Global Trade Has Recovered To Scale, With Export Power Still Concentrated

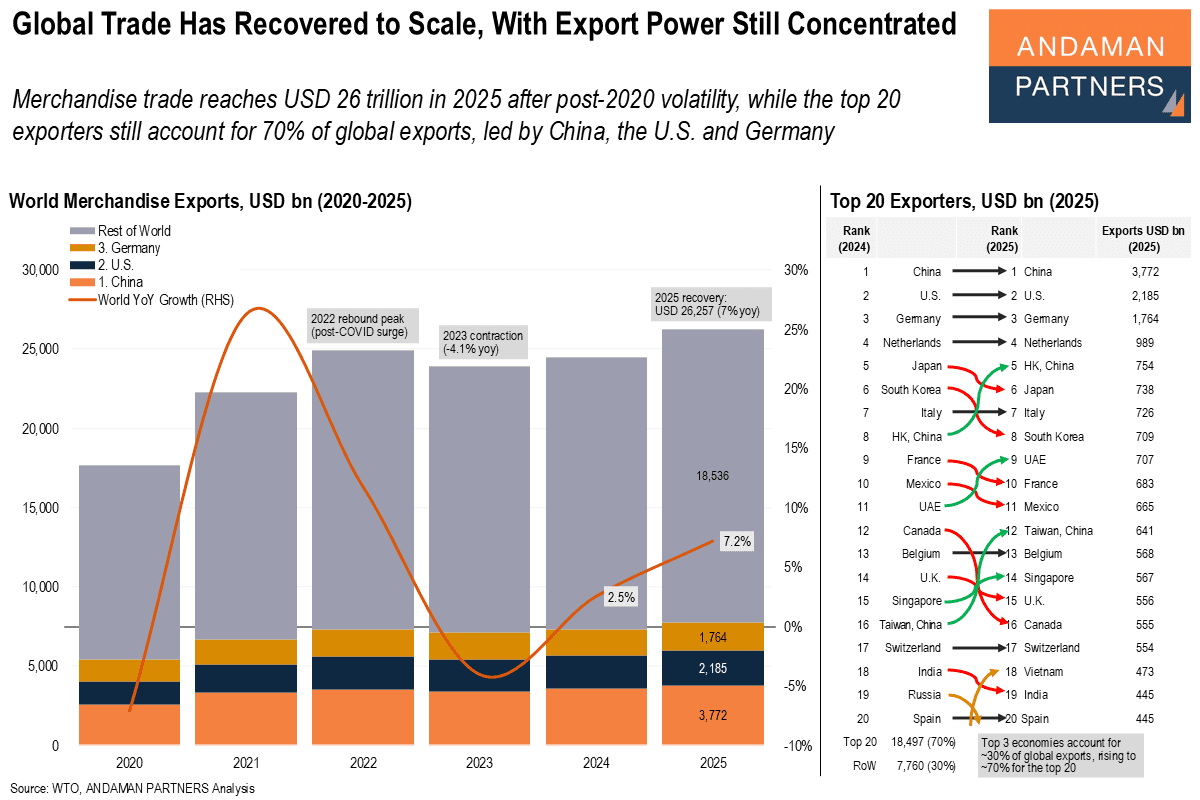

Merchandise trade reaches USD 26 trillion in 2025, while the top 20 exporters account for 70% of global exports.

Merchandise trade reaches USD 26 trillion in 2025, while the top 20 exporters account for 70% of global exports.

