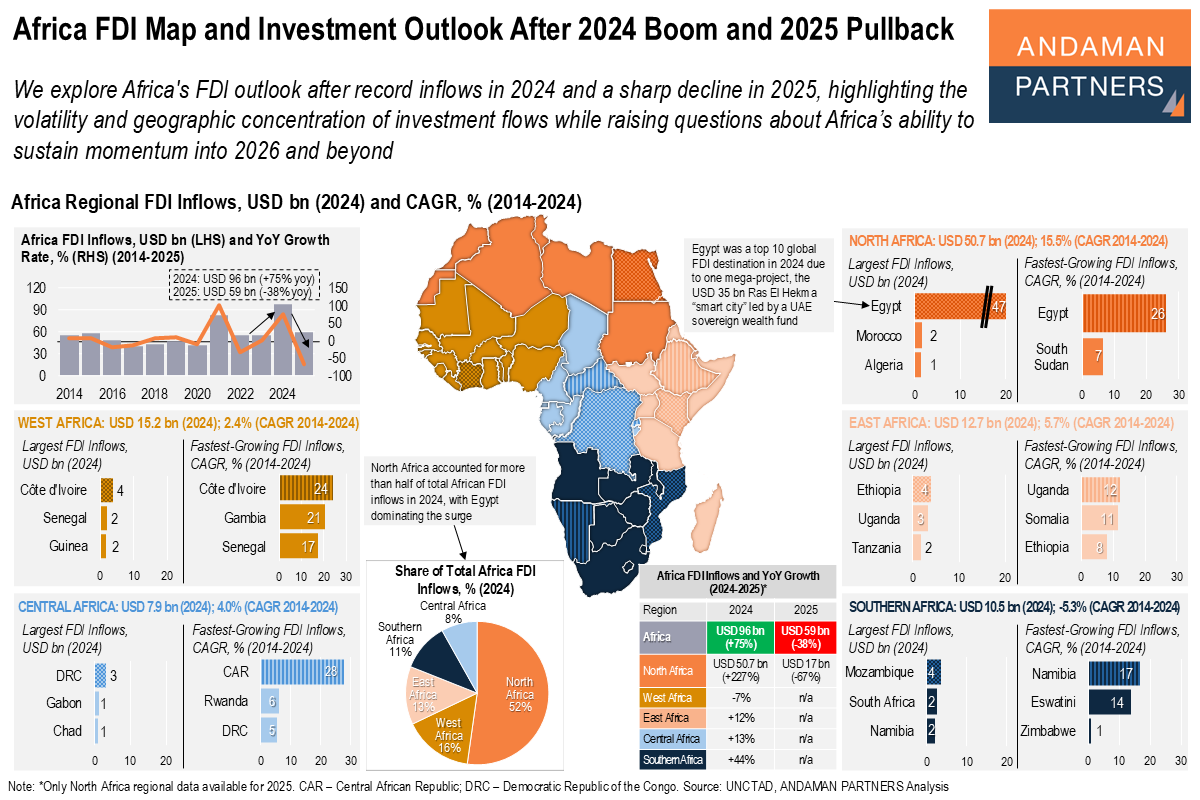

Africa FDI Map and Investment Outlook After 2024 Boom and 2025 Pullback

The volatility and geographic concentration of investment flows raises questions about Africa’s ability to sustain momentum into 2026 and beyond.

The volatility and geographic concentration of investment flows raises questions about Africa’s ability to sustain momentum into 2026 and beyond.

