High-Tech Export Intensity Since 2007 Across Major Manufacturing Economies

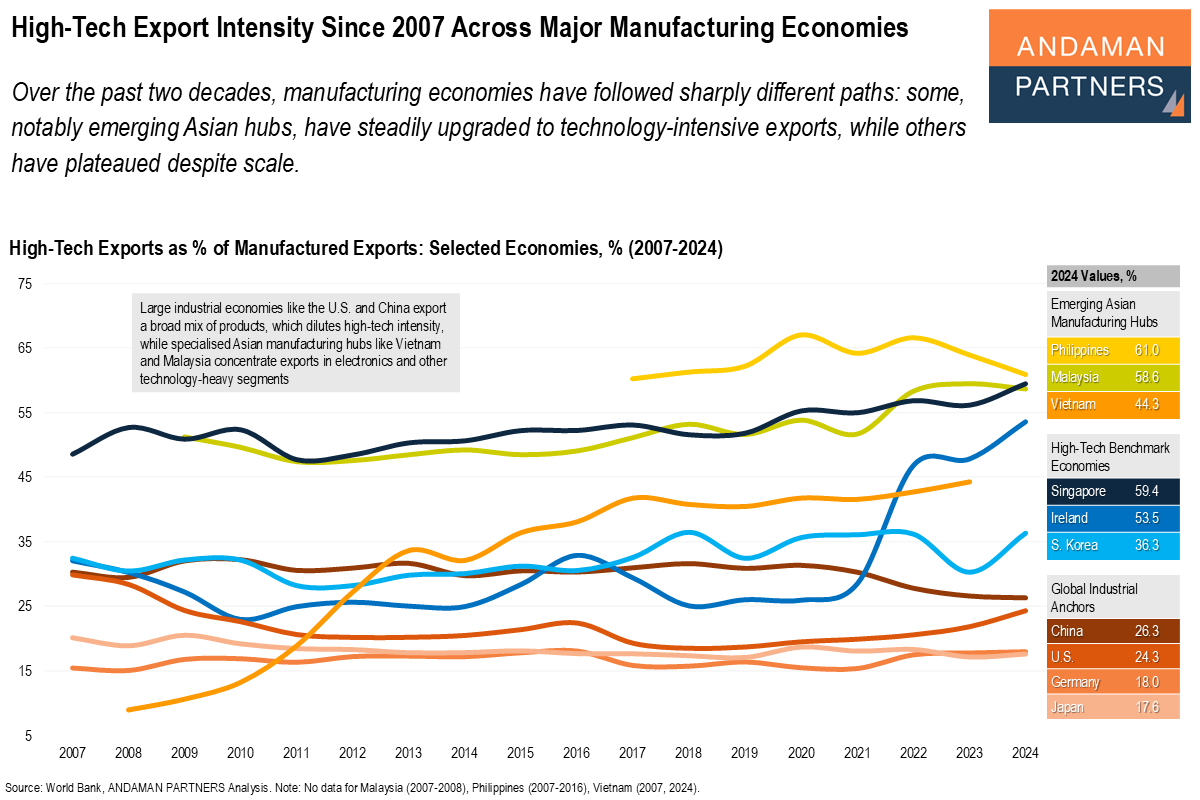

Some manufacturing economies have upgraded to tech-intensive exports while others have plateaued despite scale.

Some manufacturing economies have upgraded to tech-intensive exports while others have plateaued despite scale.

