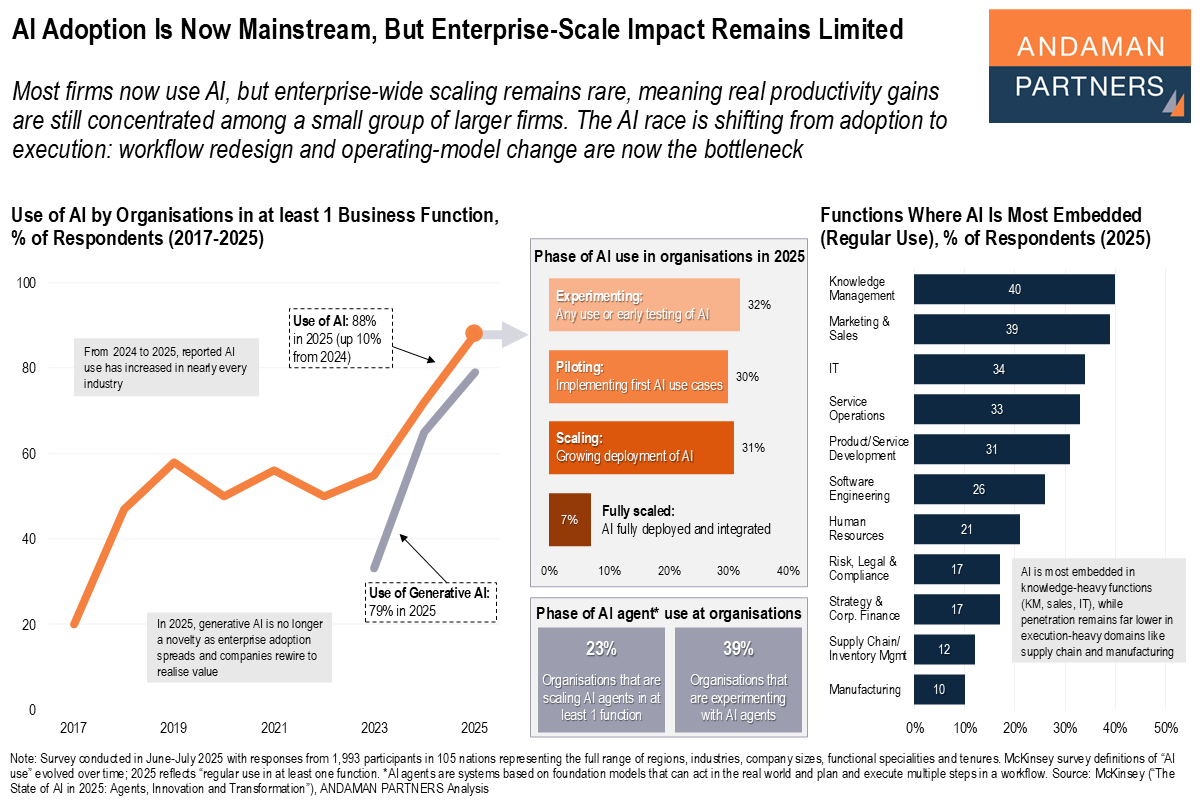

AI Adoption Is Now Mainstream, But Enterprise-Scale Impact Remains Limited

Most firms now use AI, but enterprise-wide scaling remains rare, meaning productivity gains are concentrated in a small group of larger firms.

Most firms now use AI, but enterprise-wide scaling remains rare, meaning productivity gains are concentrated in a small group of larger firms.