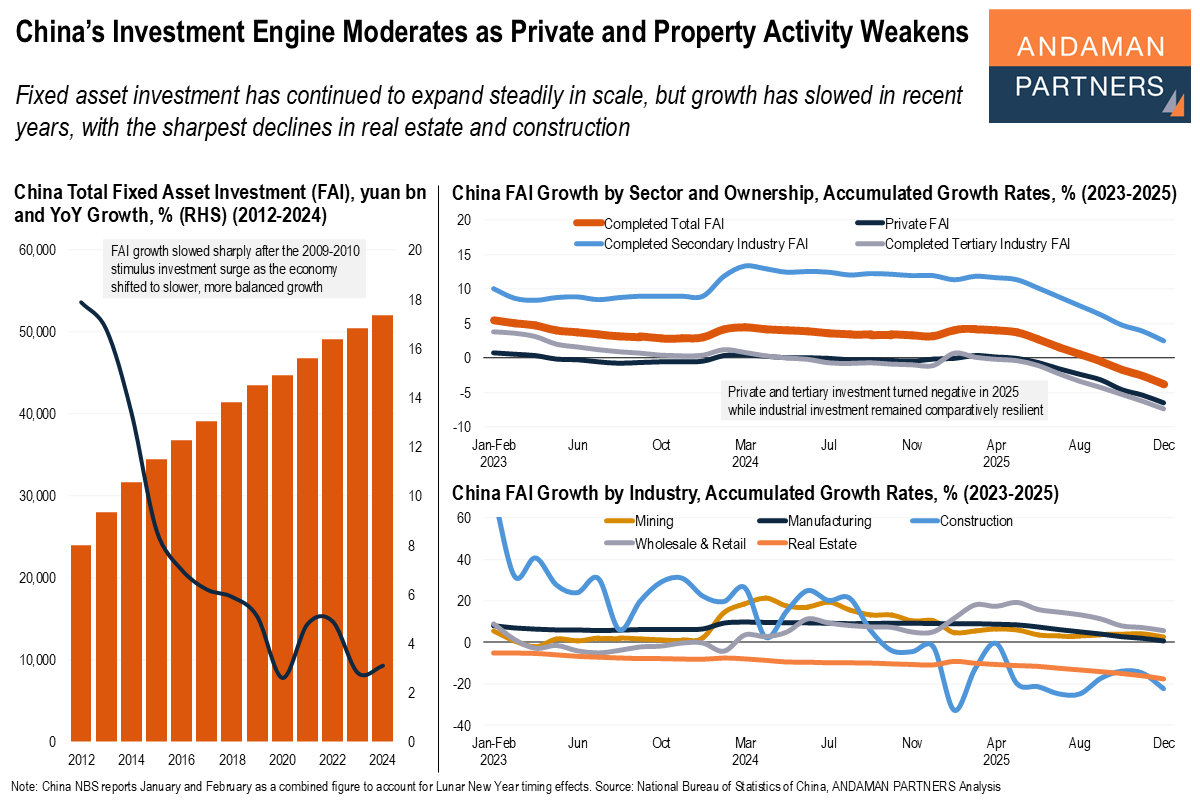

Fixed asset investment has continued to expand steadily, but growth has slowed in recent years, with the sharpest declines in real estate and construction.