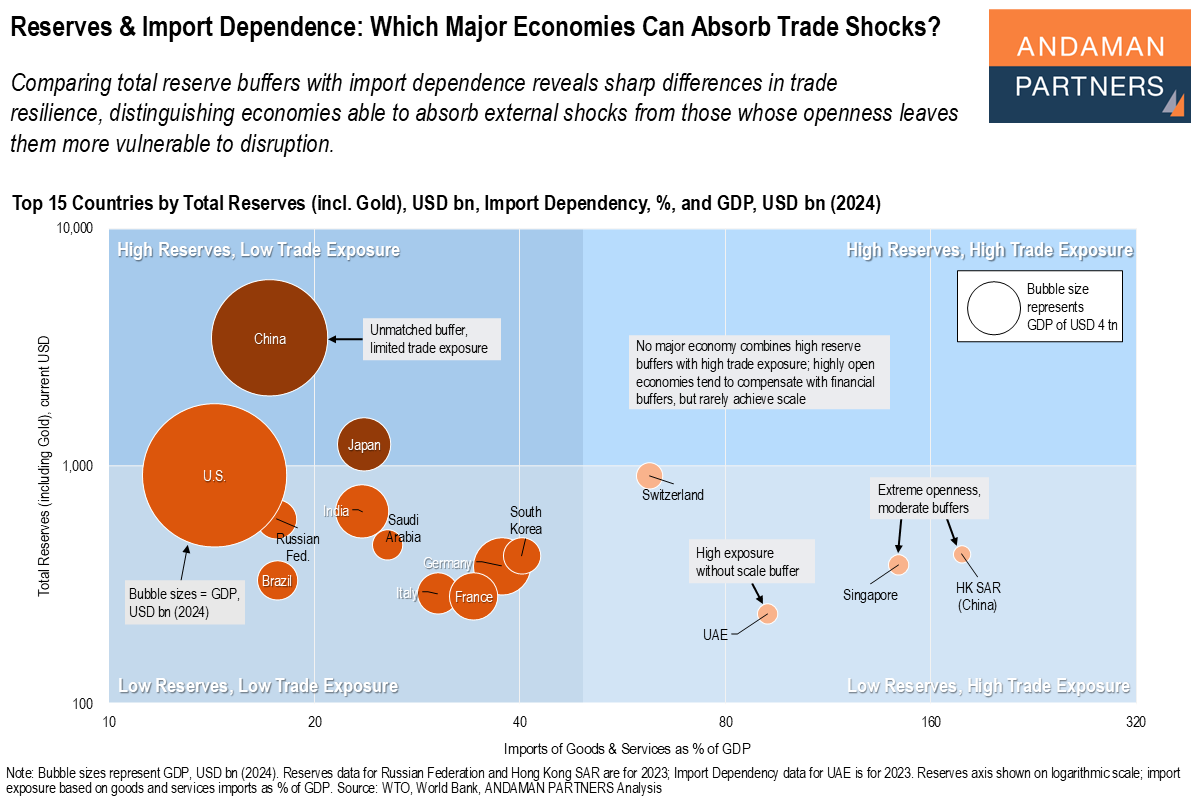

Comparing total reserve buffers with import dependence reveals sharp differences in trade resilience among major economies.

