The World’s Most Strategic Supply Chain Is Highly Concentrated and Interdependent

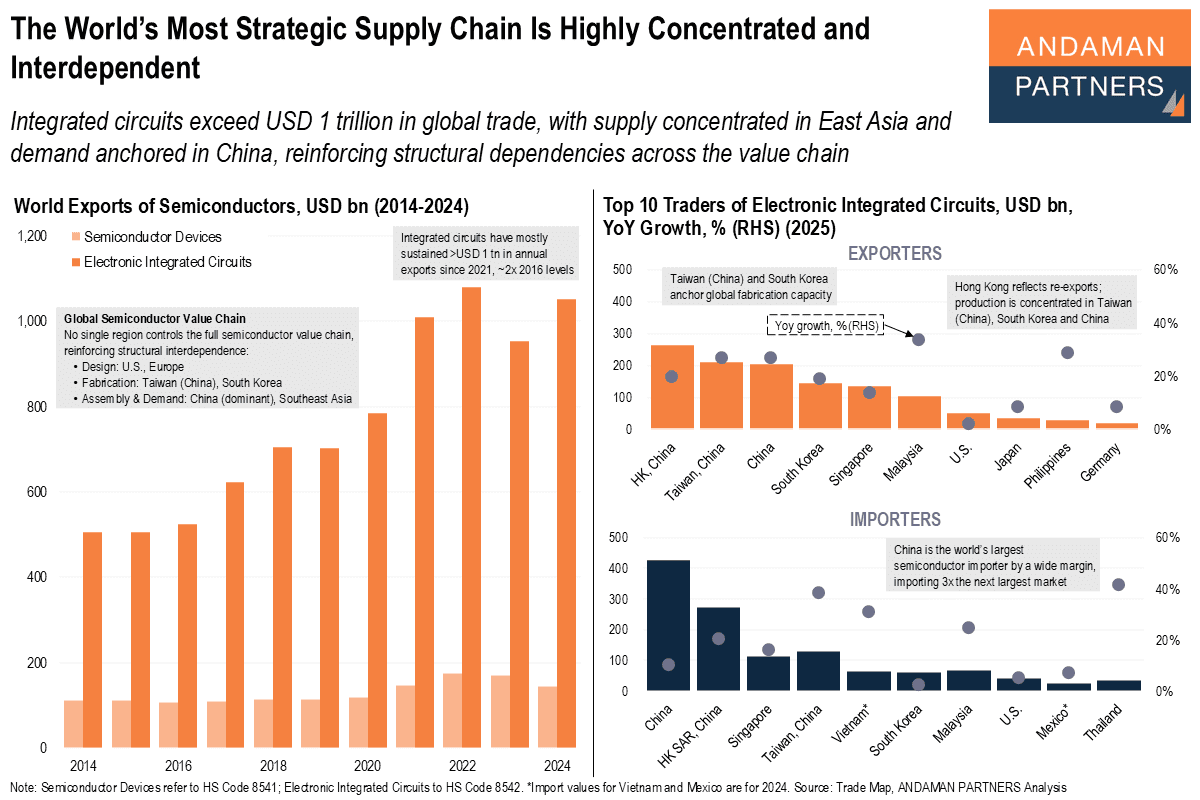

Integrated circuits exceed USD 1 trillion in global trade, with supply concentrated in Asia and demand in China, reinforcing structural dependencies.

Integrated circuits exceed USD 1 trillion in global trade, with supply concentrated in Asia and demand in China, reinforcing structural dependencies.