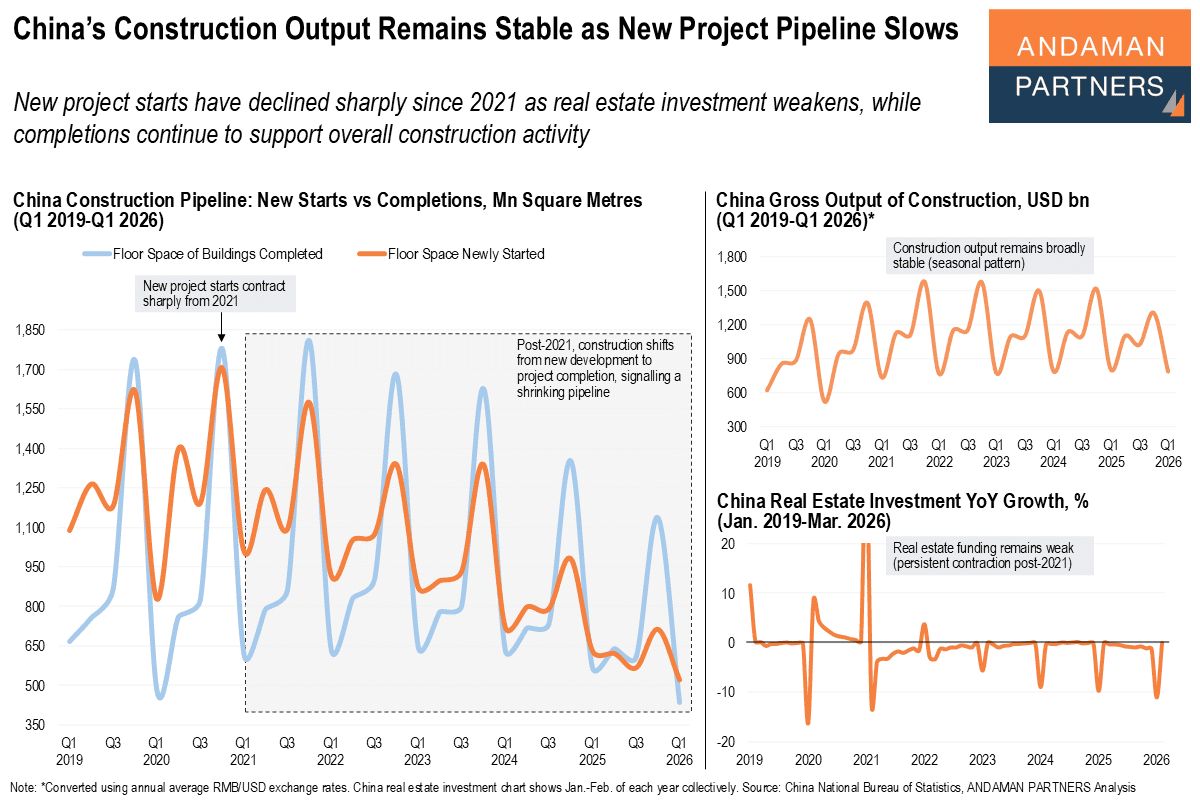

New project starts have declined sharply since 2021 as real estate investment weakens, while completions continue to support overall construction activity.