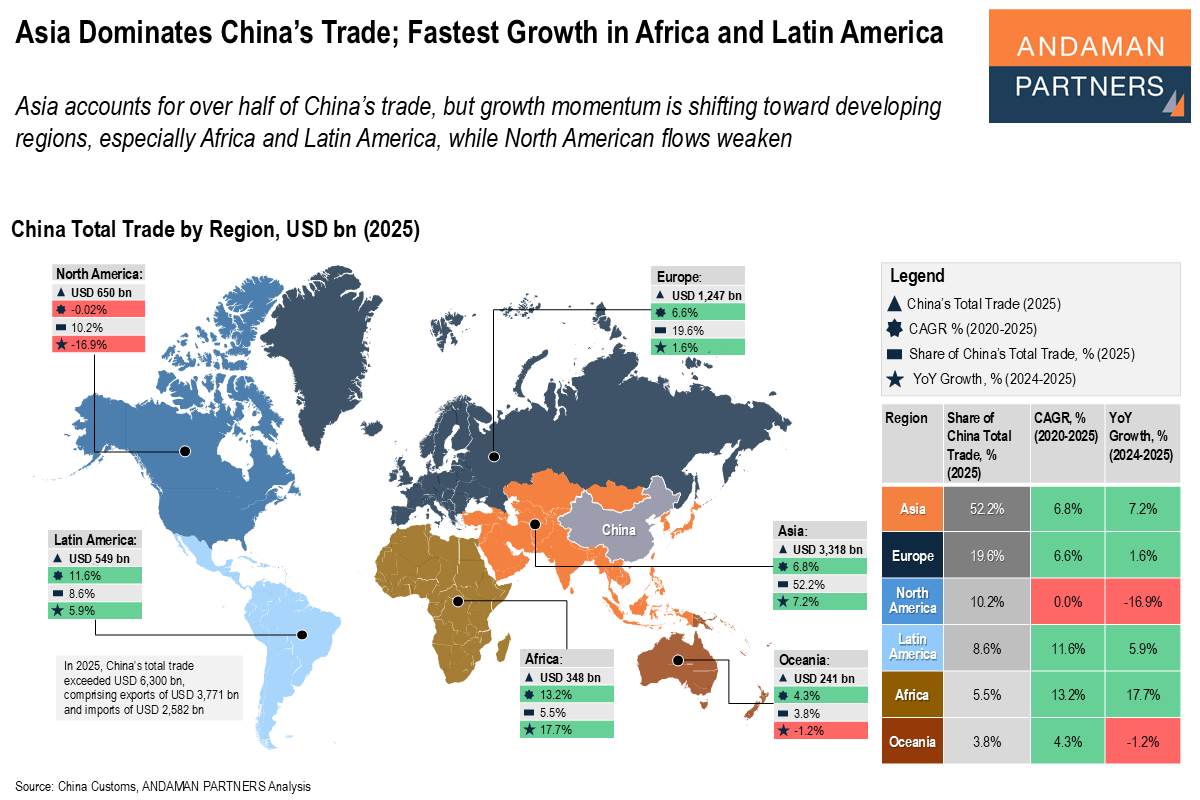

Asia accounts for over half of China’s trade, but growth momentum is shifting toward developing regions, especially Africa and Latin America.