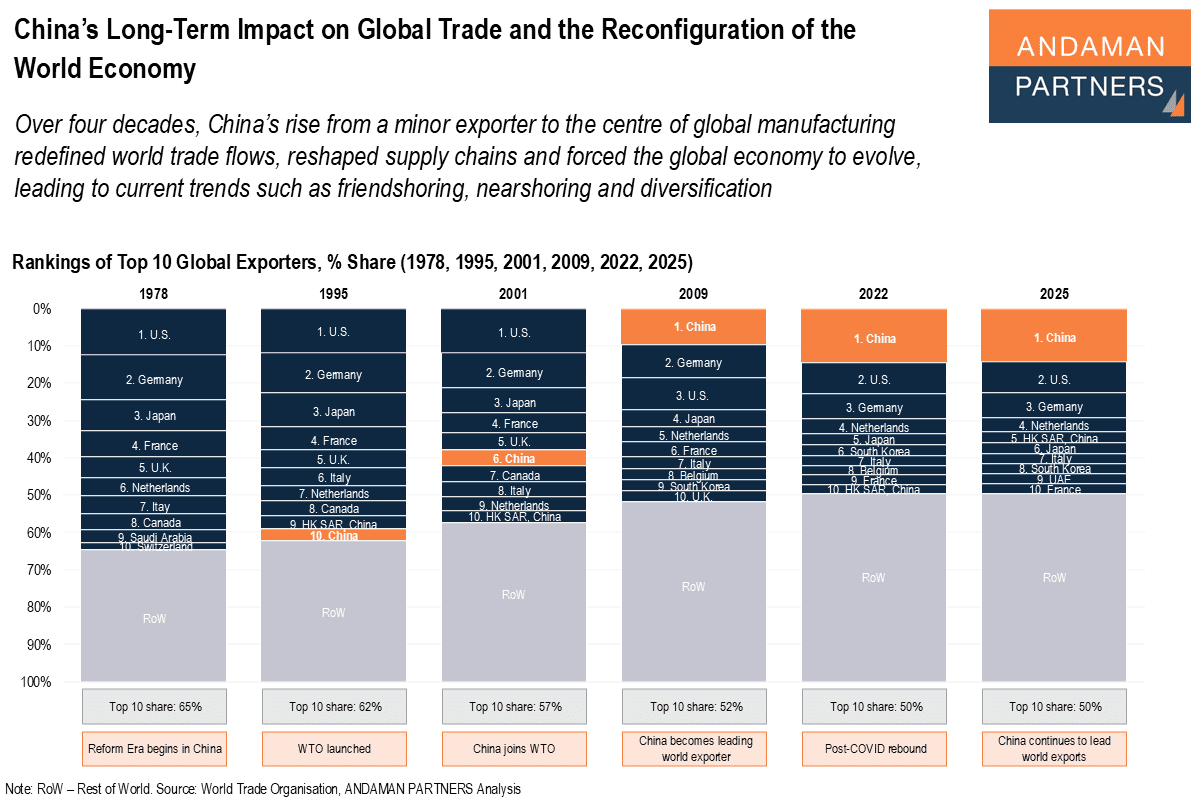

China’s rise from a minor exporter to the centre of global manufacturing redefined trade flows, reshaped supply chains and forced the global economy to evolve.