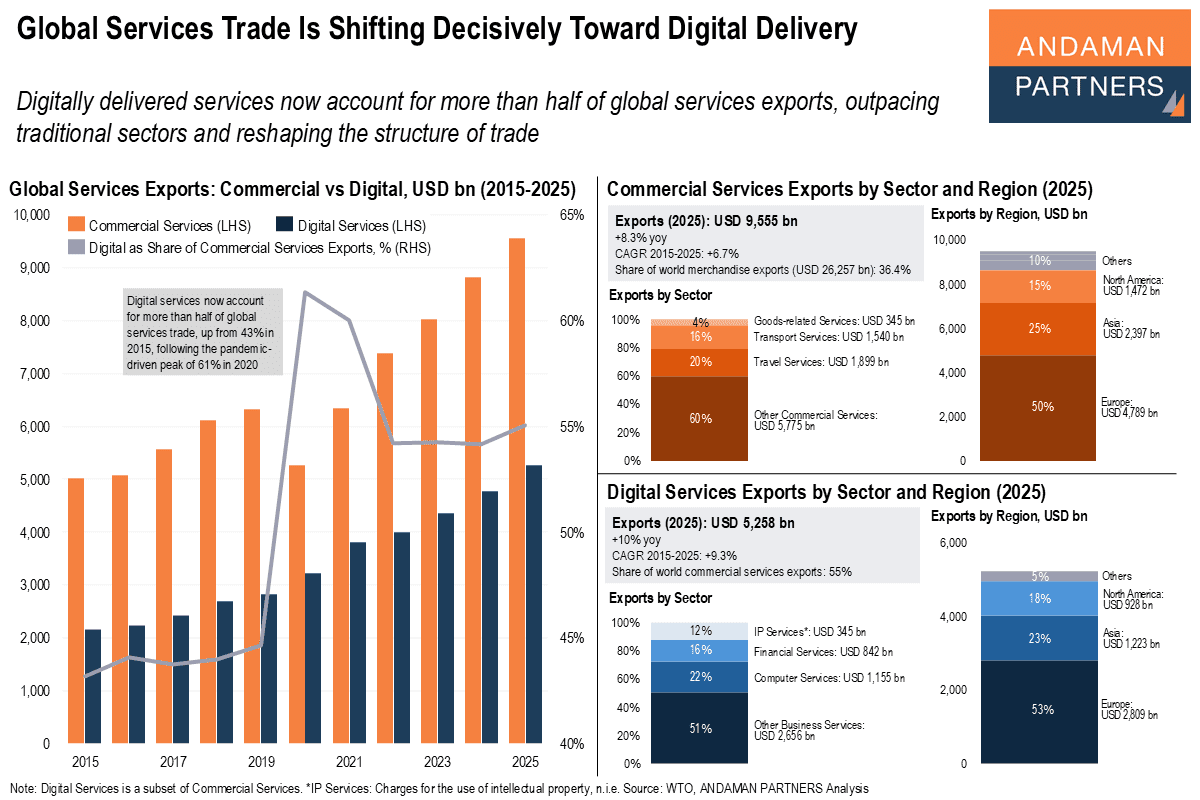

Digitally delivered services now account for more than half of global services exports, outpacing traditional sectors and reshaping the structure of trade.