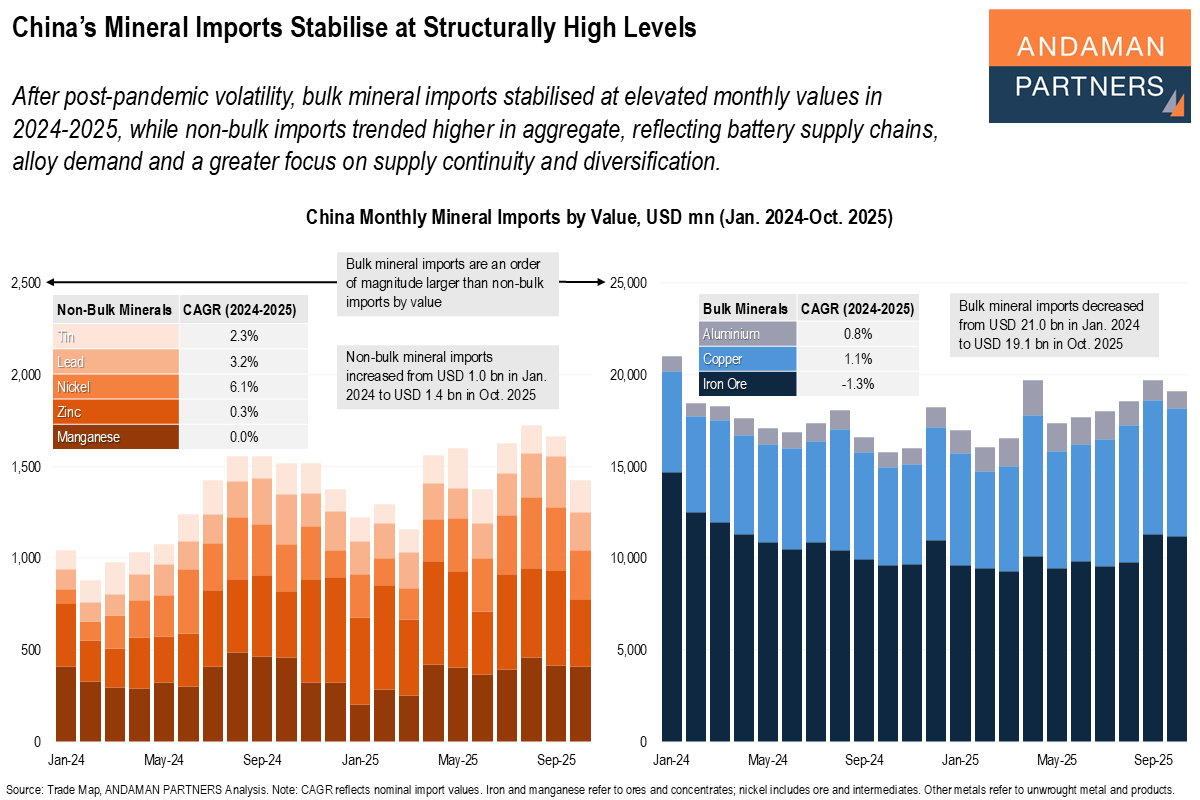

Bulk mineral imports stabilised at elevated monthly values in 2024-2025, while non-bulk imports trended higher in aggregate.