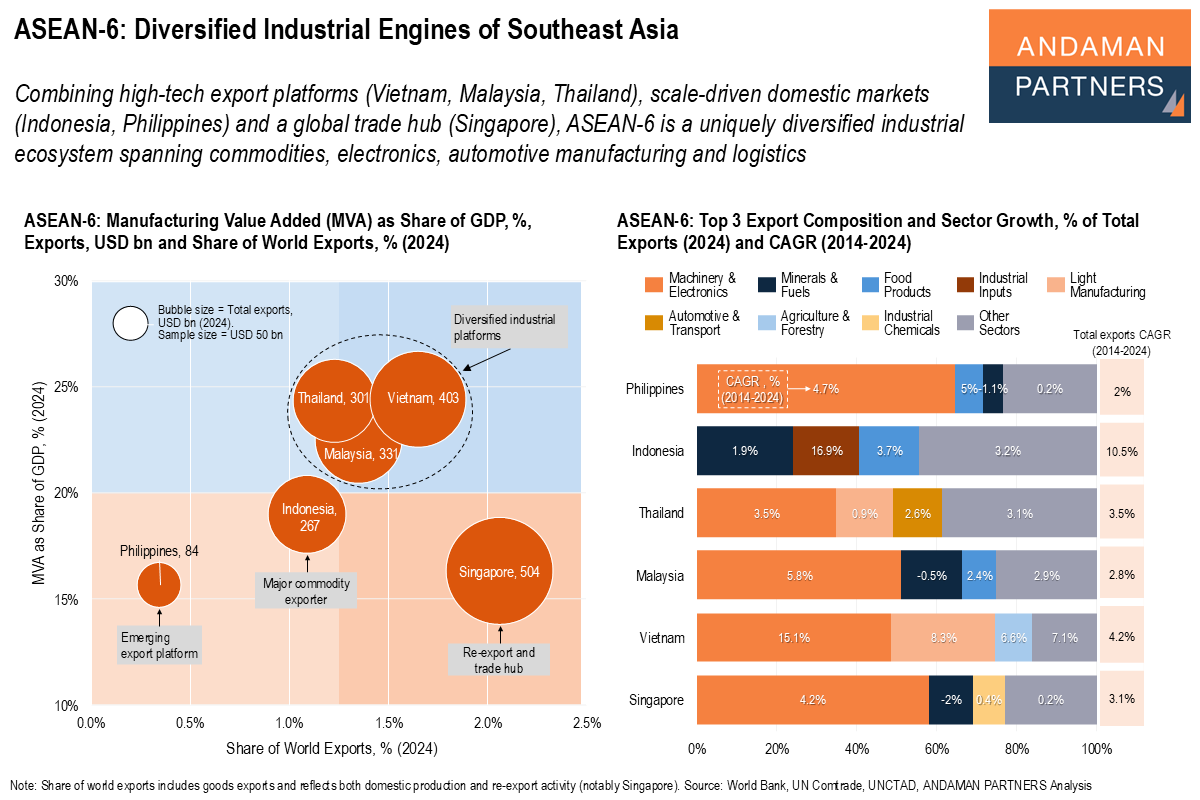

Combining high-tech export platforms, scale-driven domestic markets and a global trade hub, ASEAN-6 is a uniquely diversified industrial ecosystem.