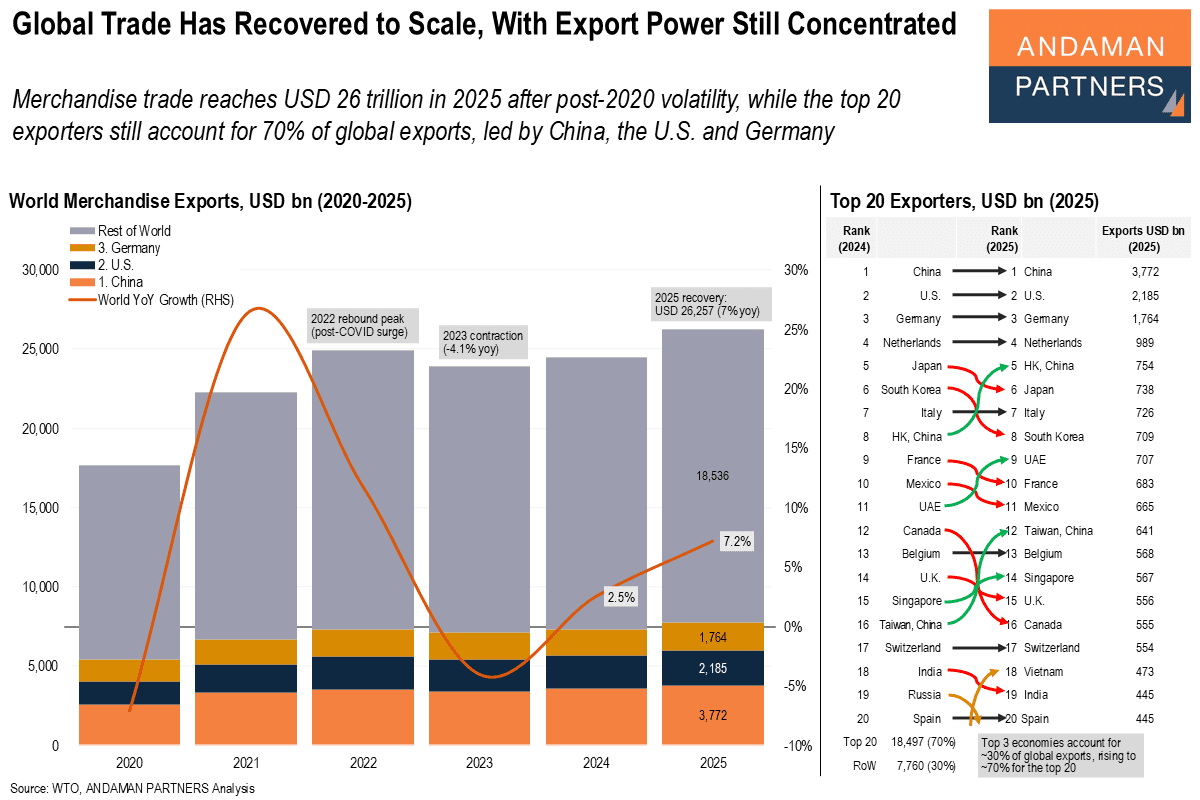

Merchandise trade reaches USD 26 trillion in 2025, while the top 20 exporters account for 70% of global exports.