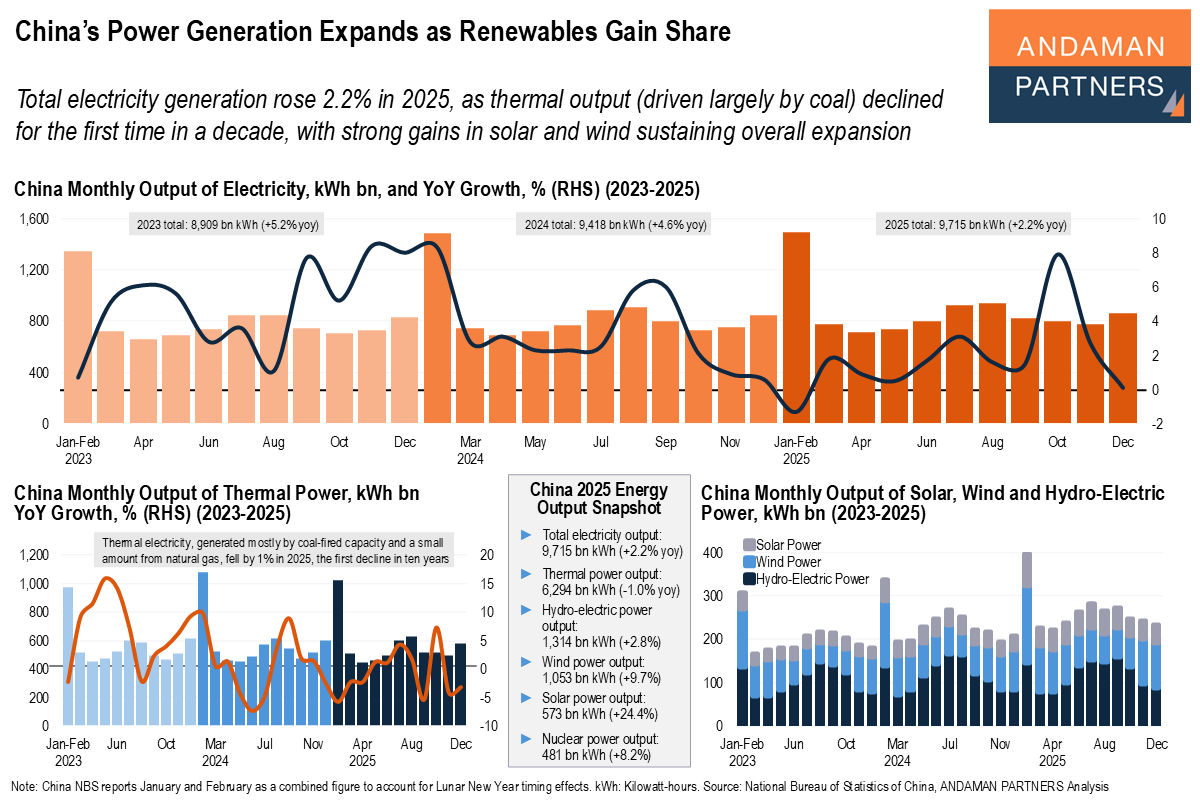

Electricity generation rose 2.2% in 2025, as thermal output declined for the first time in a decade, with strong gains in solar and wind.

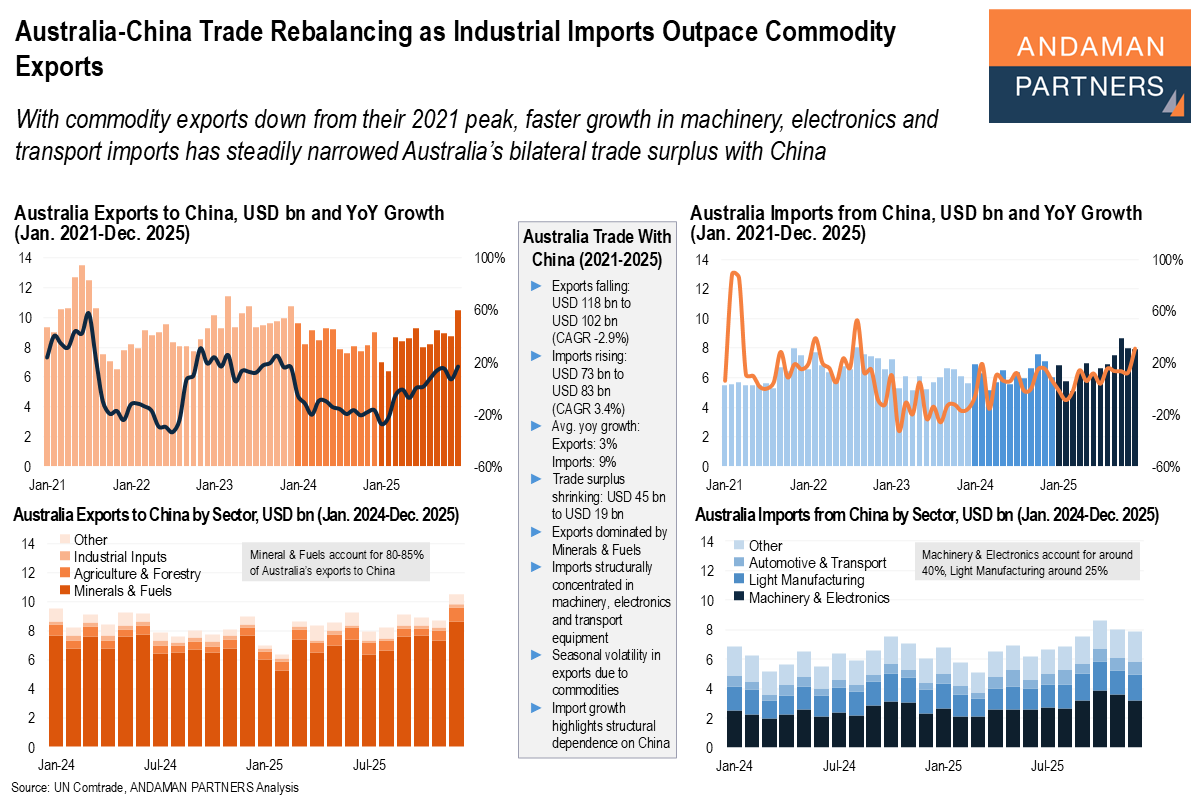

With commodity exports down from 2021, faster growth in machinery, electronics and transport imports has narrowed Australia’s trade surplus.