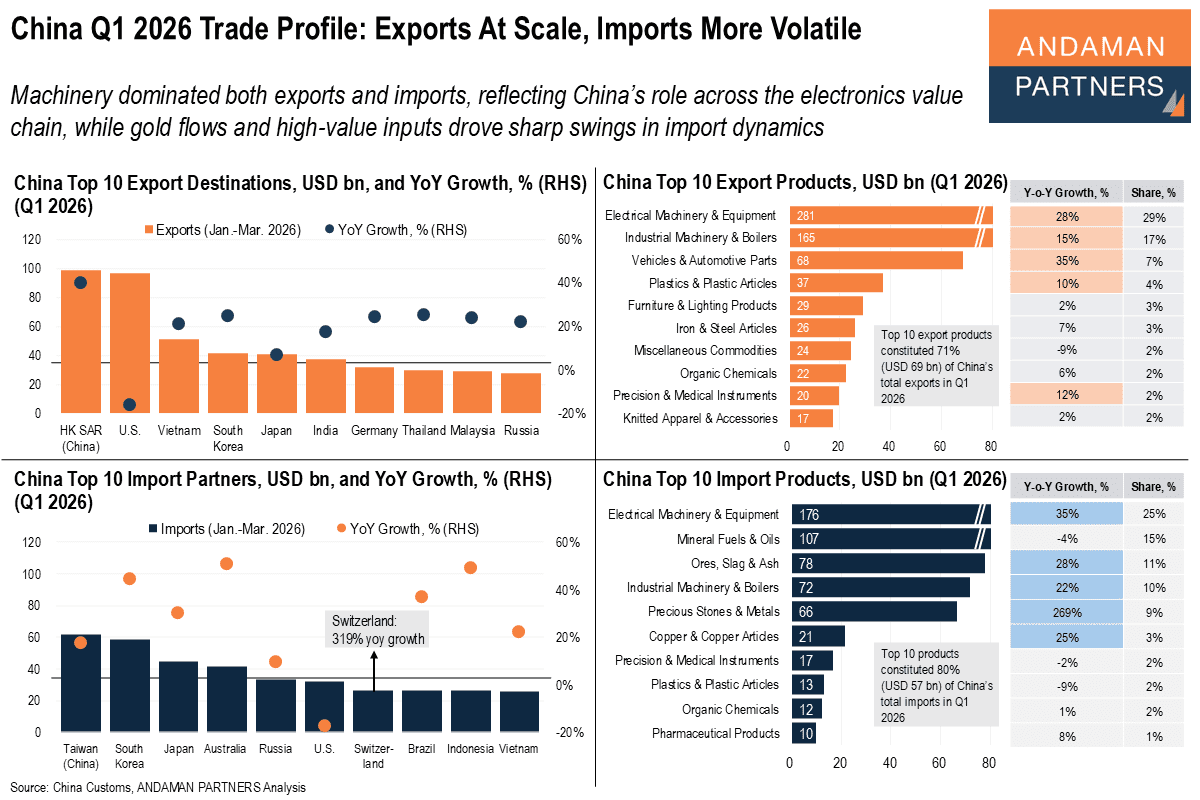

Machinery dominated exports and imports, reflecting China’s role across the electronics value chain; gold and high-value inputs drove import swings.

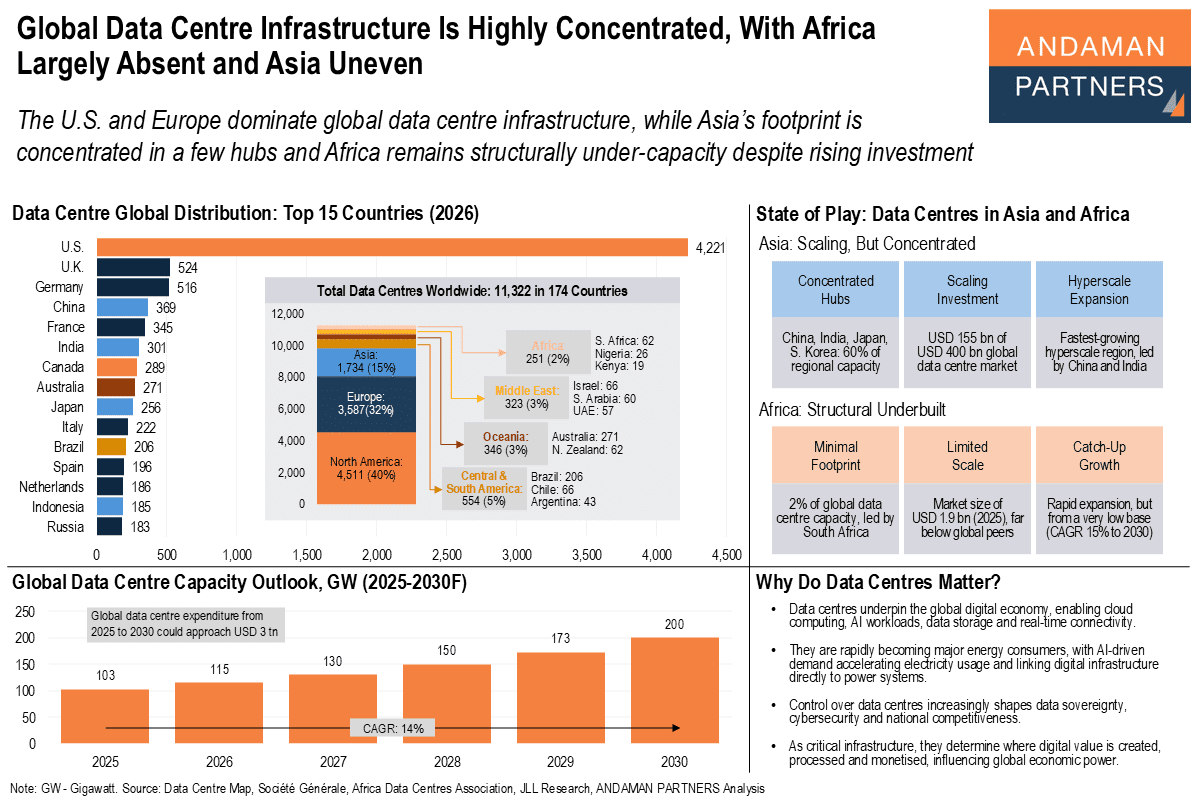

The U.S. and Europe dominate global data centre infrastructure, while Asia’s footprint is concentrated in a few hubs

