India’s Merchandise Trade Reaches Record Levels Amid Strong Domestic Demand

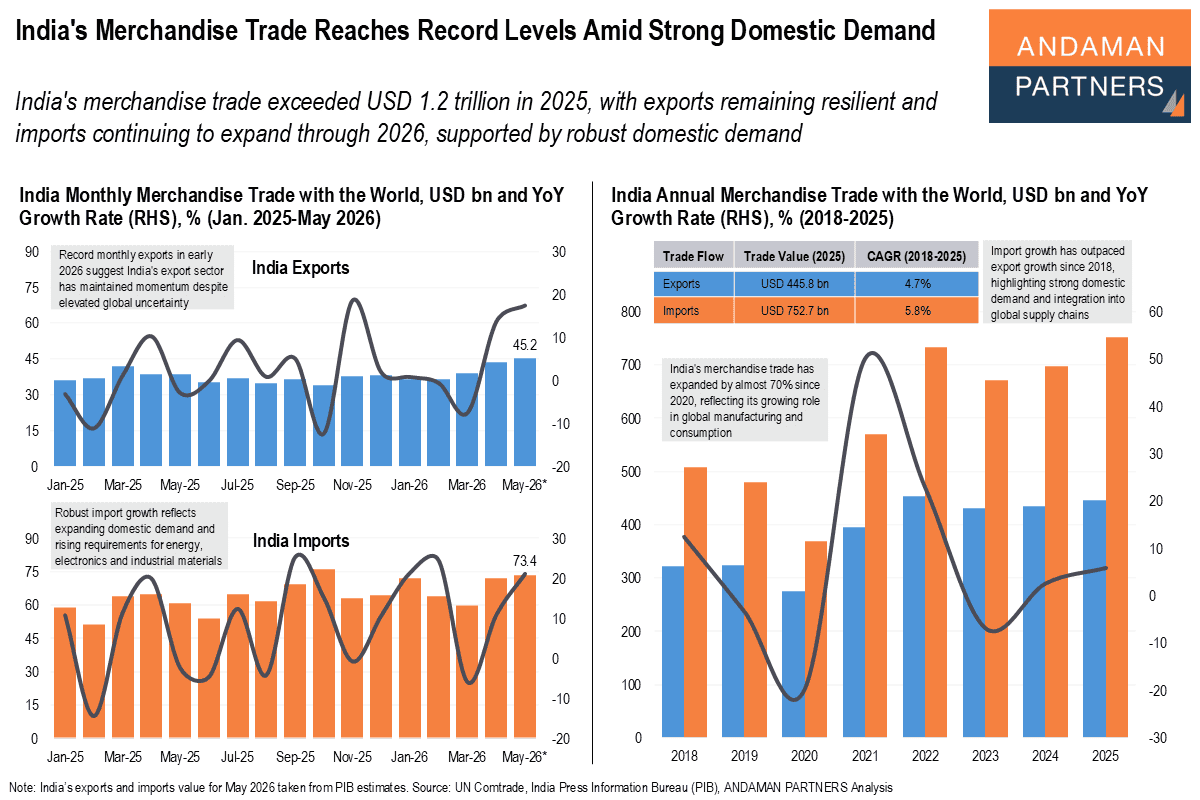

India's merchandise trade exceeded USD 1.2 trillion in 2025, with exports remaining resilient and imports continuing to expand through 2026

India's merchandise trade exceeded USD 1.2 trillion in 2025, with exports remaining resilient and imports continuing to expand through 2026