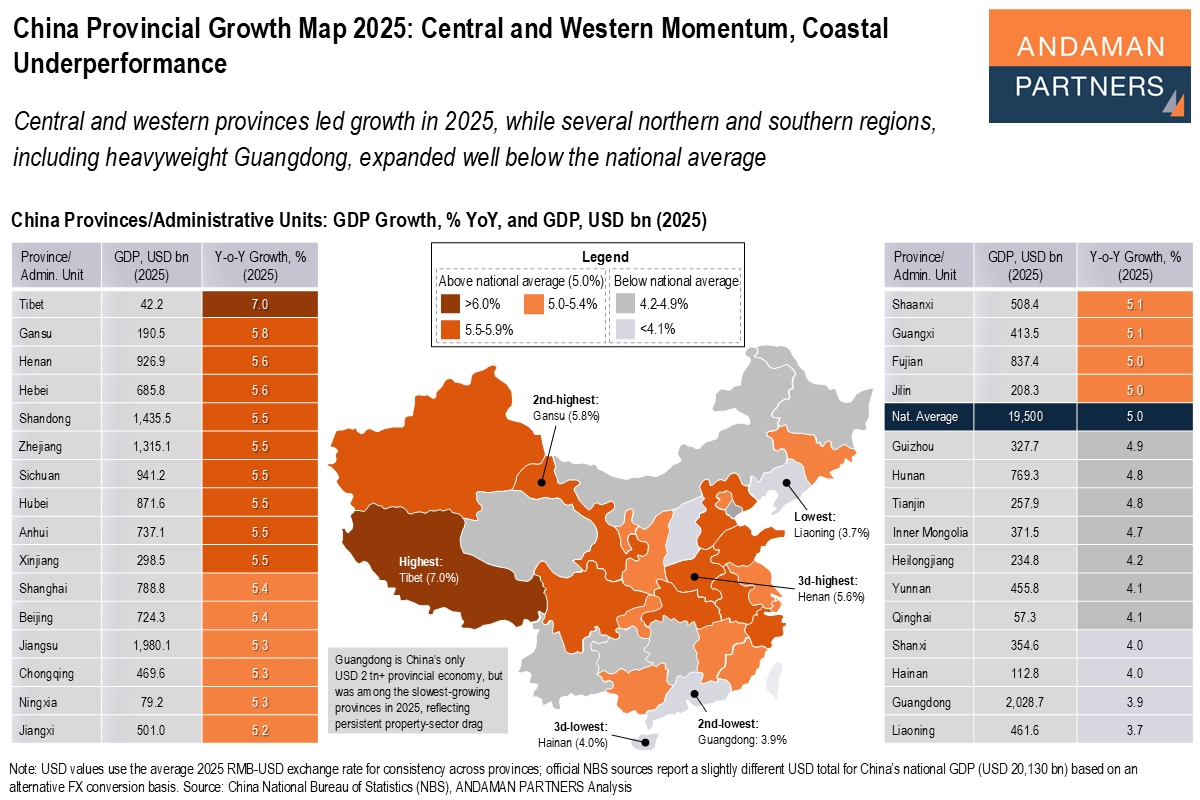

Central and western provinces led growth in 2025, while several northern and southern regions expanded well below the national average.

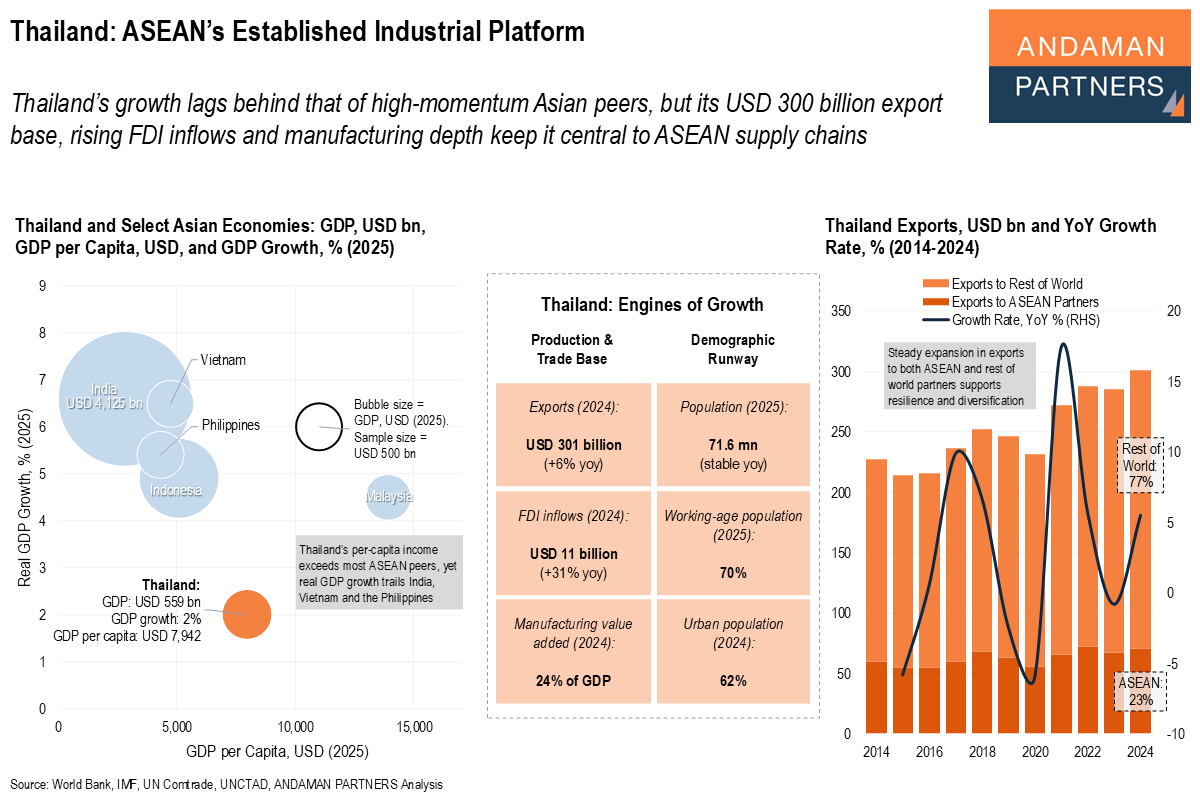

Thailand’s USD 300 billion export base, rising FDI inflows and manufacturing depth keep it central to ASEAN supply chains.