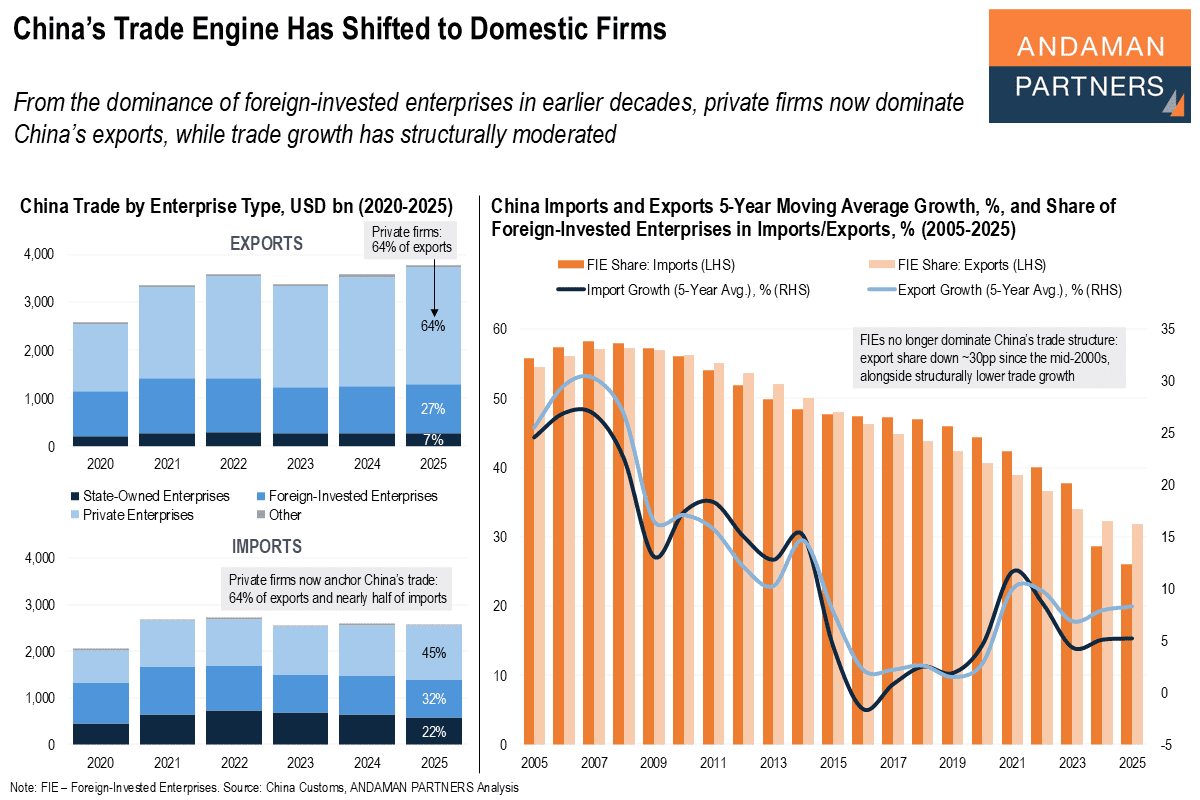

Private firms now dominate China’s exports, while trade growth has structurally moderated.