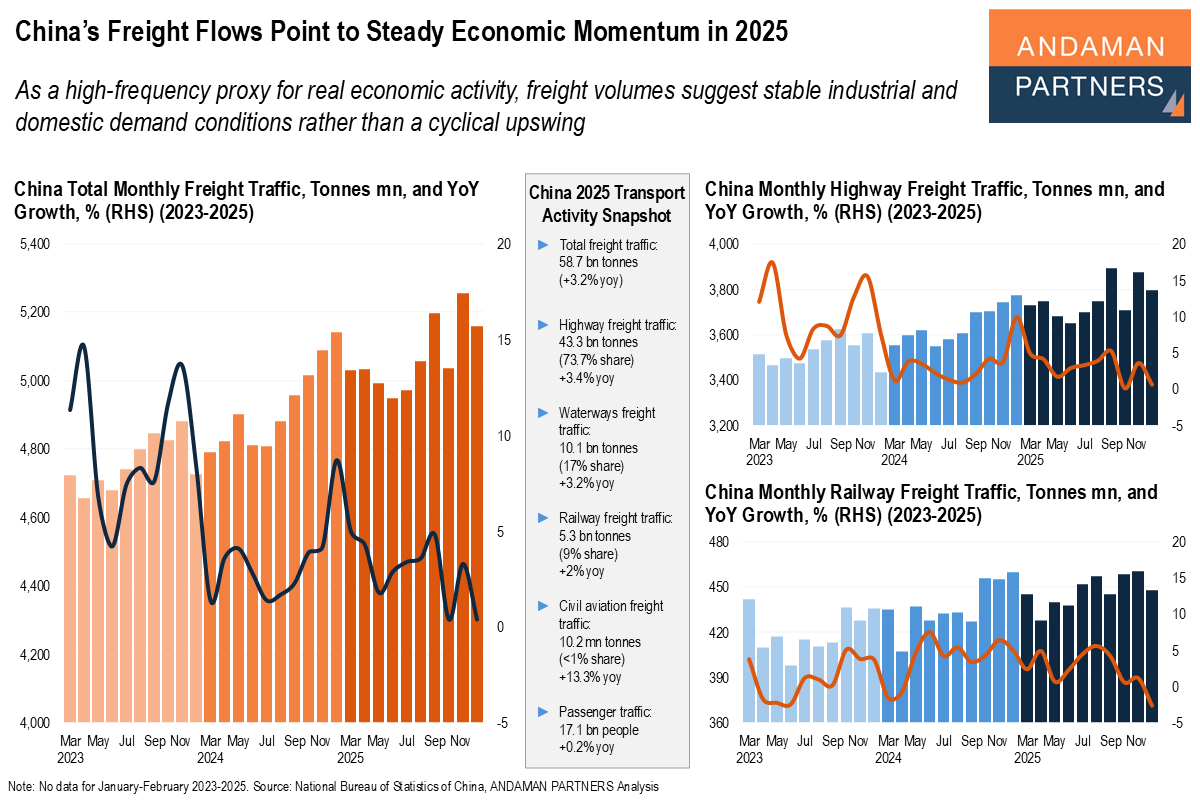

Freight volumes suggest stable conditions in industrial and domestic demand rather than a cyclical upswing.