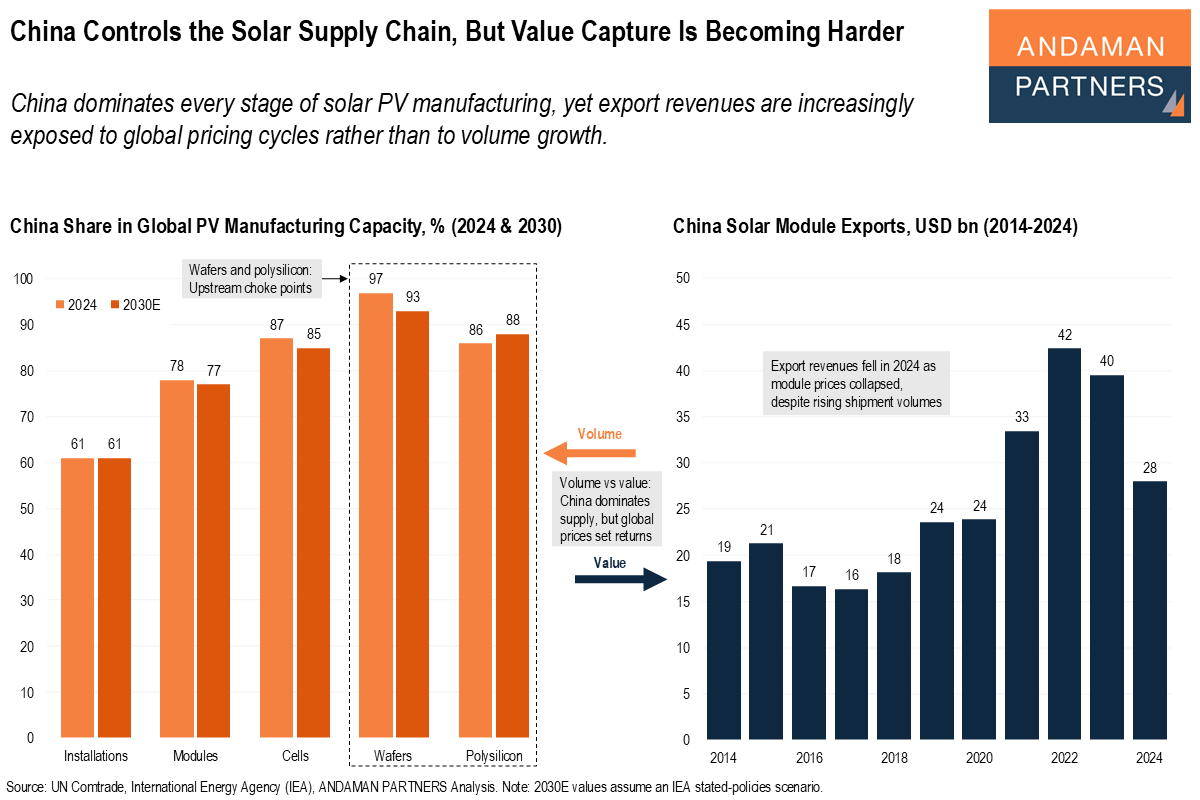

China dominates every stage of solar PV manufacturing, yet export revenues are increasingly exposed to global pricing cycles rather than to volume growth.

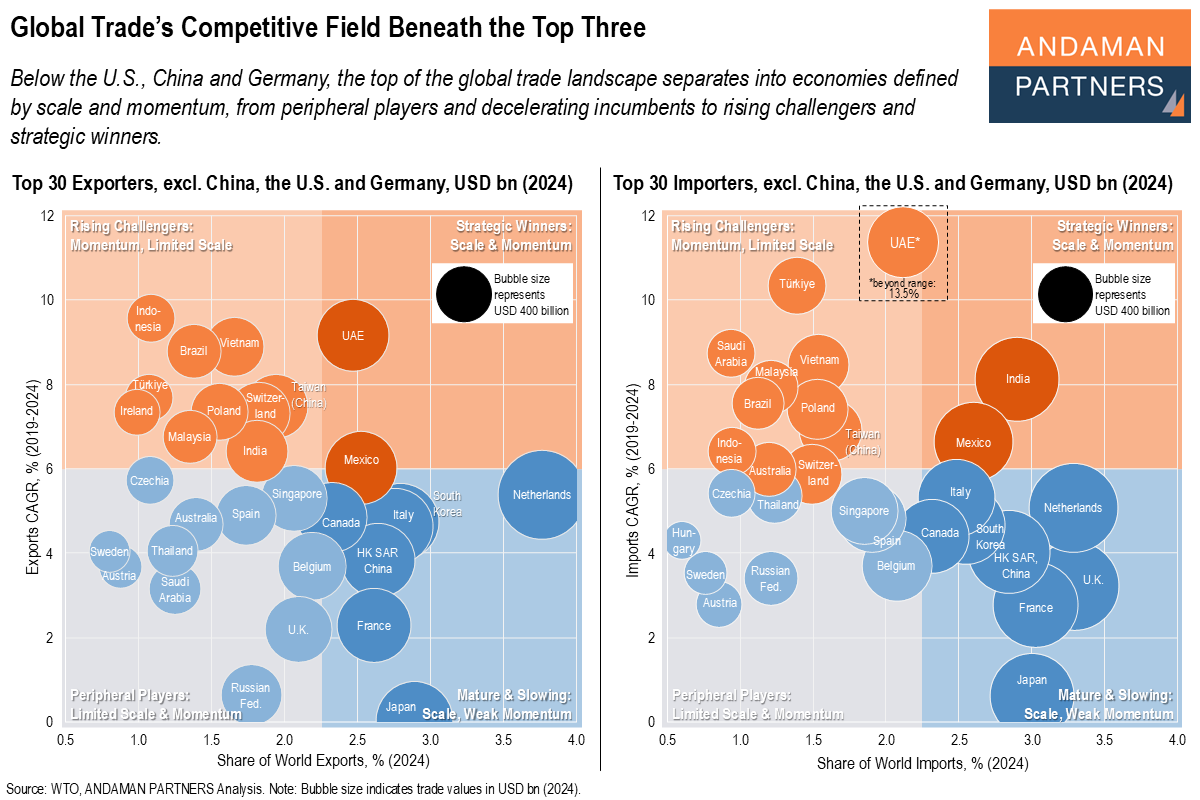

The top of the global trade landscape separates into economies defined by scale and momentum.