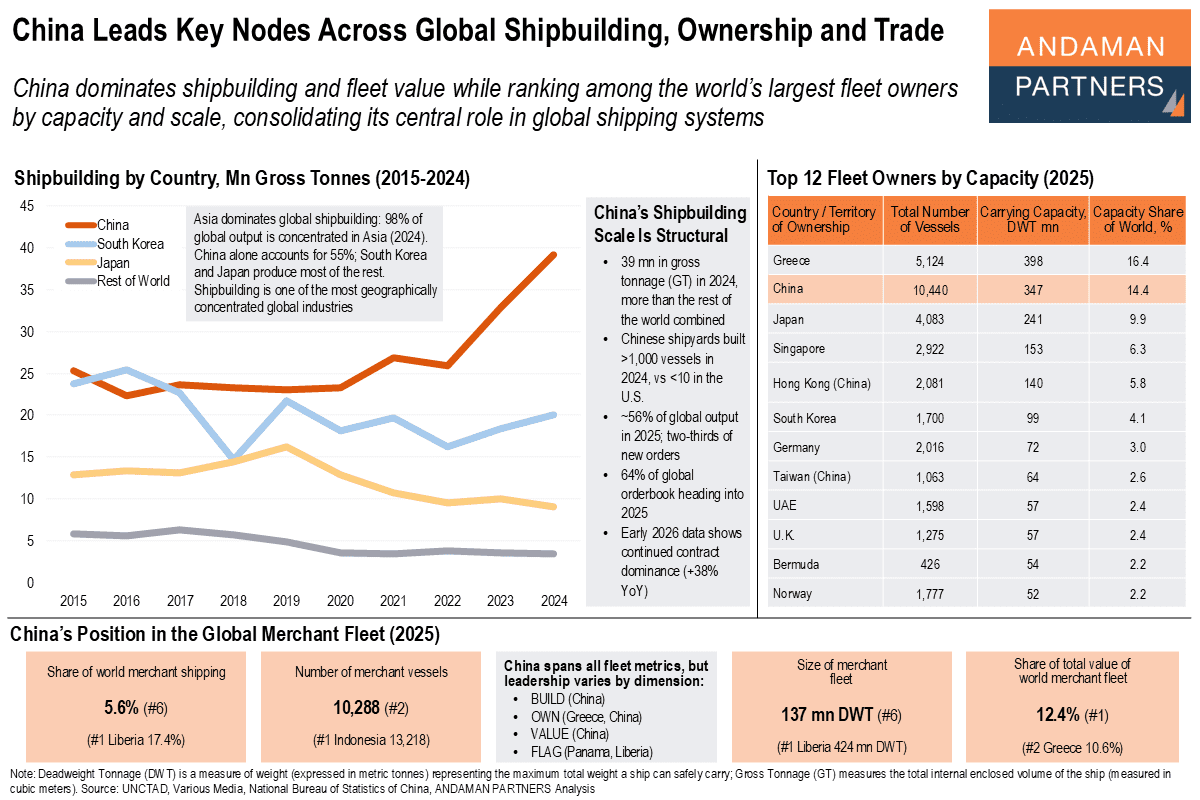

China dominates shipbuilding and fleet value while ranking among the world’s largest fleet owners by capacity and scale.