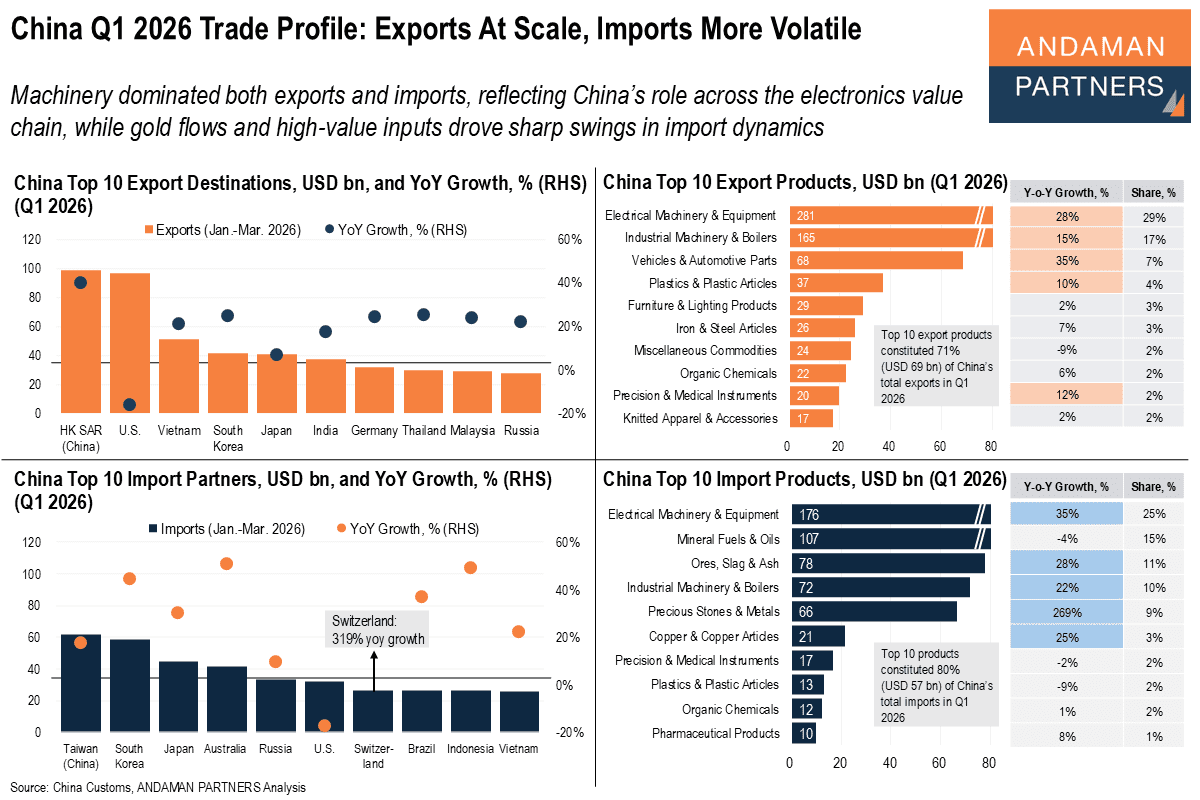

Machinery dominated exports and imports, reflecting China’s role across the electronics value chain; gold and high-value inputs drove import swings.

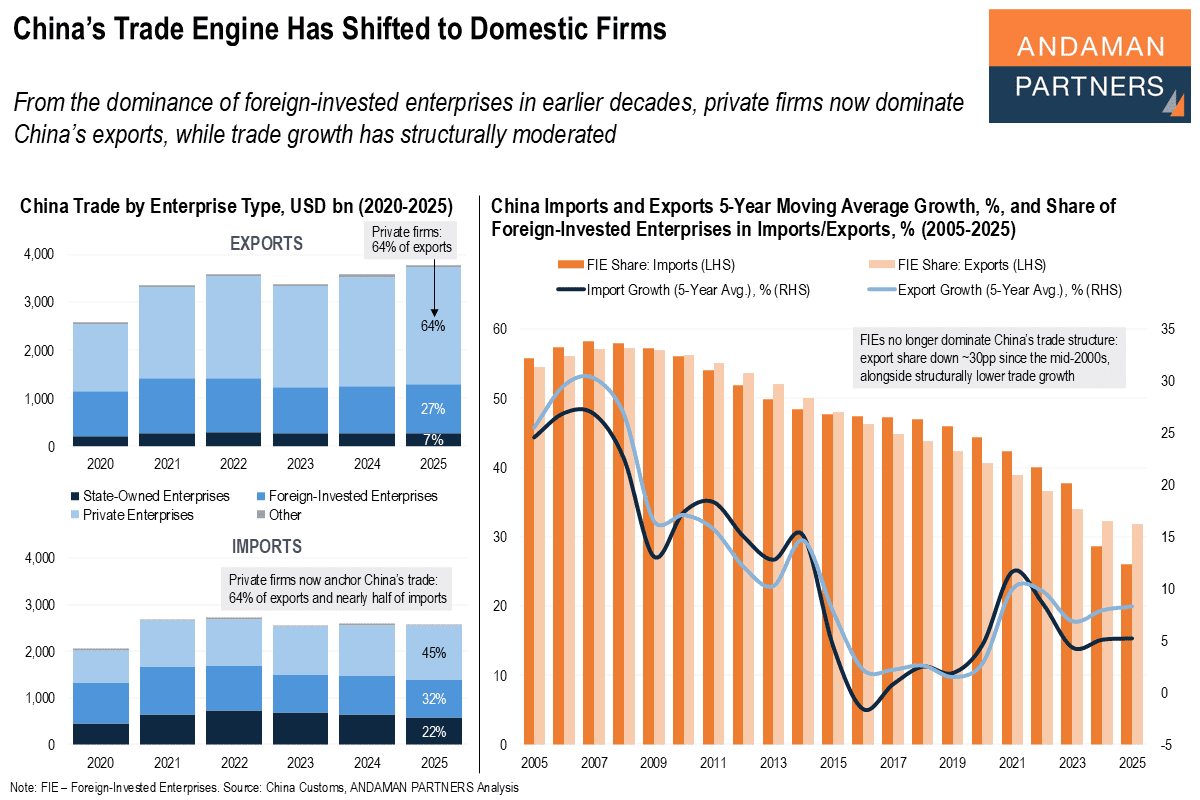

Private firms now dominate China’s exports, while trade growth has structurally moderated.