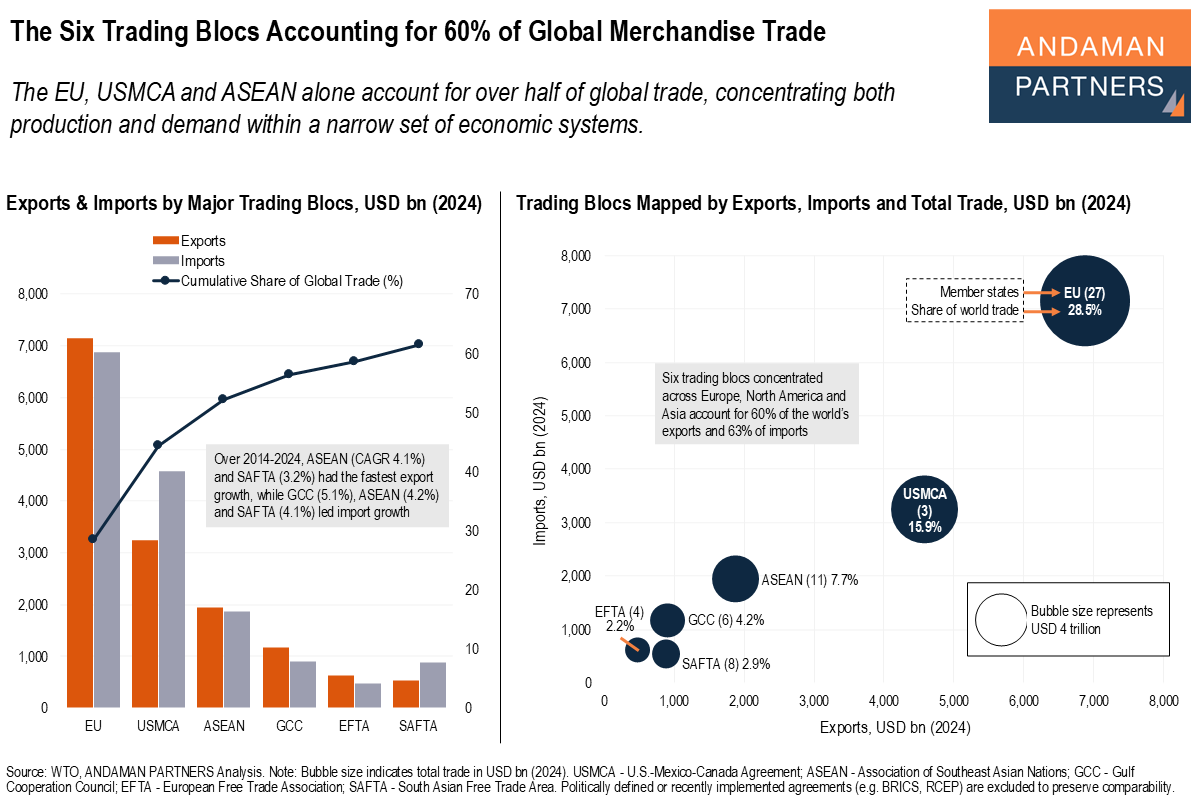

The EU, USMCA and ASEAN alone account for over half of global trade, concentrating both production and demand within a narrow set of economic systems.