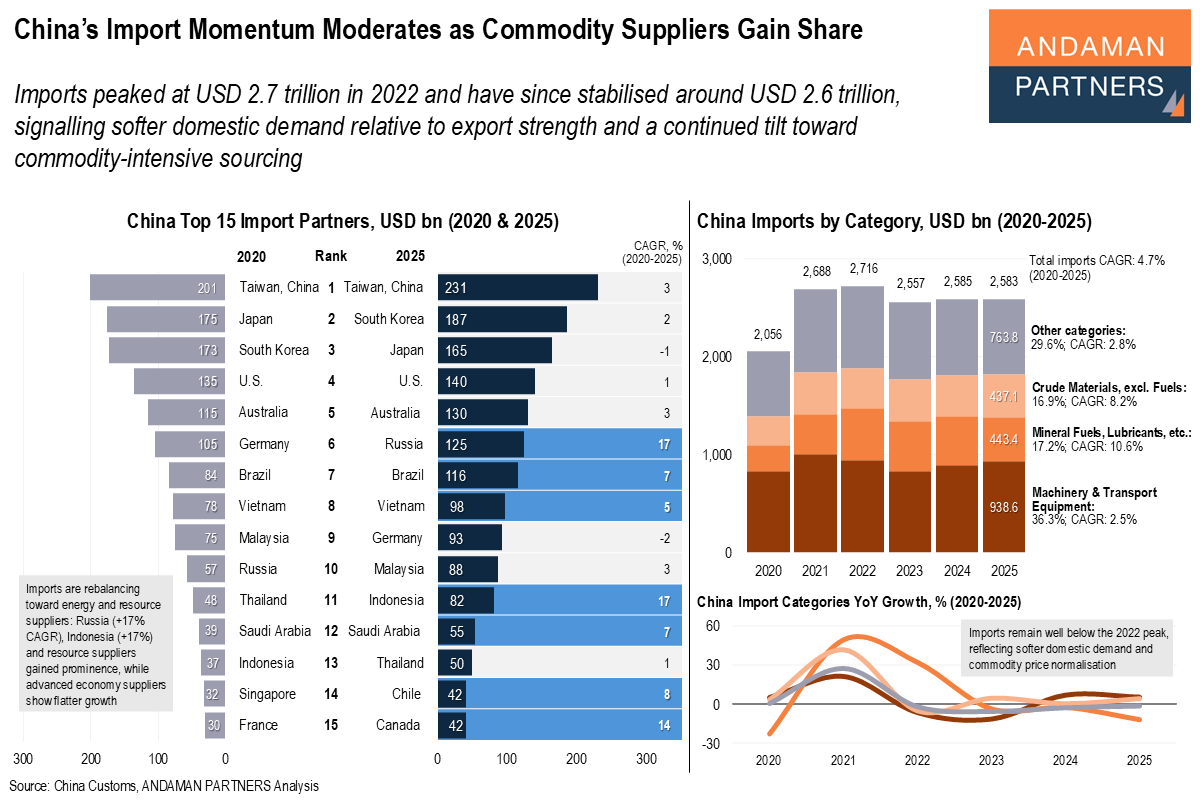

Imports have stabilised around USD 2.6 trillion, signalling softer domestic demand and a continued tilt toward commodity-intensive sourcing.