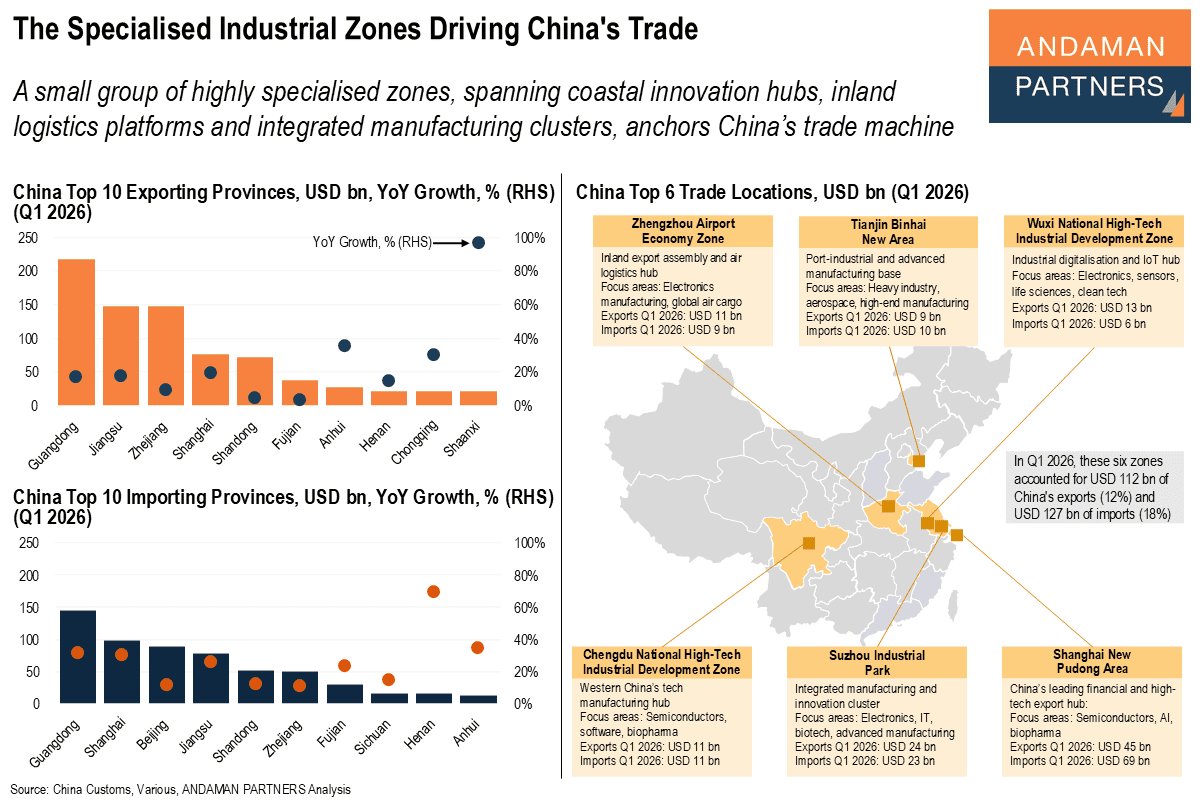

A small group of highly specialised zones anchors China’s trade machine.