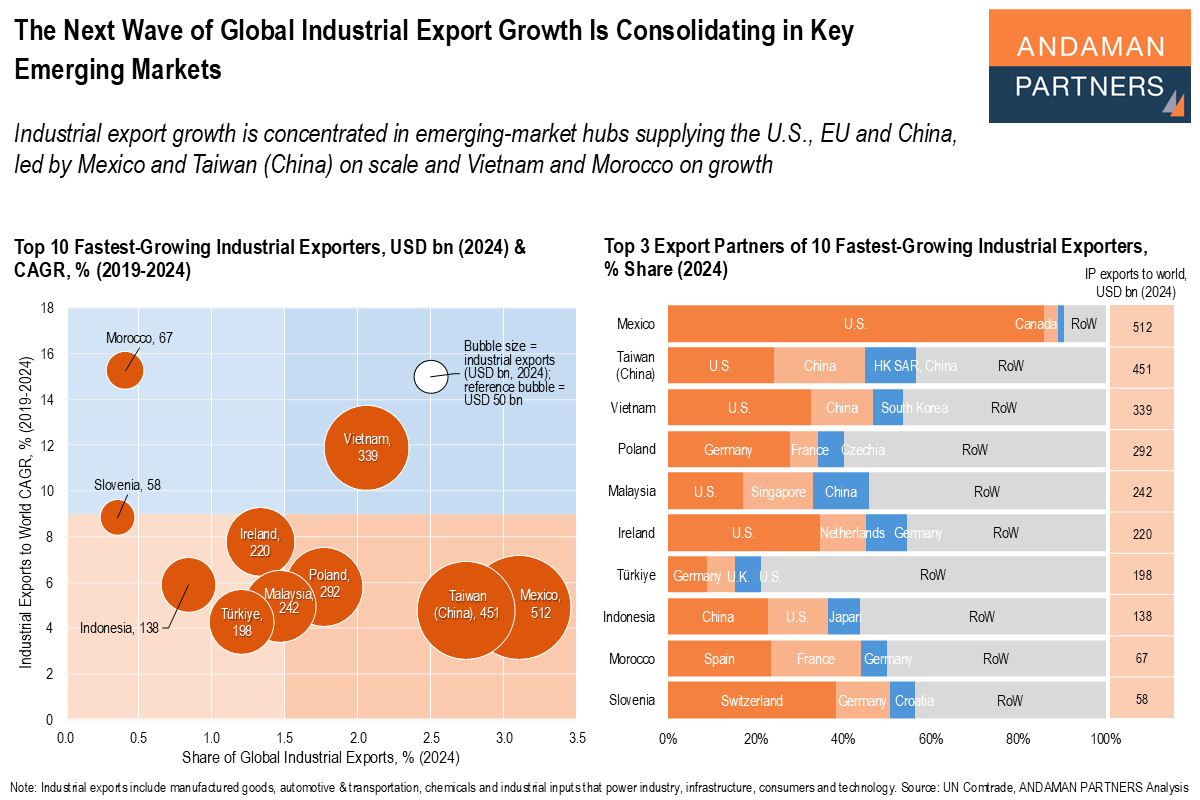

Industrial export growth is concentrated in emerging-market hubs supplying the U.S., EU and China, led by Mexico and Taiwan (China).