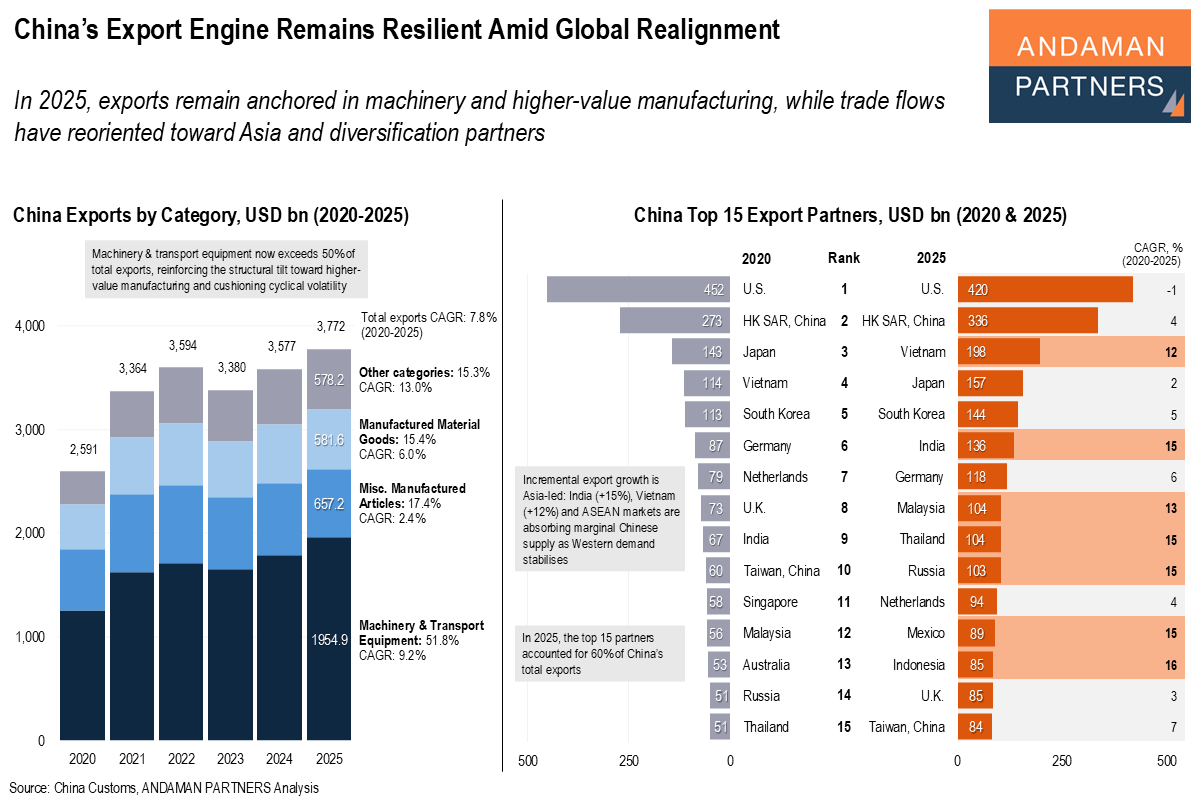

Exports remain anchored in machinery and higher-value manufacturing, while trade flows have reoriented toward Asia and diversification partners.