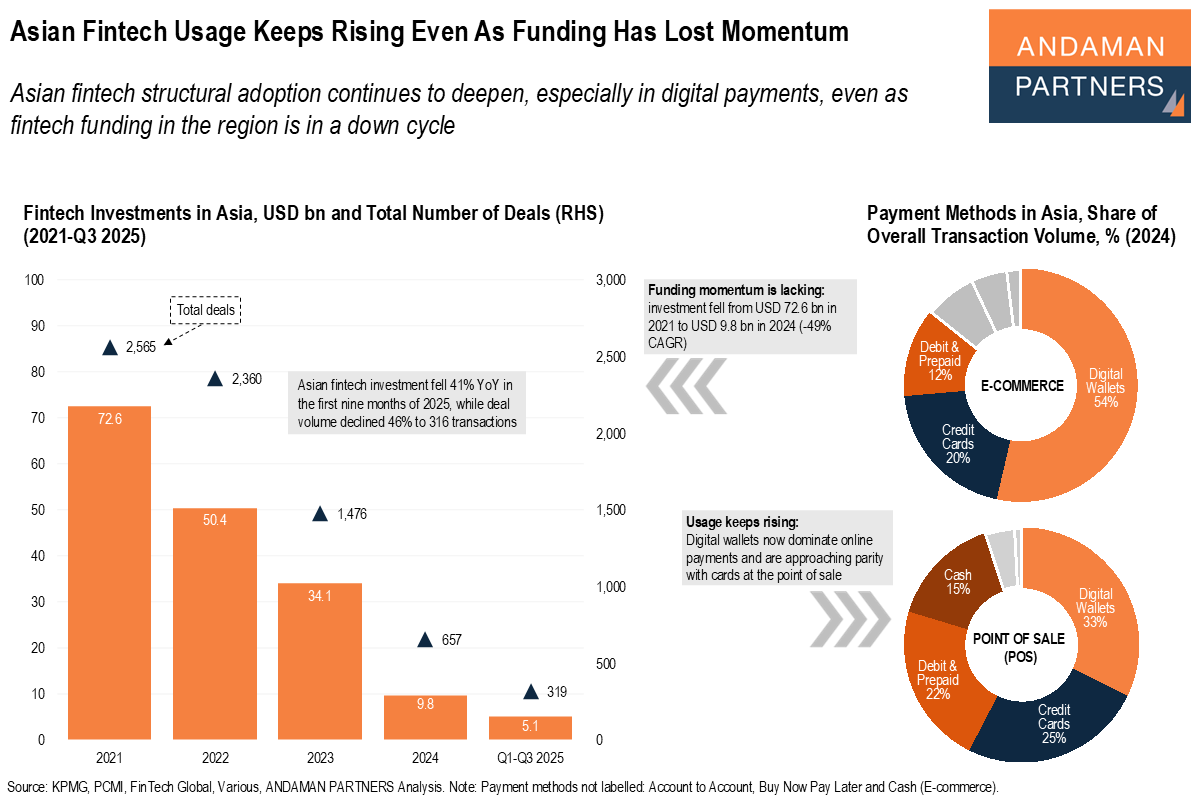

Asian fintech structural adoption continues to deepen, especially in digital payments, even as fintech funding in the region is in a down cycle.