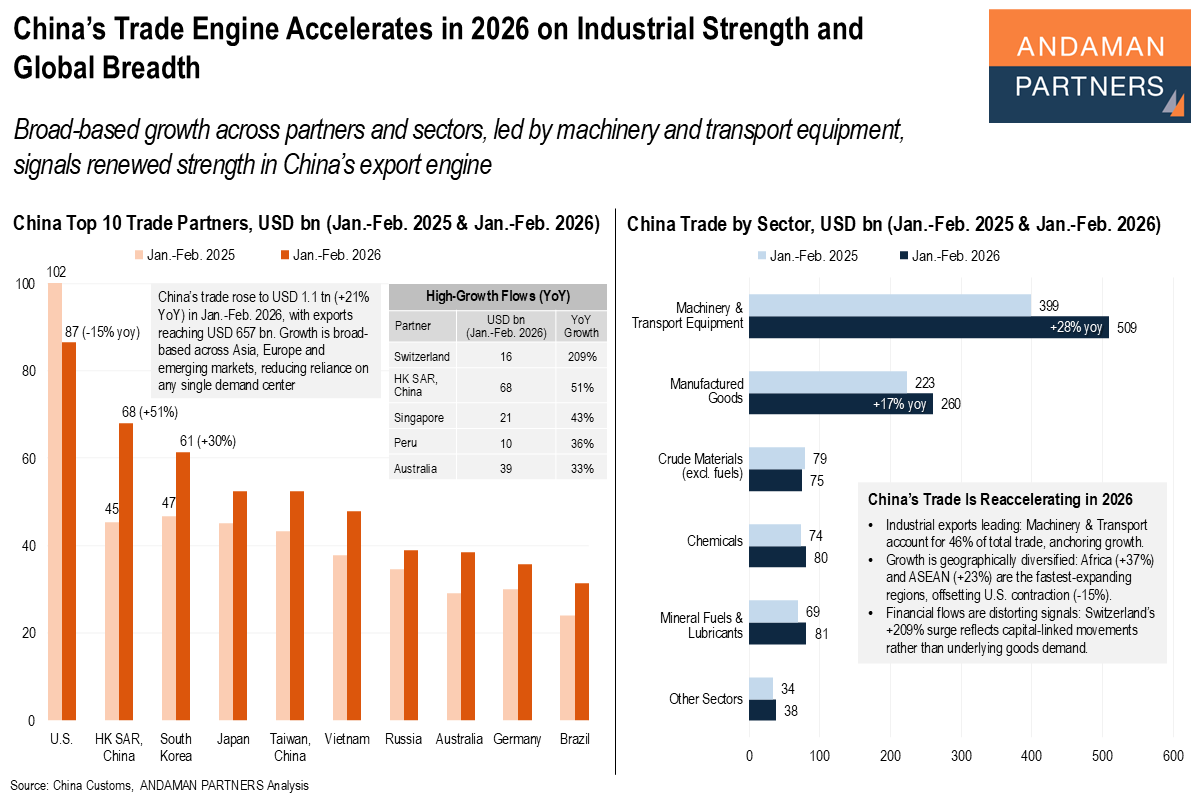

Broad-based growth across partners and sectors, led by machinery and transport equipment, signals renewed strength in China’s export engine.