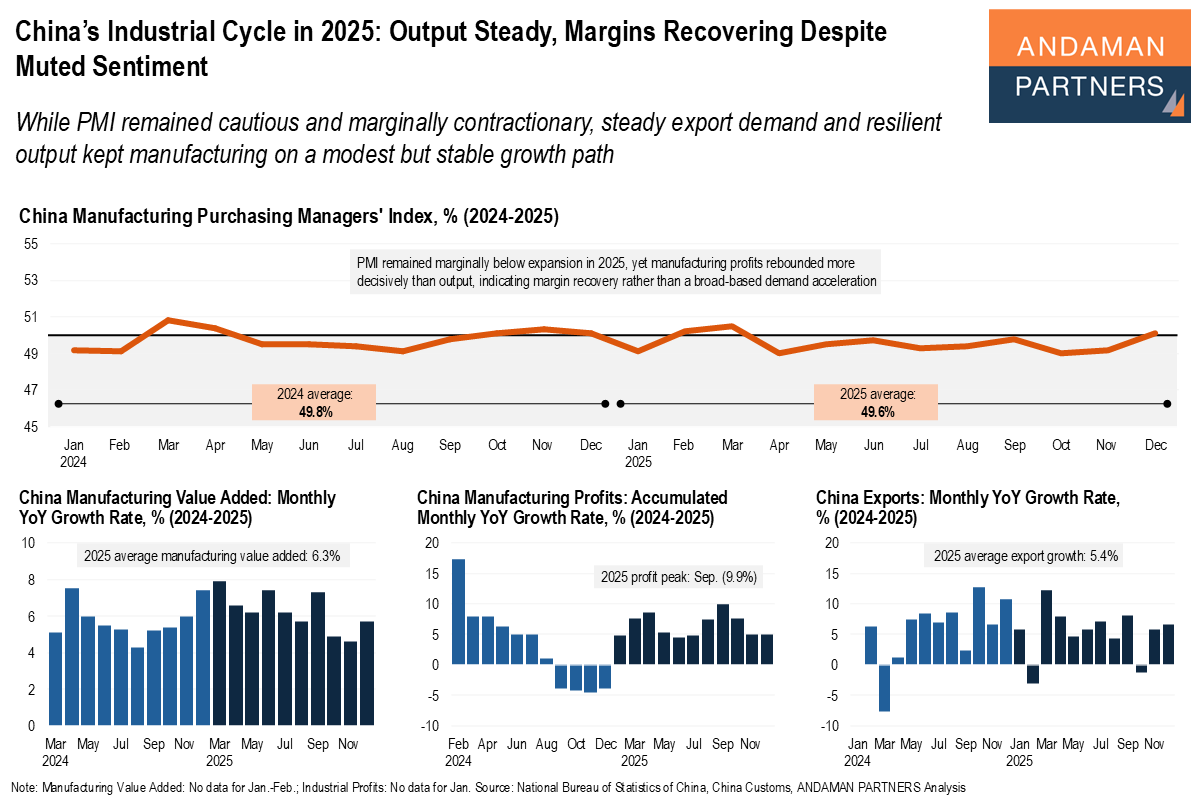

While PMI remained cautious and marginally contractionary, steady export demand and resilient output kept manufacturing on a modest but stable growth path.

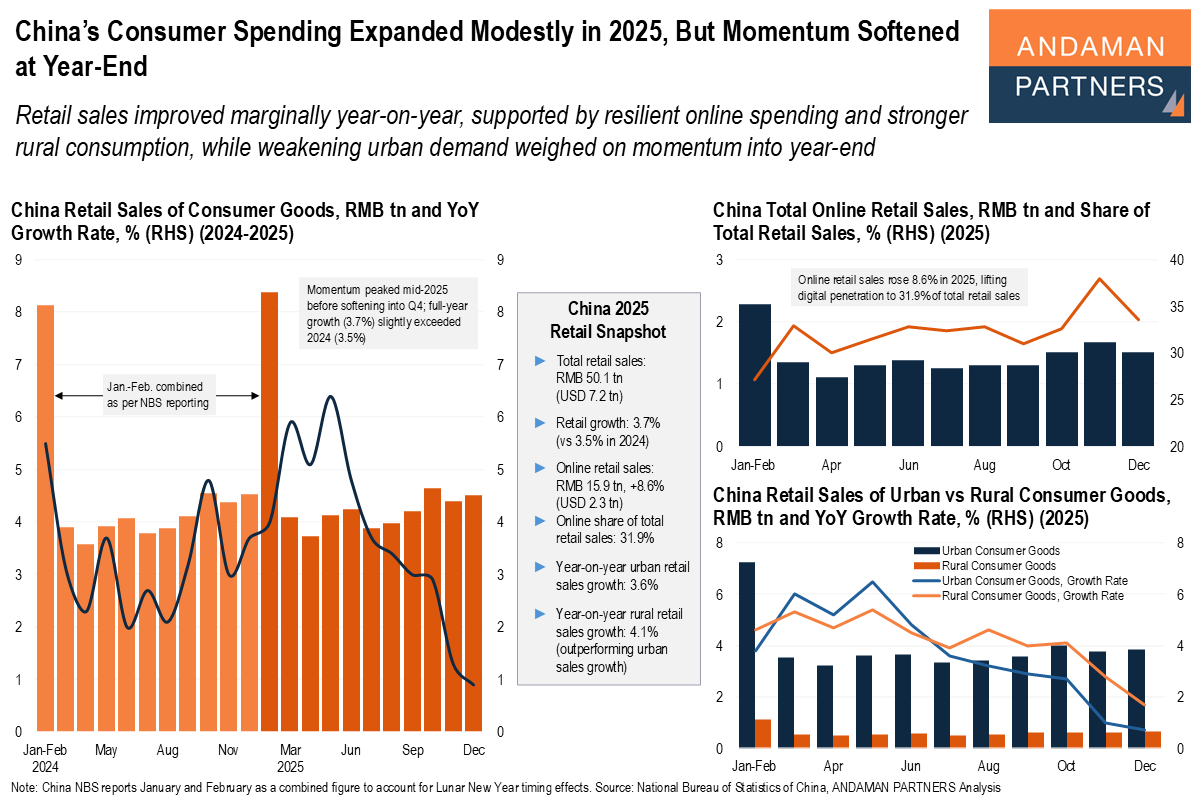

Retail sales improved marginally year-on-year, supported by resilient online spending and stronger rural consumption.