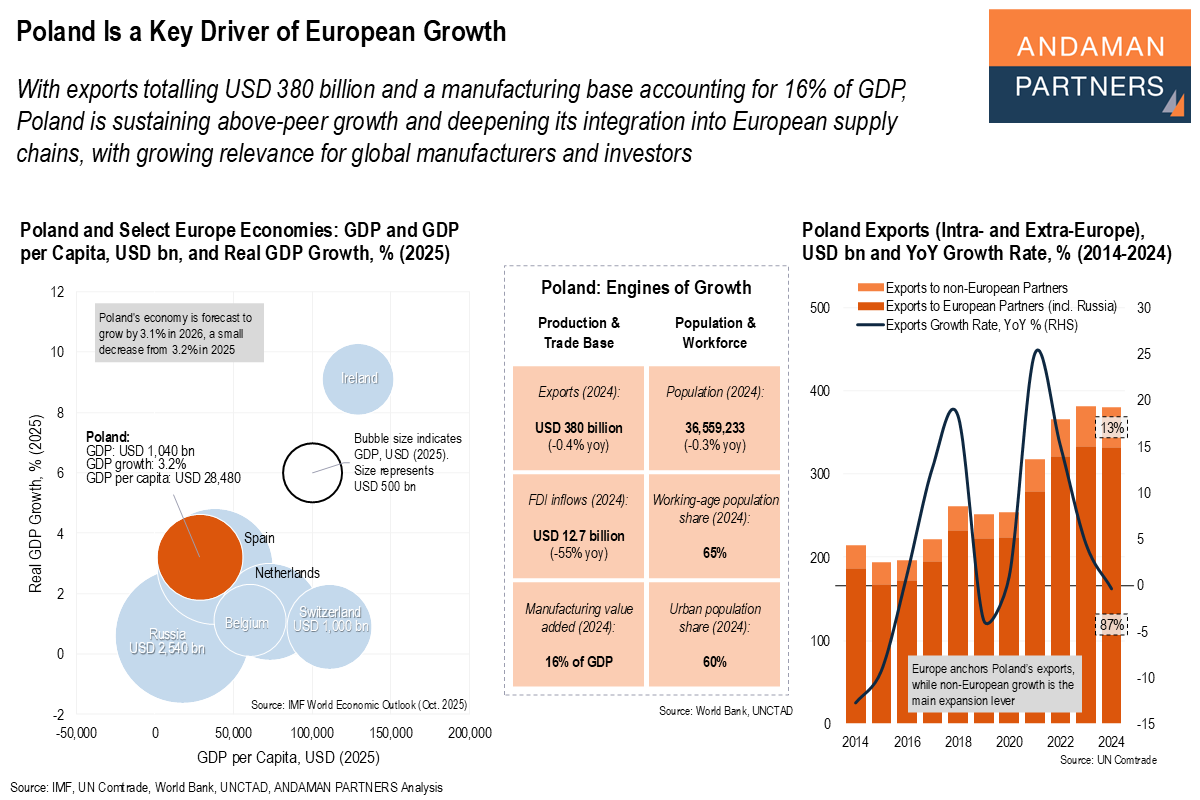

Poland is sustaining above-peer growth and deepening its integration into European supply chains.

Mexico, Vietnam, Thailand and India anchor export volumes to China, the EU and the U.S., while India stands out for the fastest growth.