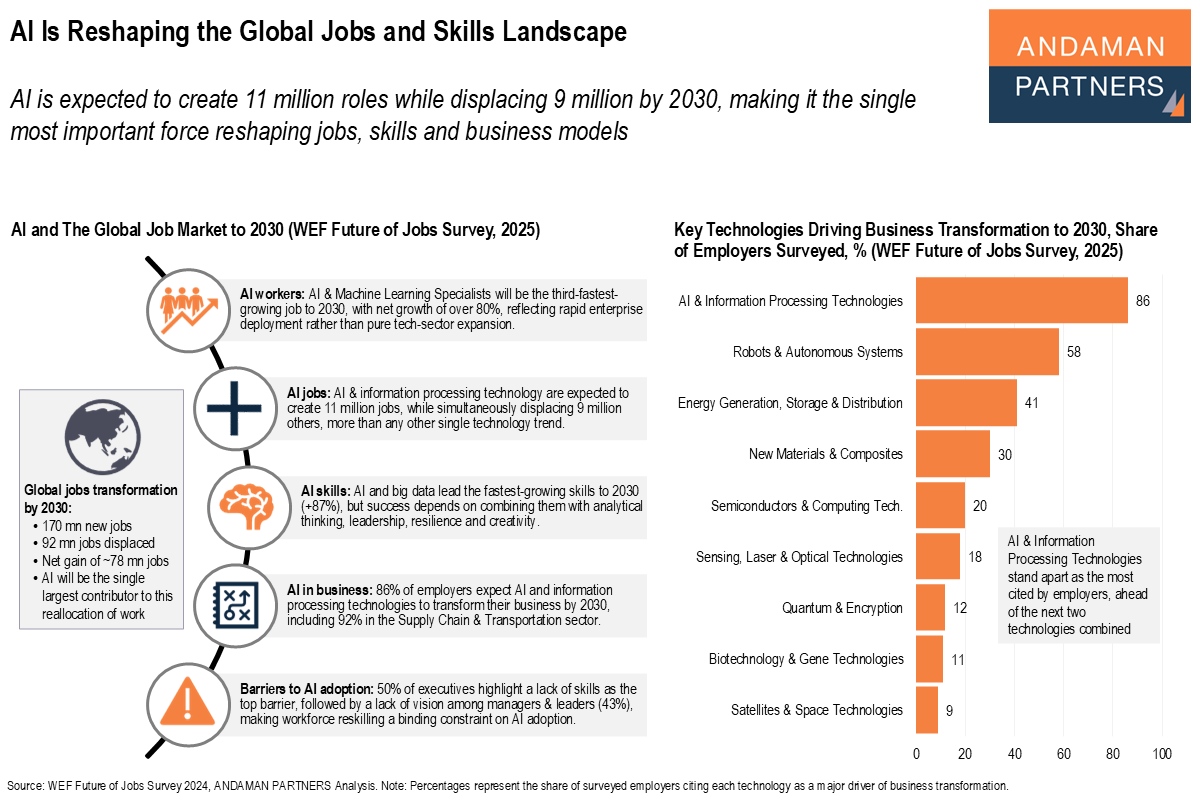

AI is expected to create 11 million roles while displacing 9 million by 2030, making it the single most important force reshaping jobs, skills and business models.