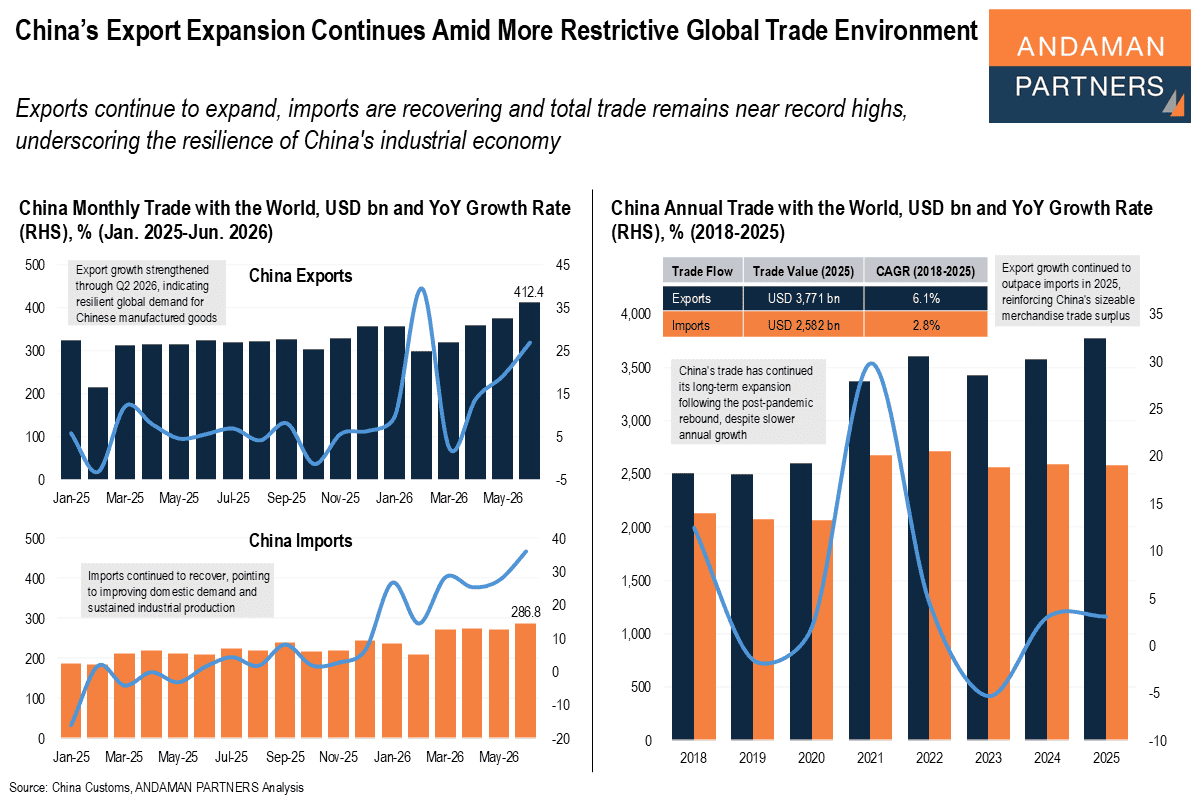

Exports continue to expand, imports are recovering and total trade remains near record highs