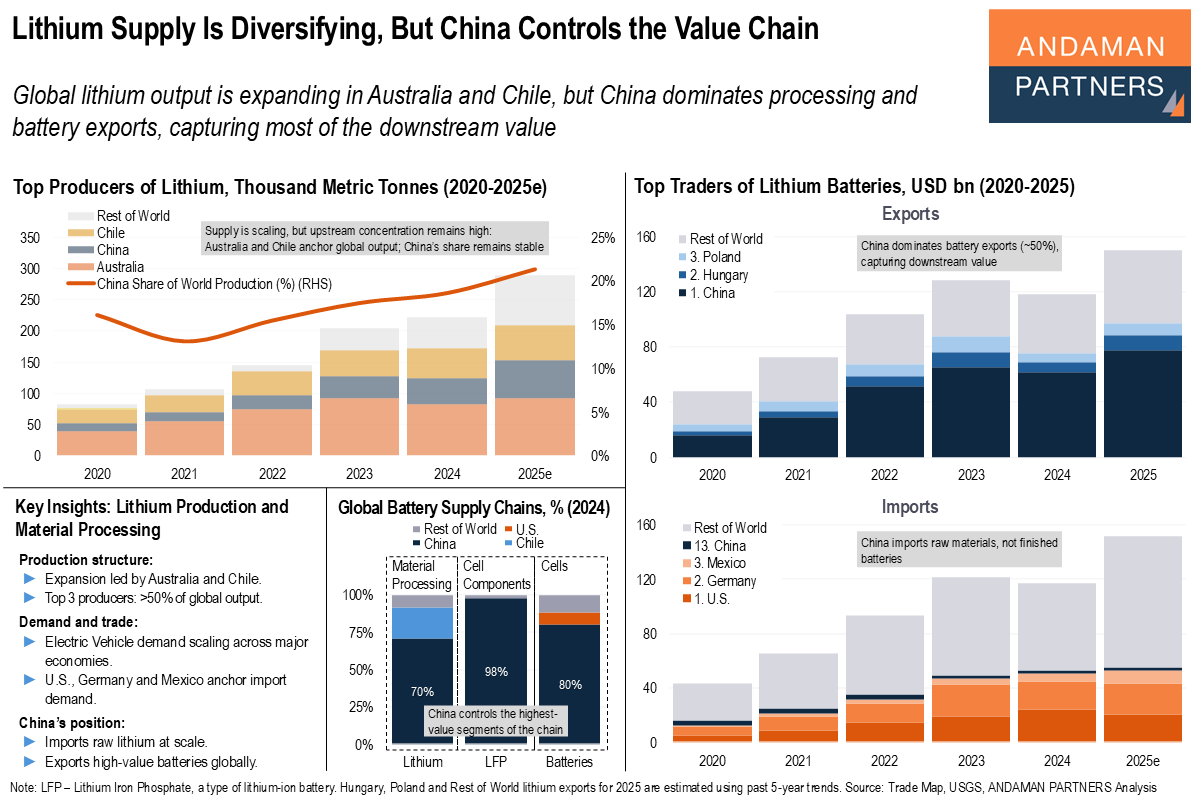

Global lithium output is expanding in Australia and Chile, but China dominates processing and battery exports, capturing most of the downstream value.

