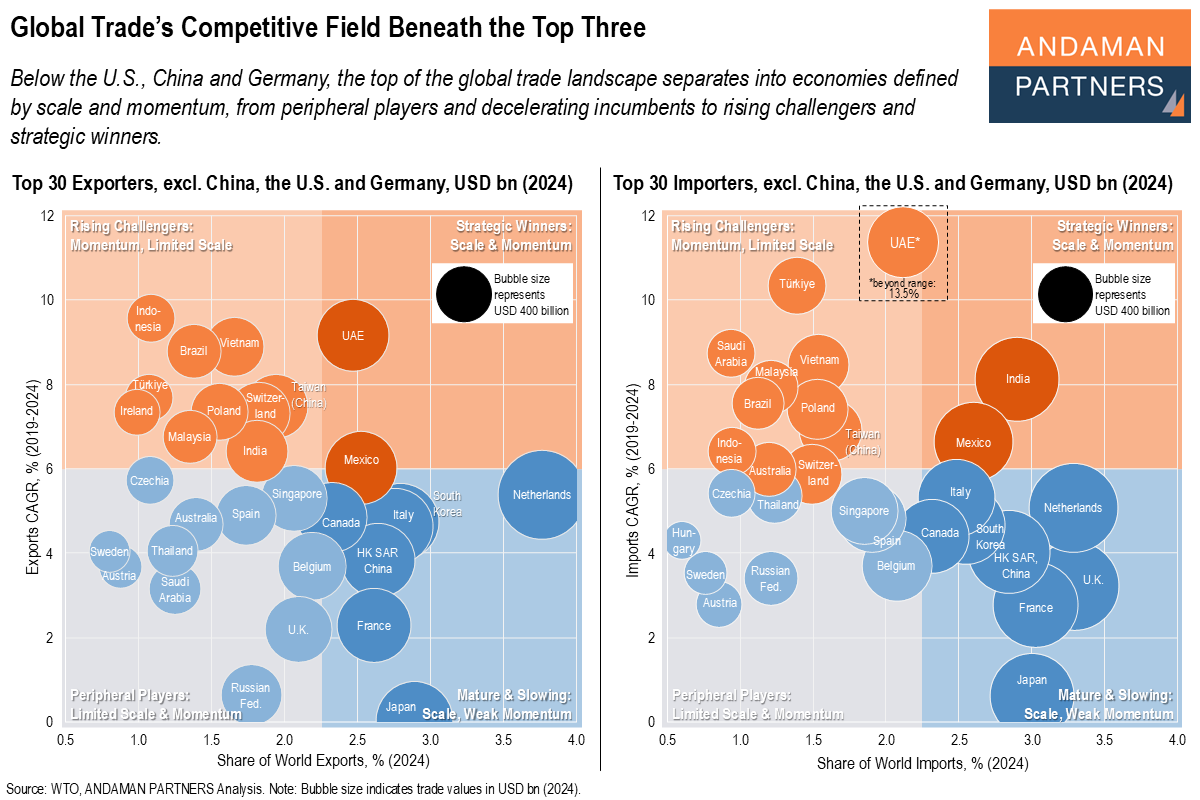

At first glance, global trade is dominated by the familiar heavyweights. But once the U.S., China and Germany are set aside, the competitive field beneath the system anchors comes into view. The top 30 economies below the top three define where trade momentum is receding and emerging, and where scale is eroding and building.

The world’s next tier of trading economies can be organised along two decisive dimensions: scale, measured by share of global trade, and momentum, captured through multi-year trade growth. Together, these two dimensions separate economies into four distinct strategic positions, each with very different implications for corporates, investors and policymakers.

Strategic Winners: India, Mexico, UAE

At the top are the Strategic Winners. These economies combine meaningful scale with sustained trade momentum. They are not merely growing; they are compounding relevance. They increasingly act as hubs in global supply chains and demand networks, making them disproportionately important relative to their size. For companies, these are markets and sourcing locations that warrant long-term commitment rather than tactical engagement.

Rising Challengers: Brazil, Indonesia, Ireland, Malaysia, Poland, Switzerland, Taiwan (China), Türkiye, Vietnam

The Rising Challengers economies lack scale today, but their momentum is unmistakable. Over time, this group often supplies the next generation of trade hubs, manufacturing platforms or regional gateways. Ignoring them because they are still relatively small is a common strategic error, particularly when trade growth, not current share, determines future positioning.

Mature & Slowing: Canada, France, Hong Kong SAR (China), Italy, Japan, Netherlands, South Korea

Economies in the Mature & Slowing category retain substantial trade weight, yet their growth lags that of their peers. This does not imply decline, but it does signal diminishing marginal relevance. For CEOs, this quadrant raises questions around exposure, optimisation and resilience rather than expansion.

Peripheral Players: Australia, Austria, Belgium, Czechia, Hungary, Russian Federation, Saudi Arabia, Singapore, Spain, Sweden, Thailand, U.K.

The Peripheral Players economies combine limited scale with weak momentum. From a strategic perspective, these markets matter less for global trade decisions and can potentially be deprioritised.

Beyond the top three economies, global trade is not flat or uniform; it is sorting itself into winners, challengers and laggards, and the dividing line is no longer geography or income level, but the interaction of scale and sustained momentum.