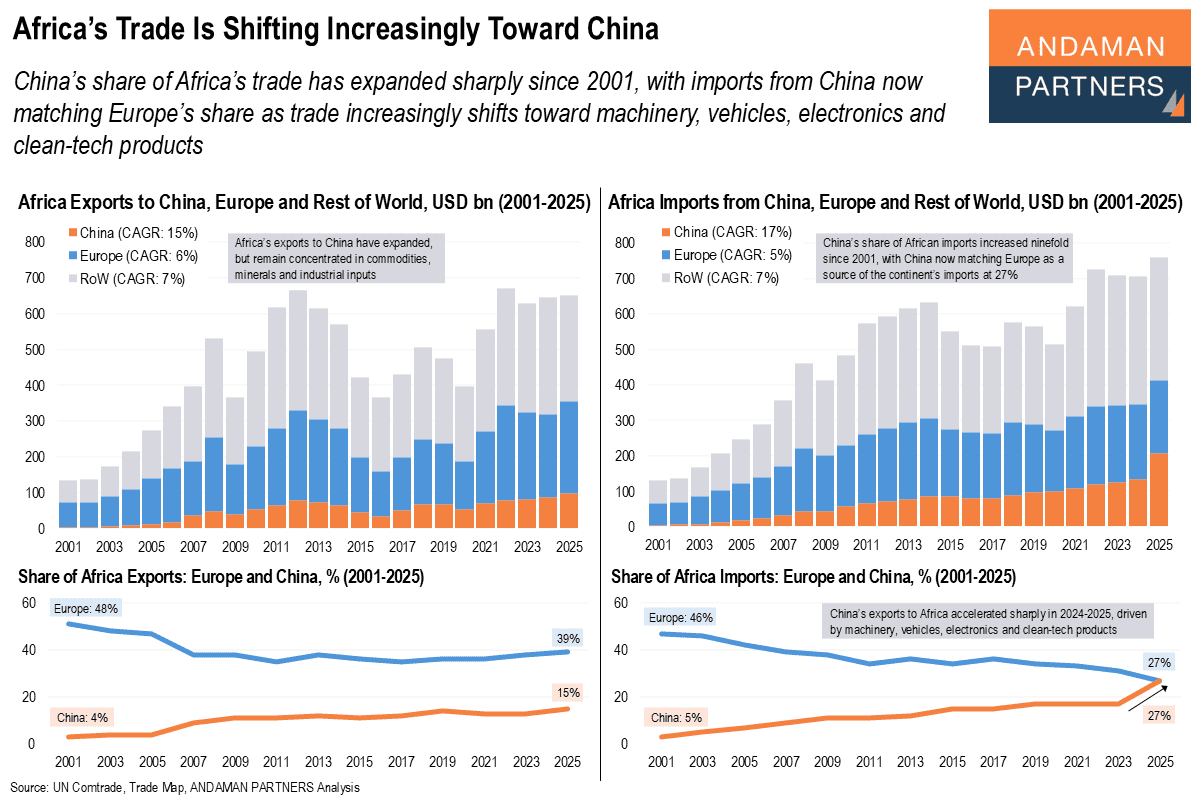

China’s share of Africa’s trade has expanded sharply since 2001, with imports from China now matching Europe’s share

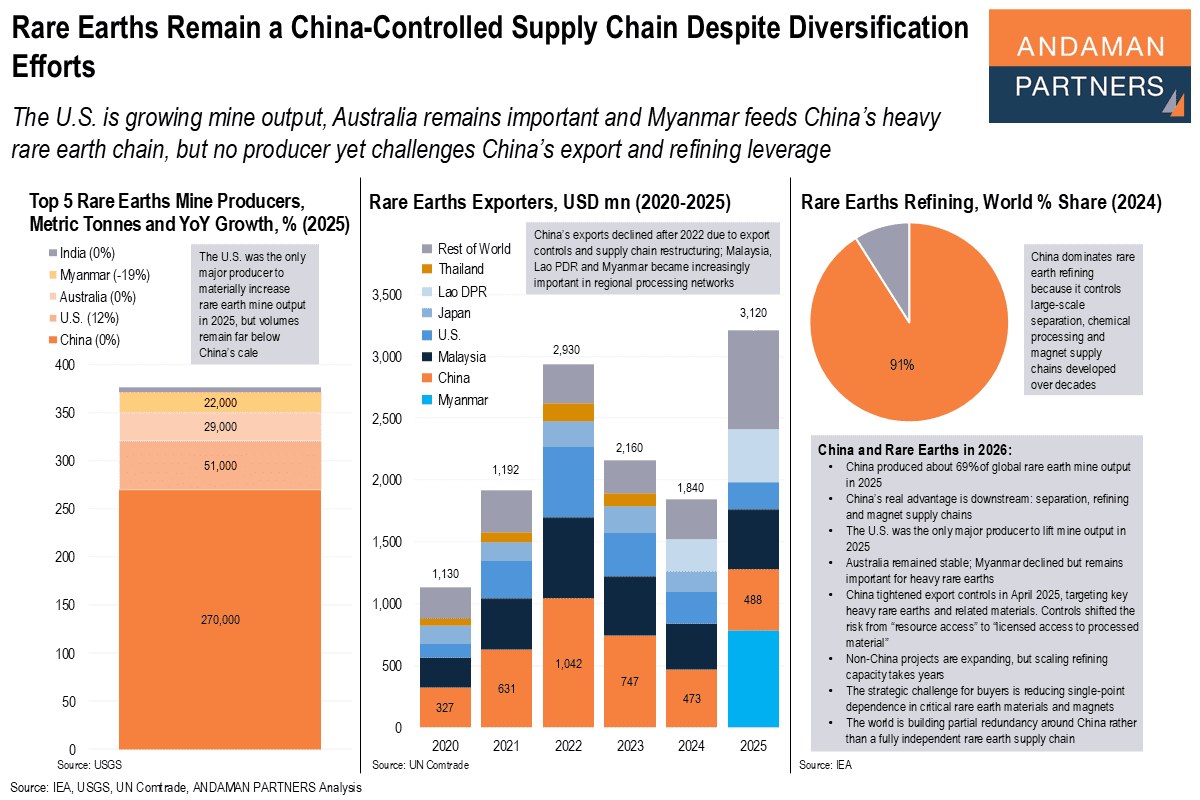

The U.S. is growing mine output, but no producer yet challenges China’s export and refining leverage.