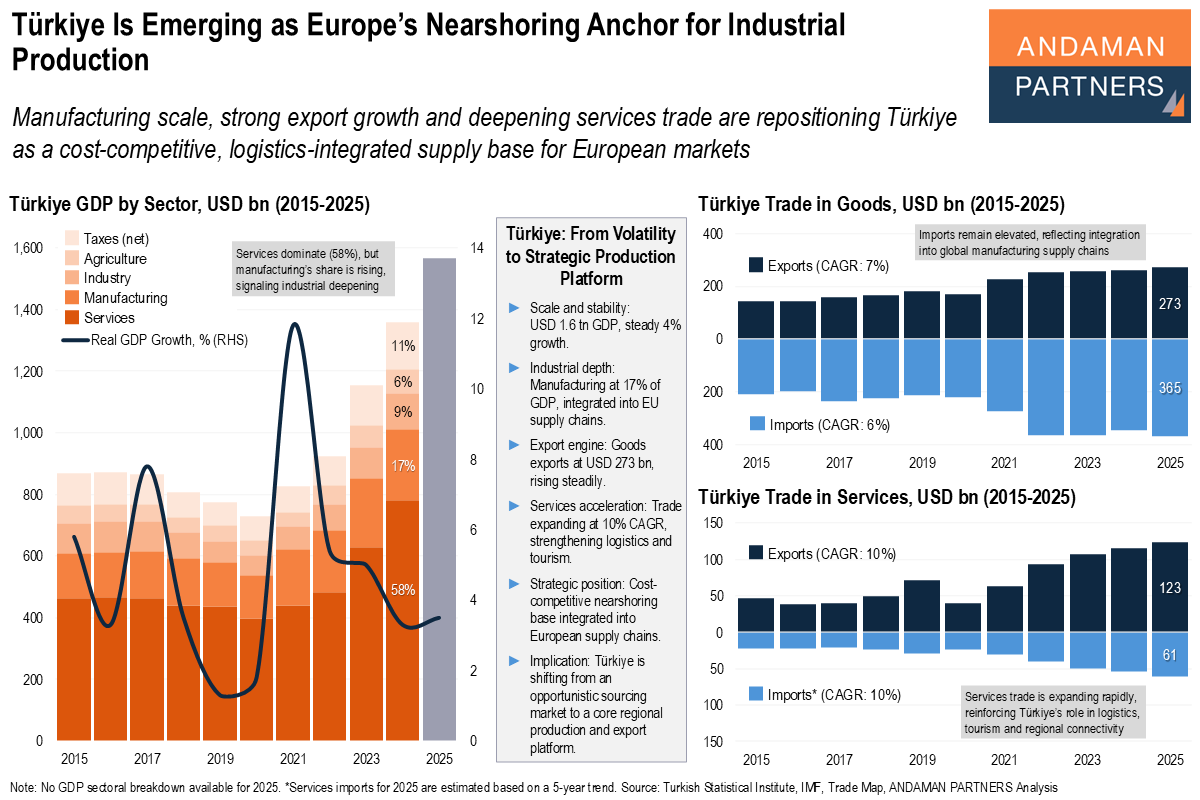

Manufacturing scale, strong export growth and deepening services trade are repositioning Türkiye as a cost-competitive supply base for Europe.

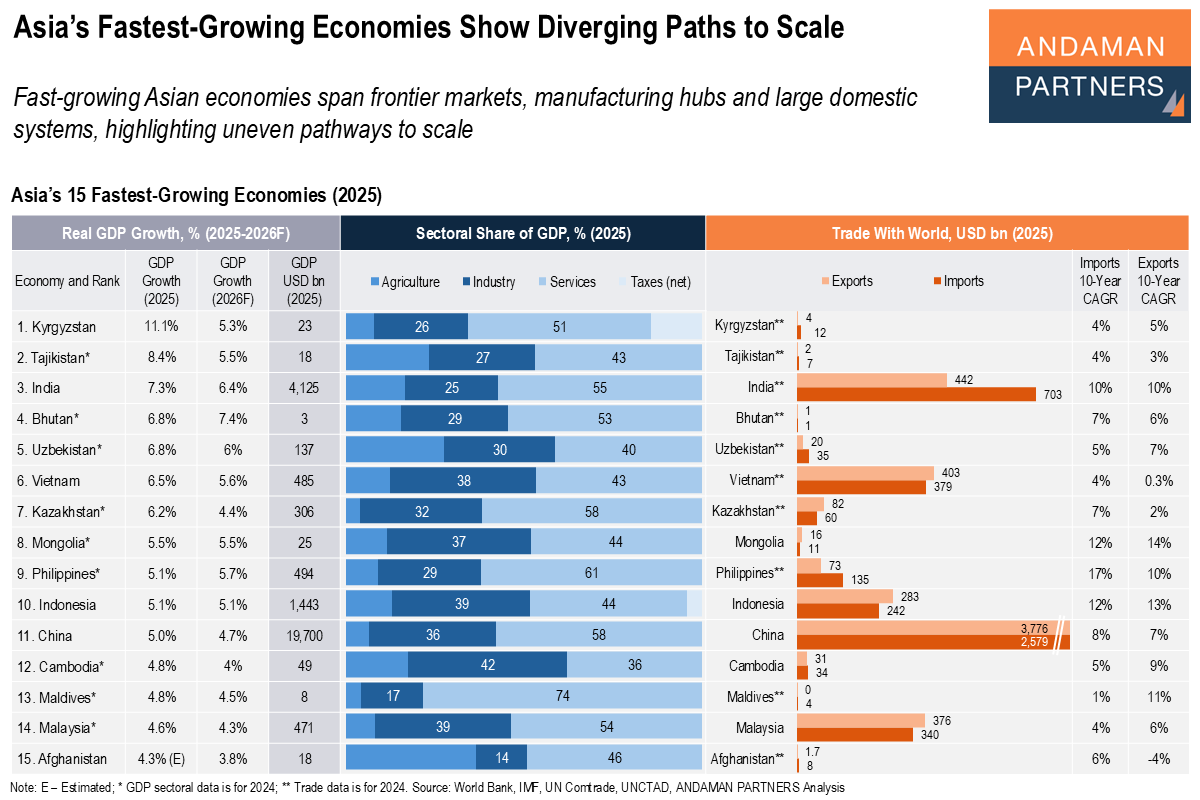

Fast-growing Asian economies span frontier markets, manufacturing hubs and large domestic systems, highlighting uneven pathways to scale.