Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

AAMEG Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to sponsor and support the AAMEG pre-Mining Indaba Cocktails & Canapes event.

AAMEG & ACBSA Event in Johannesburg Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to sponsor and support the AAMEG & ABCSA pre-Mining Indaba Connections & Canapes event.

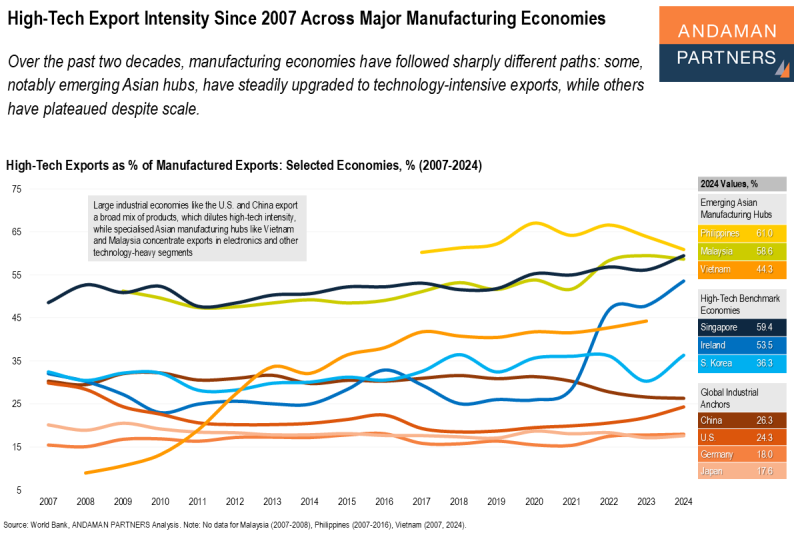

High-Tech Export Intensity Since 2007 Across Major Manufacturing Economies

Some manufacturing economies have upgraded to tech-intensive exports while others have plateaued despite scale.

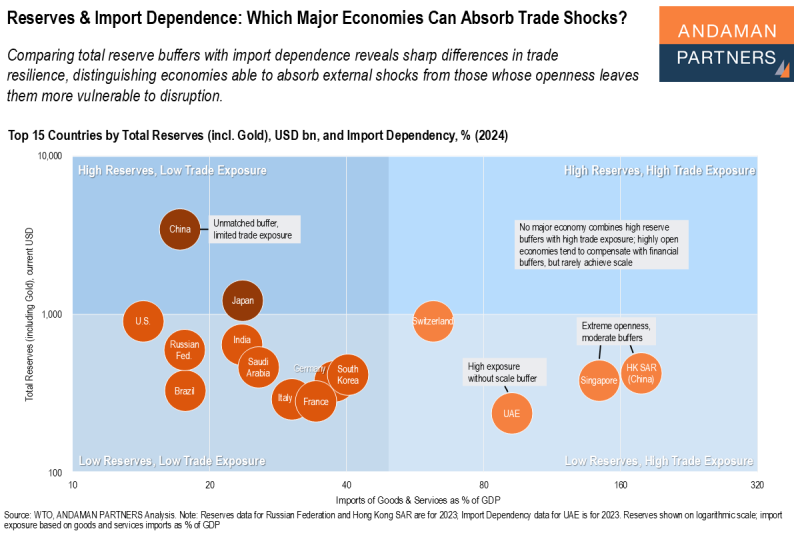

Reserves & Import Dependence: Which Major Economies Can Absorb Trade Shocks?

Comparing total reserve buffers with import dependence reveals sharp differences in trade resilience among major economies.

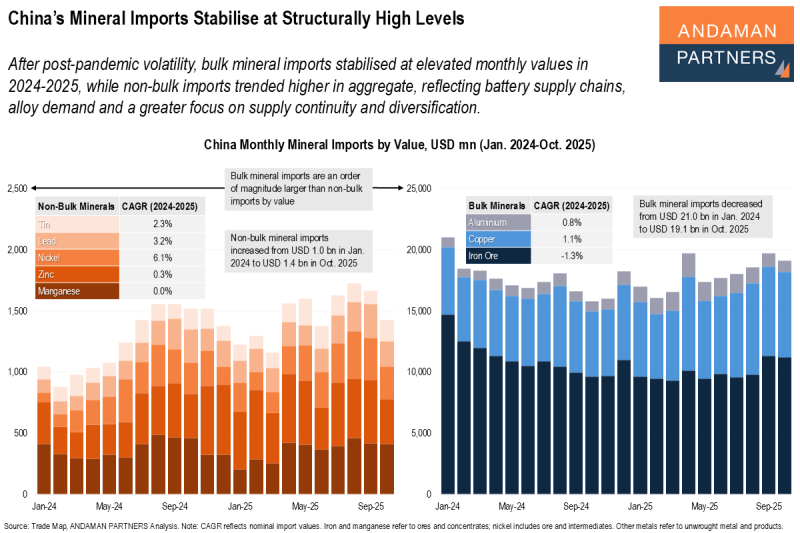

China’s Mineral Imports Stabilise at Structurally High Levels

Bulk mineral imports stabilised at elevated monthly values in 2024-2025, while non-bulk imports trended higher in aggregate.