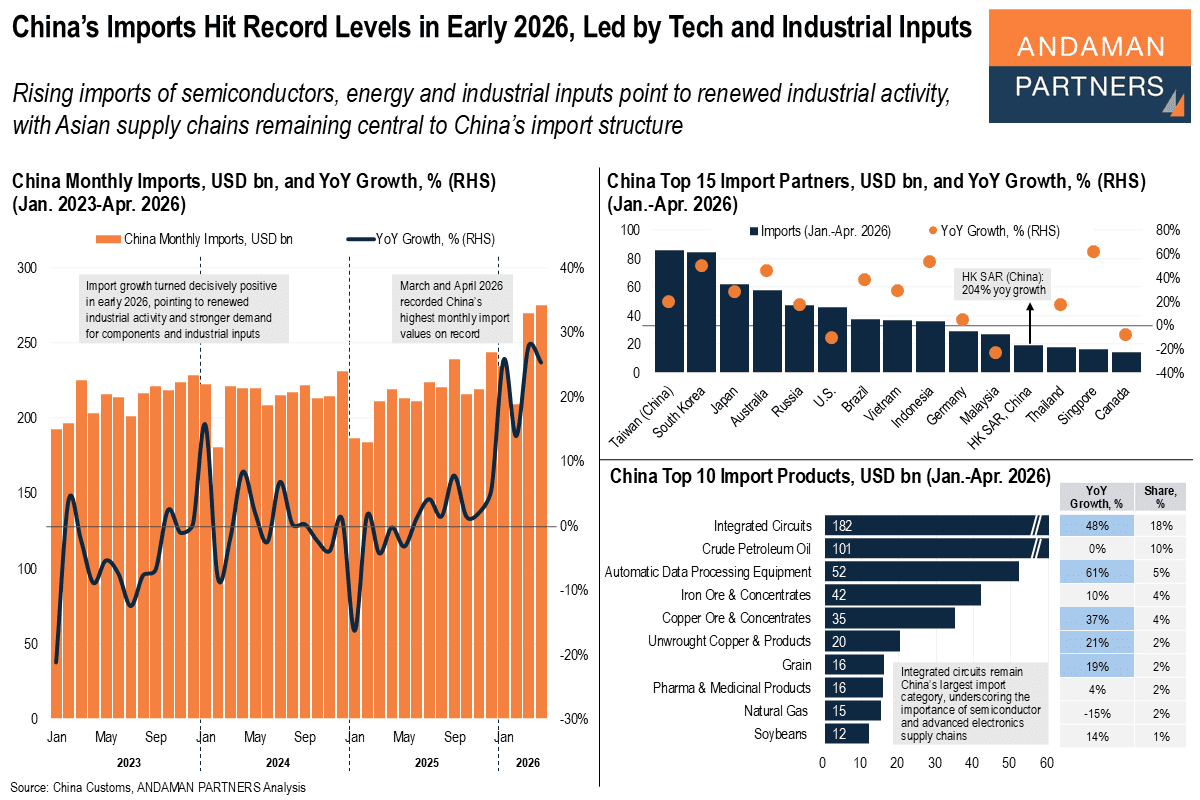

Rising imports of semiconductors, energy and industrial inputs point to renewed industrial activity.

