ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

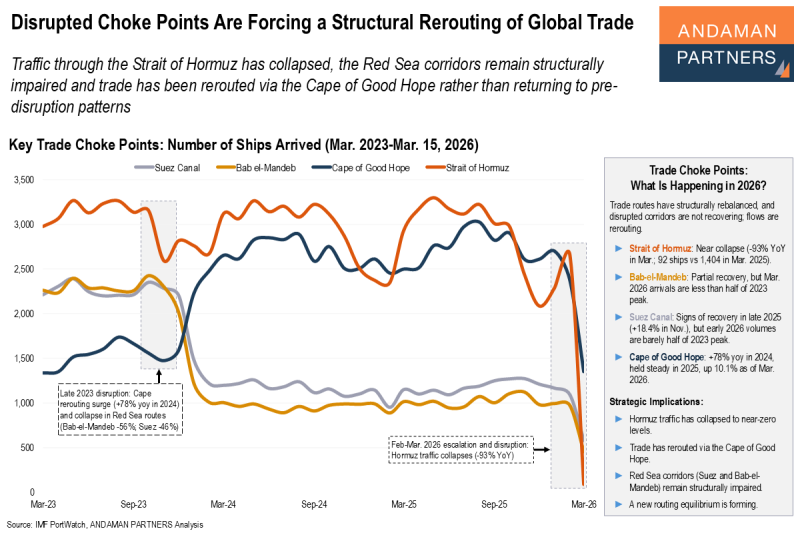

Disrupted Choke Points Are Forcing a Structural Rerouting of Global Trade

Traffic through the Strait of Hormuz has collapsed, the Red Sea corridors remain structurally impaired and trade has been rerouted via the Cape of Good Hope.

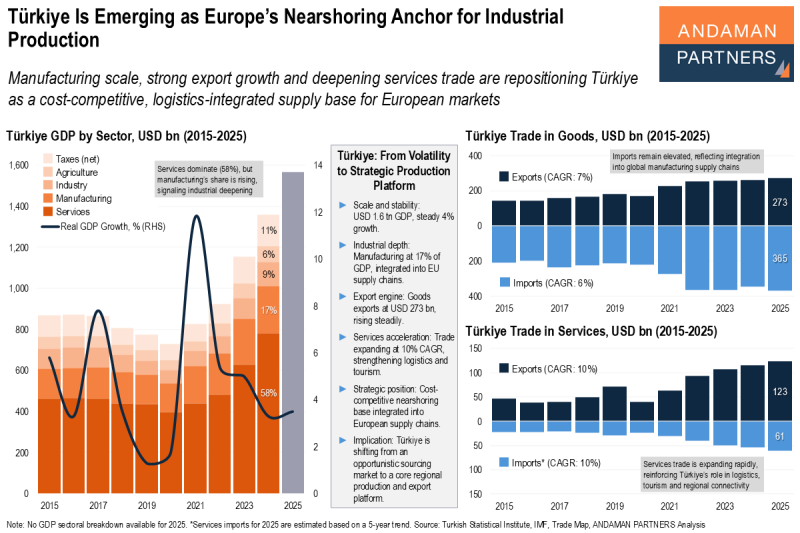

Türkiye Is Emerging as Europe’s Nearshoring Anchor for Industrial Production

Manufacturing scale, strong export growth and deepening services trade are repositioning Türkiye as a cost-competitive supply base for Europe.

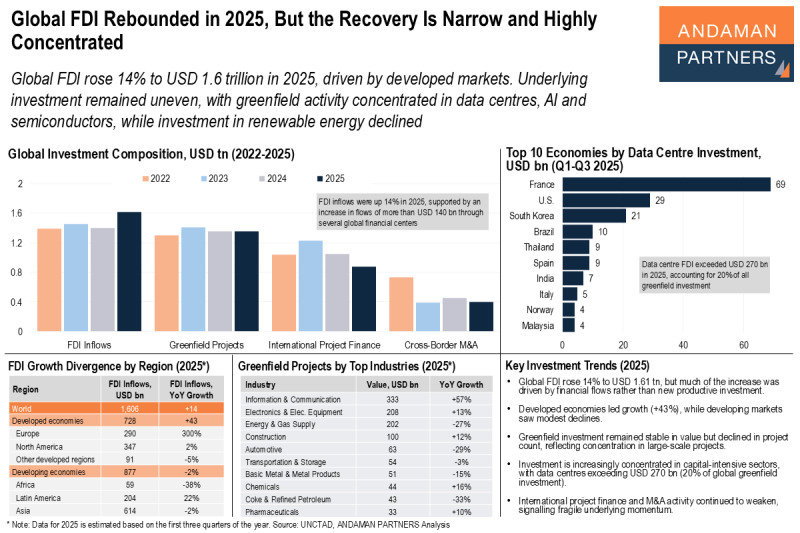

Global FDI Rebounded in 2025, But the Recovery Is Narrow and Highly Concentrated

Investment remained uneven, with greenfield activity concentrated in data centres, AI and semiconductors, while investment in renewable energy declined.