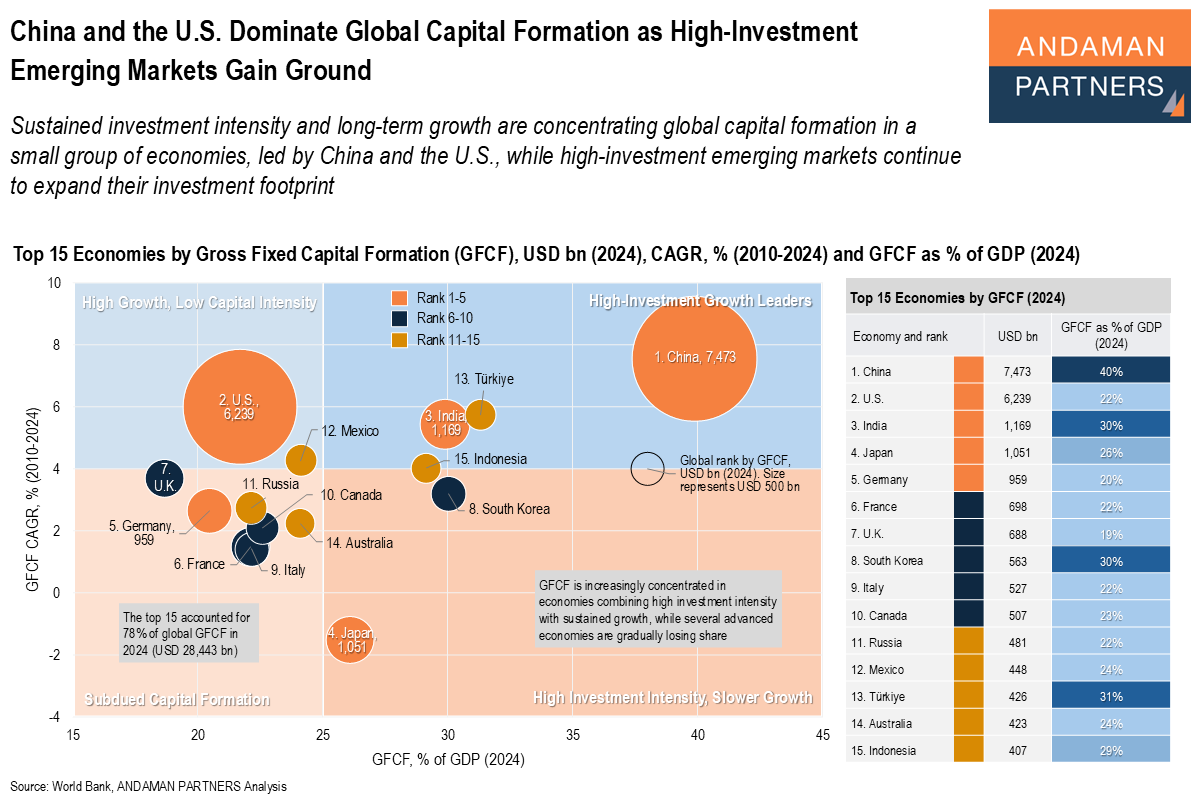

Sustained investment intensity and long-term growth are concentrating global capital formation in a small group of economies, led by China and the U.S.