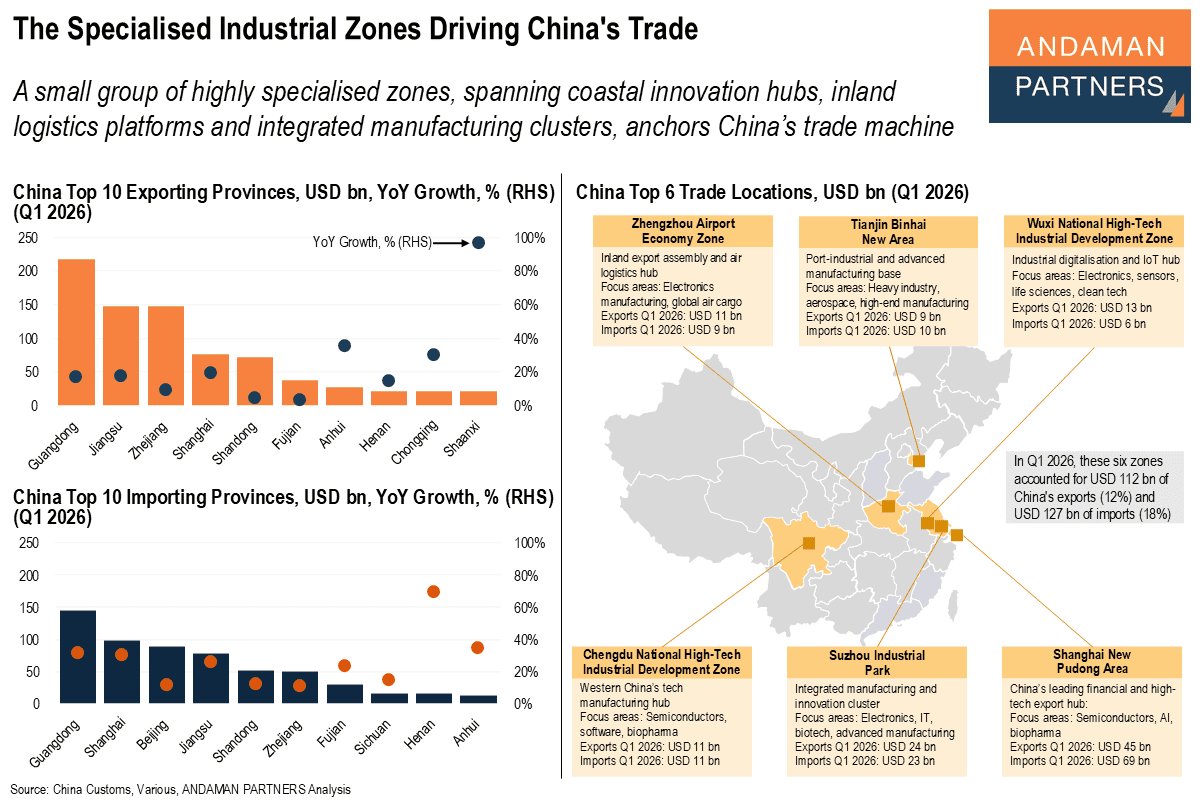

A small group of highly specialised zones anchors China’s trade machine.