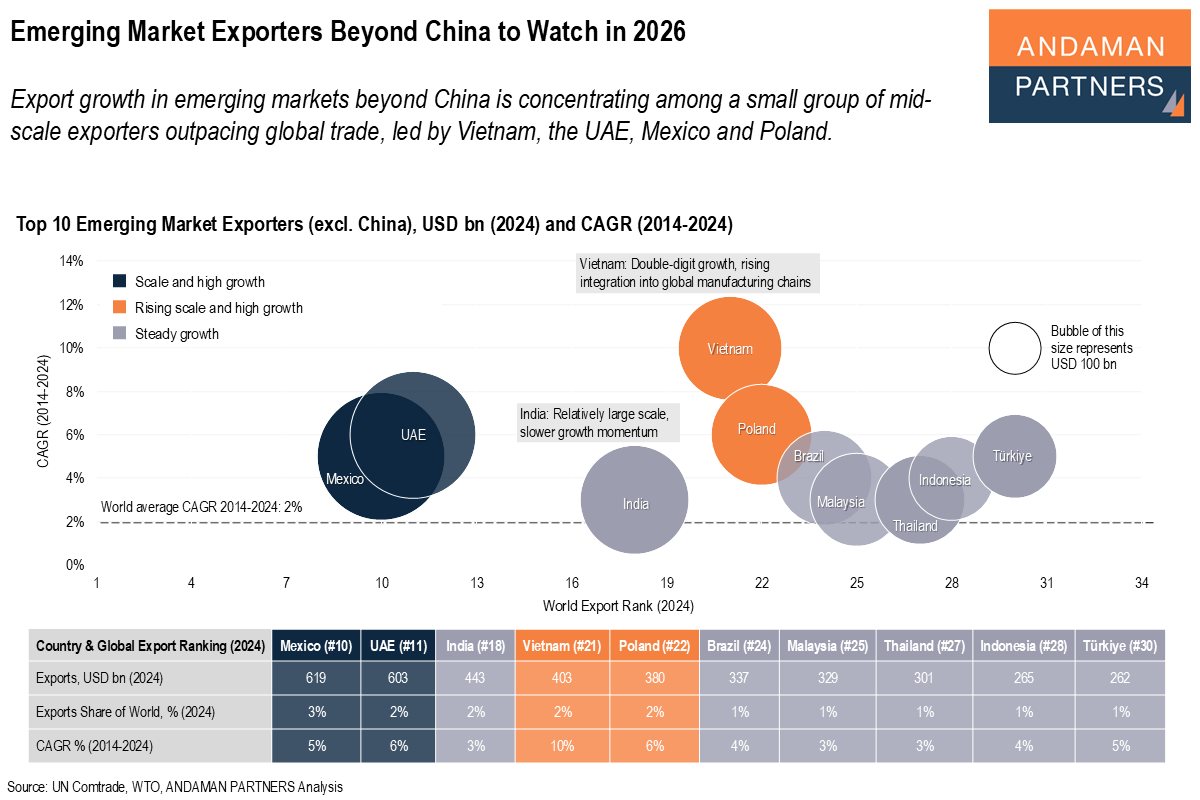

Export growth in emerging markets beyond China is concentrating among a small group of mid-scale exporters outpacing global trade.

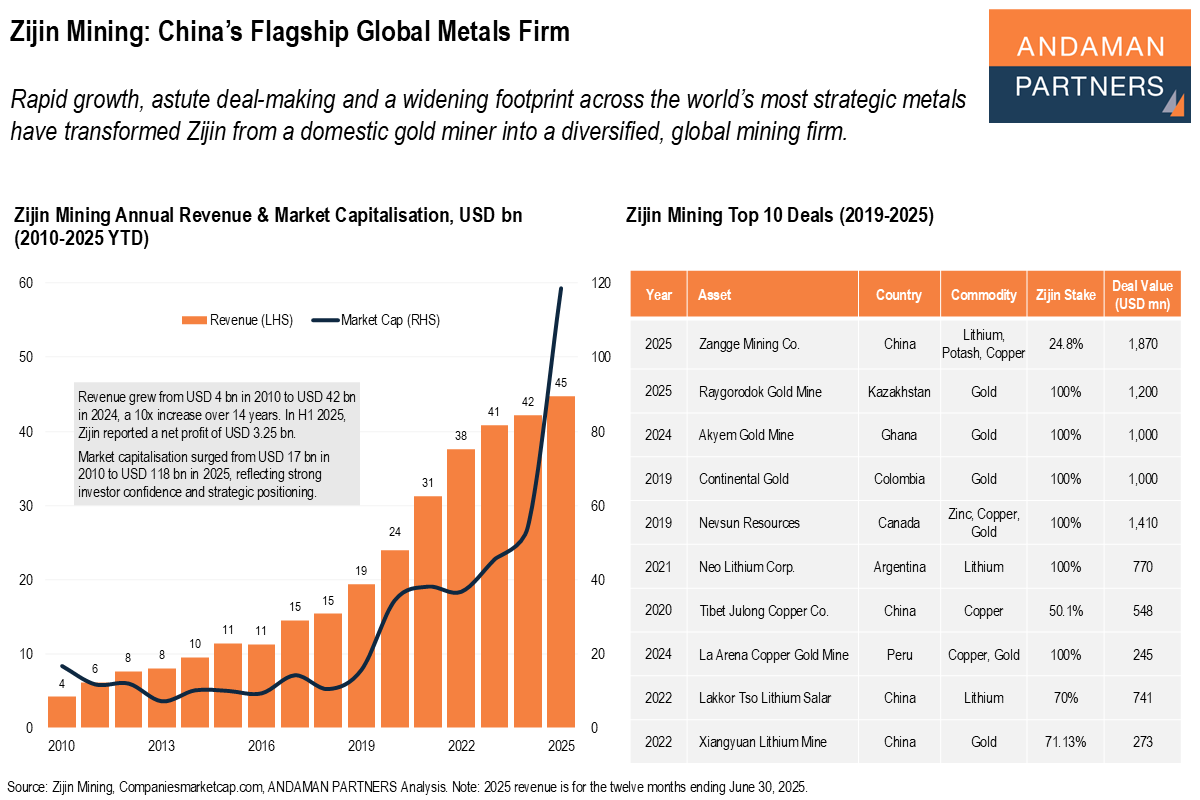

Rapid growth, astute deal-making and a widening footprint across strategic metals have transformed Zijin into a diversified, global mining firm.