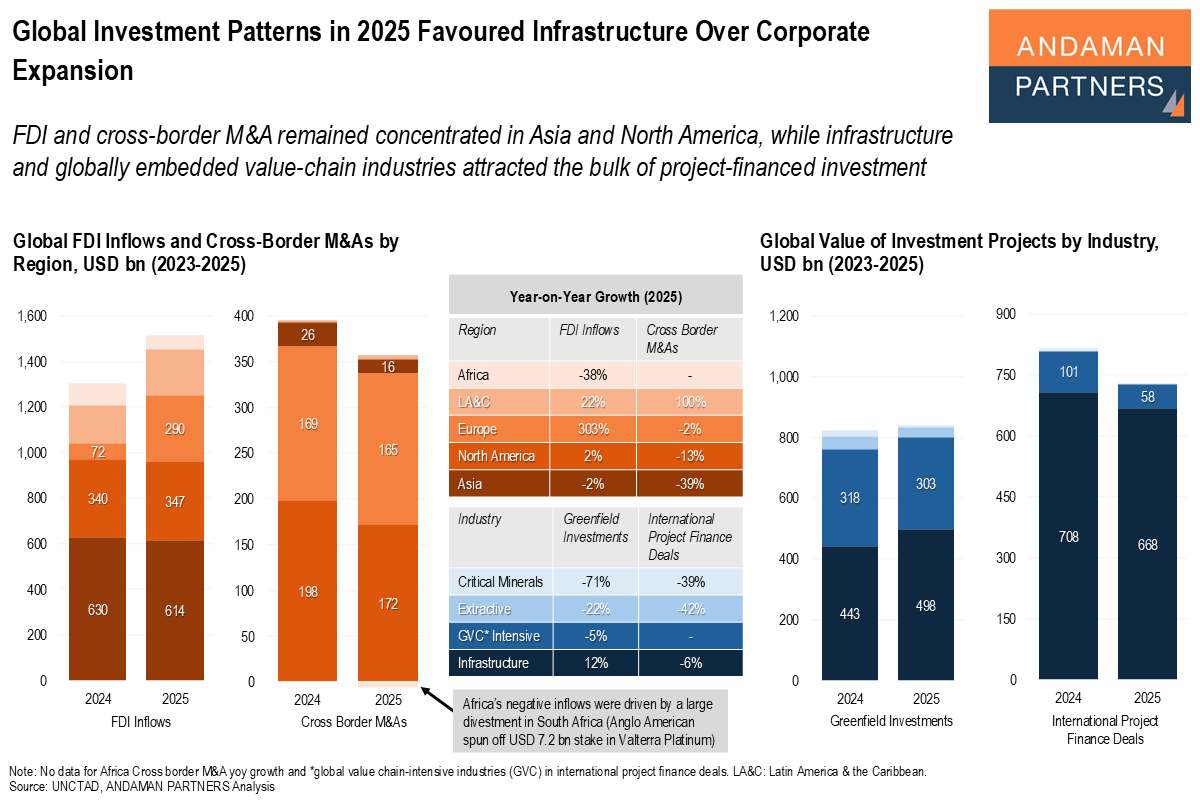

FDI and M&A remained concentrated in Asia and North America, while infrastructure attracted the bulk of project-financed investment.

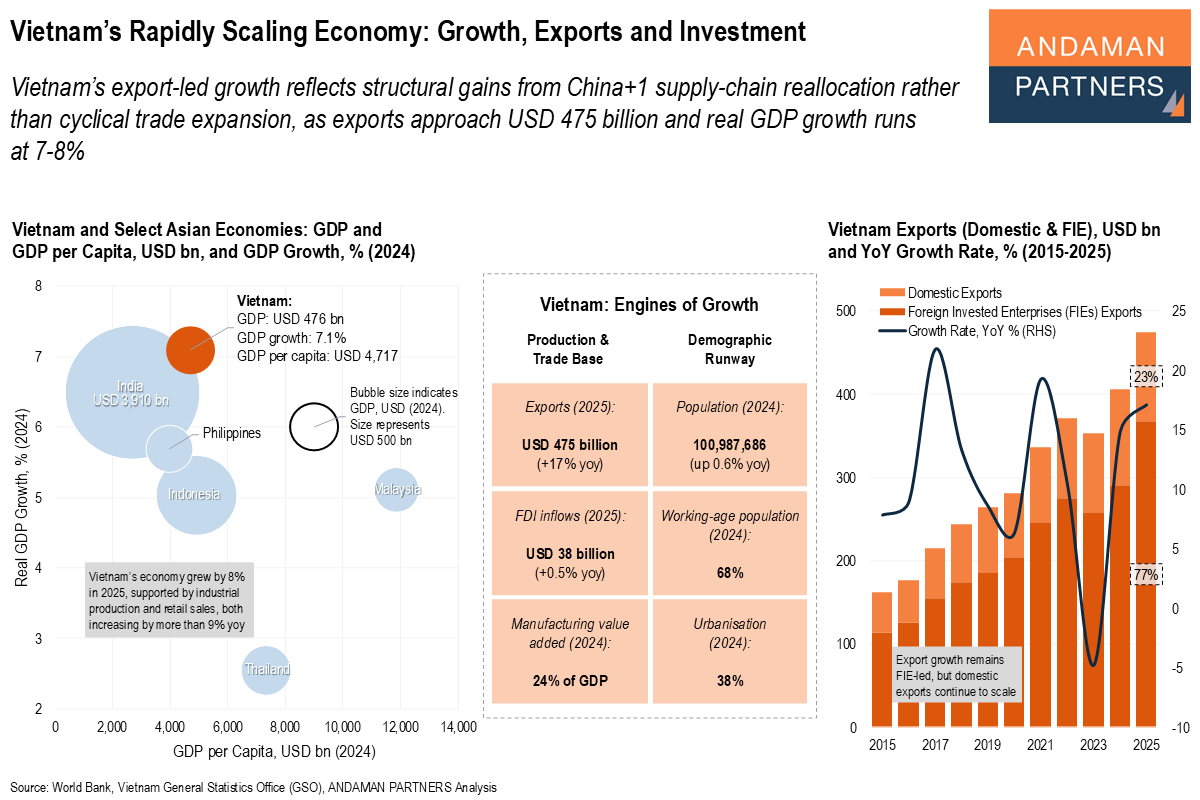

Vietnam’s export-led growth reflects structural gains from China+1 supply-chain reallocation rather than cyclical trade expansion.