ANDAMAN PARTNERS Attended the Australia Governance Summit 2026 in Sydney

ANDAMAN PARTNERS Co-Founder Kobus van der Wath attended the Australia Governance Summit (AGS26) in Sydney, Australia.

ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

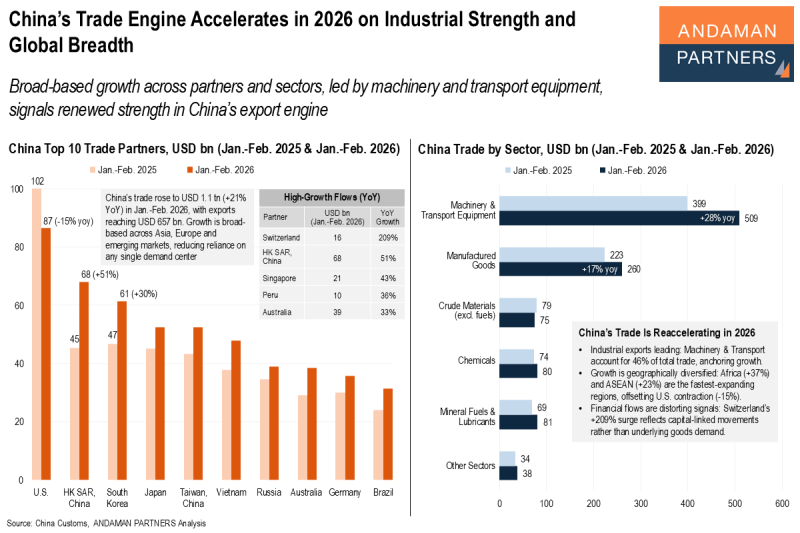

China’s Trade Engine Accelerates in 2026 on Industrial Strength and Global Breadth

Broad-based growth across partners and sectors, led by machinery and transport equipment, signals renewed strength in China’s export engine.

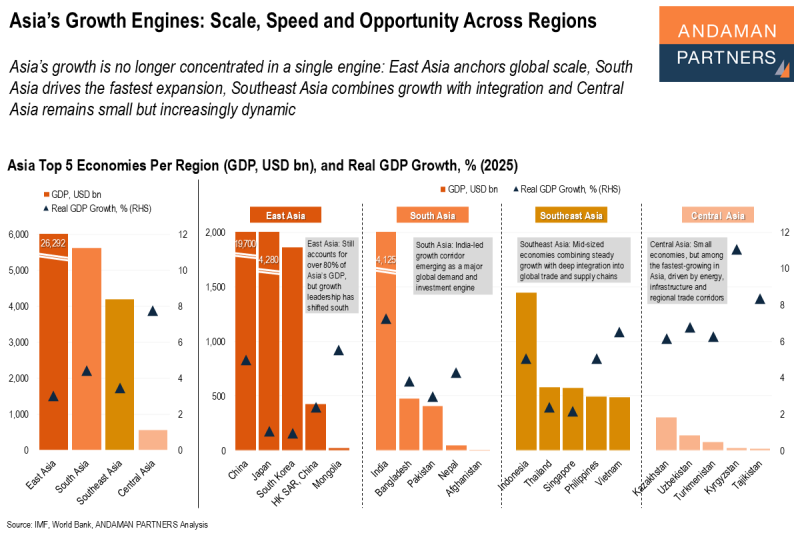

Asia’s Growth Engines: Scale, Speed and Opportunity Across Regions

Asia’s scale, speed and integration are no longer concentrated in a single core, but spread across multiple, complementary engines.

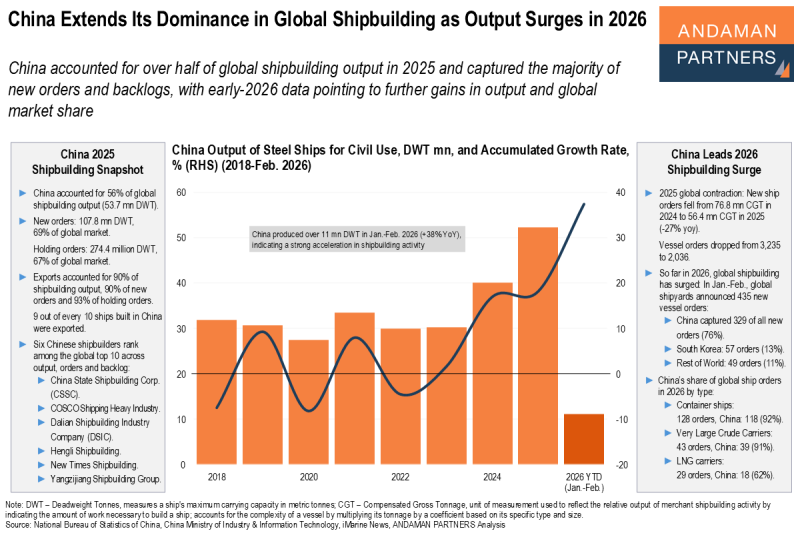

China Extends Its Dominance in Global Shipbuilding as Output Surges in 2026

Even as global ship orders declined in 2025, early-2026 data shows a rapid rebound, with China securing the vast majority of new contracts.