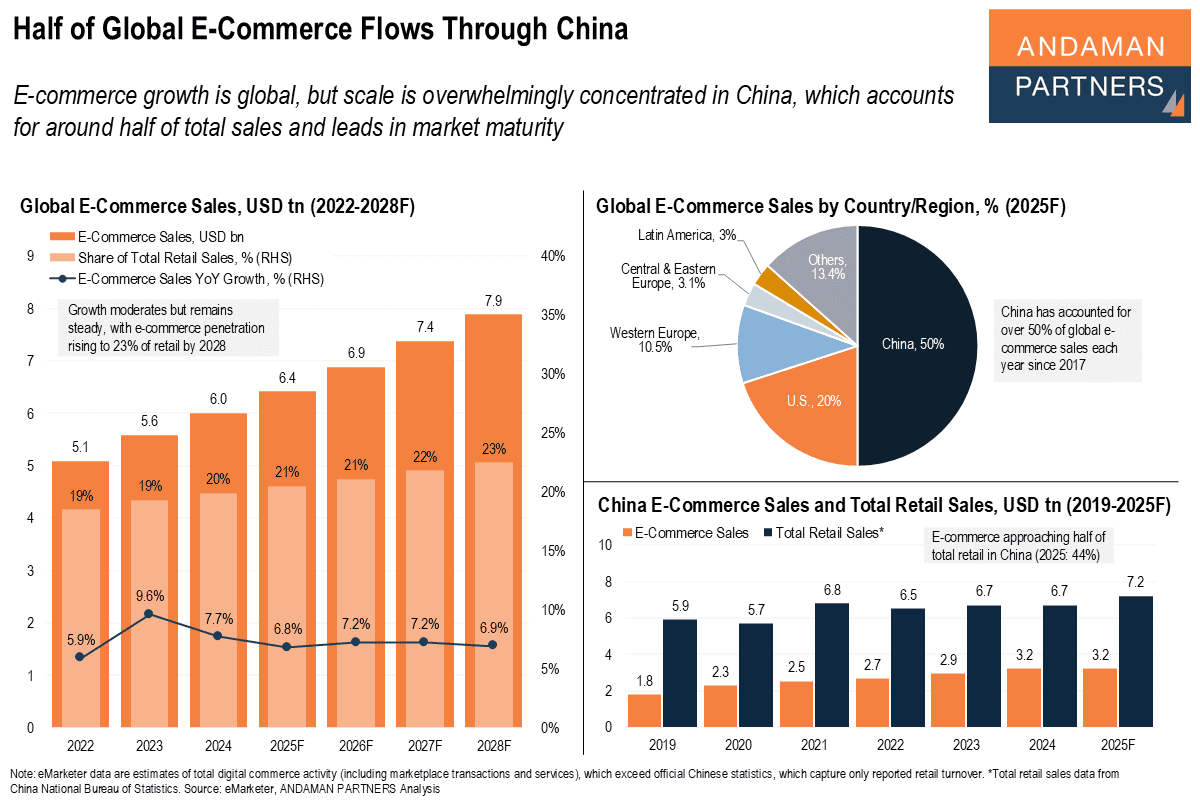

E-commerce growth is global, but scale is overwhelmingly concentrated in China.

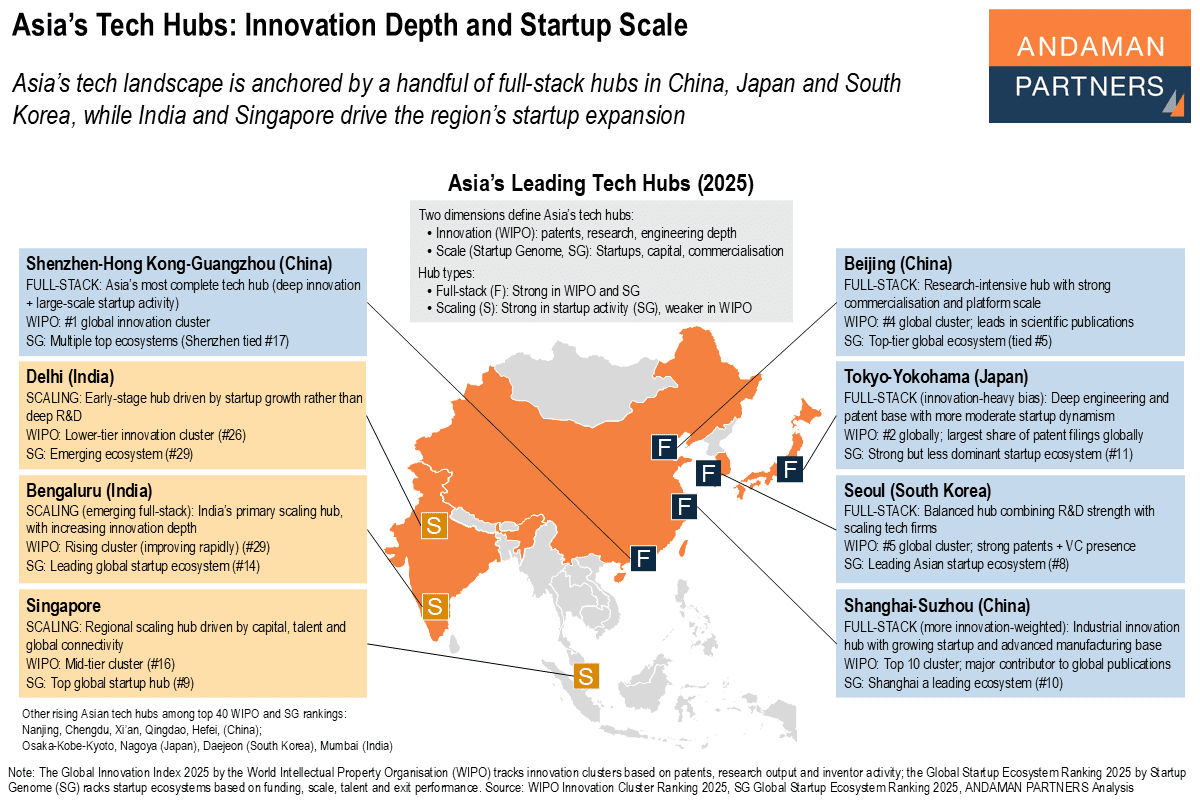

Asia’s tech landscape is anchored by a handful of full-stack hubs in China, Japan and South Korea, while India and Singapore drive startup expansion.