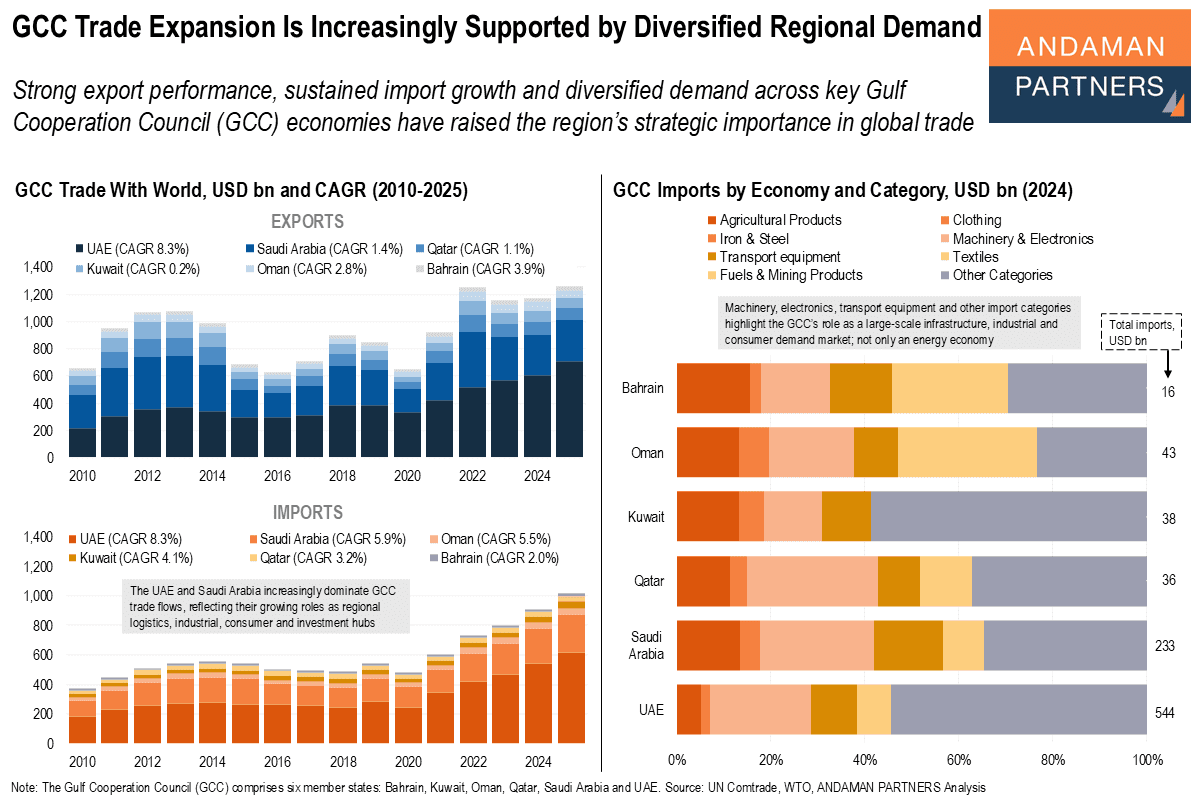

Strong export performance, sustained import growth and diversified demand across the GCC have raised the region’s strategic importance.

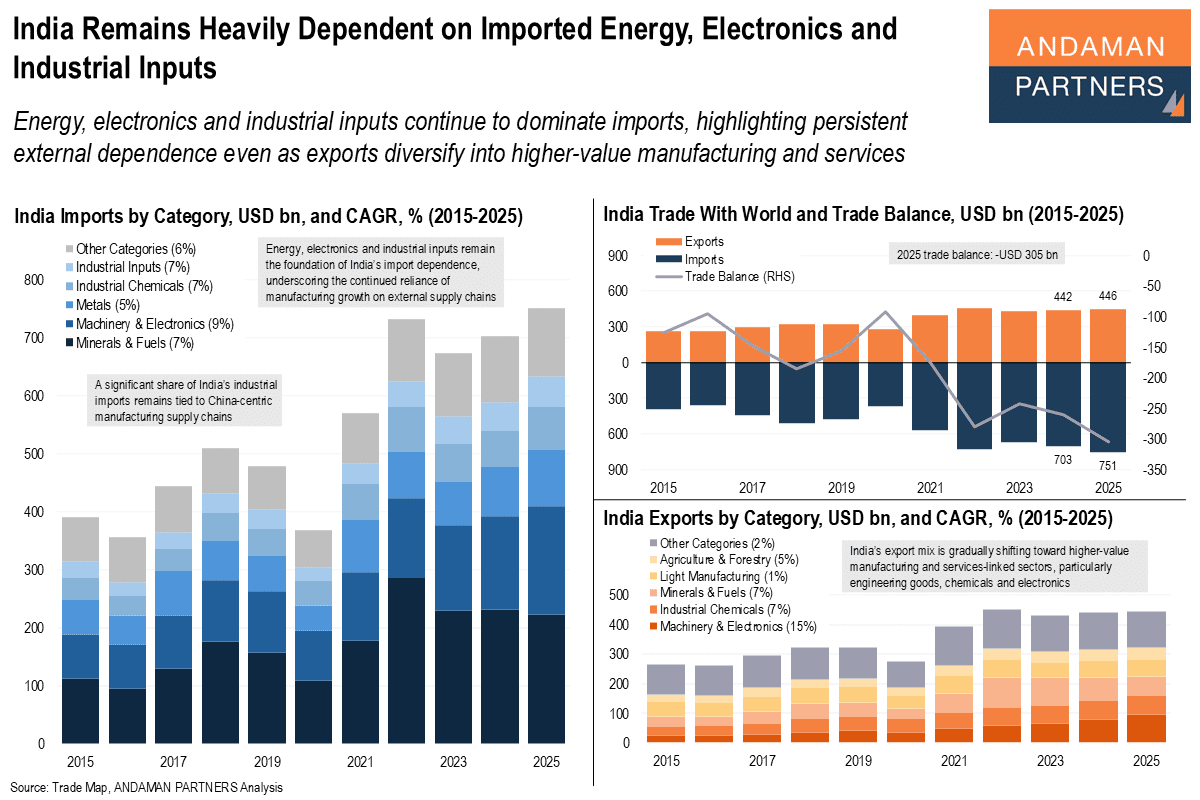

Energy, electronics and industrial inputs continue to dominate India's imports, highlighting persistent external dependence.

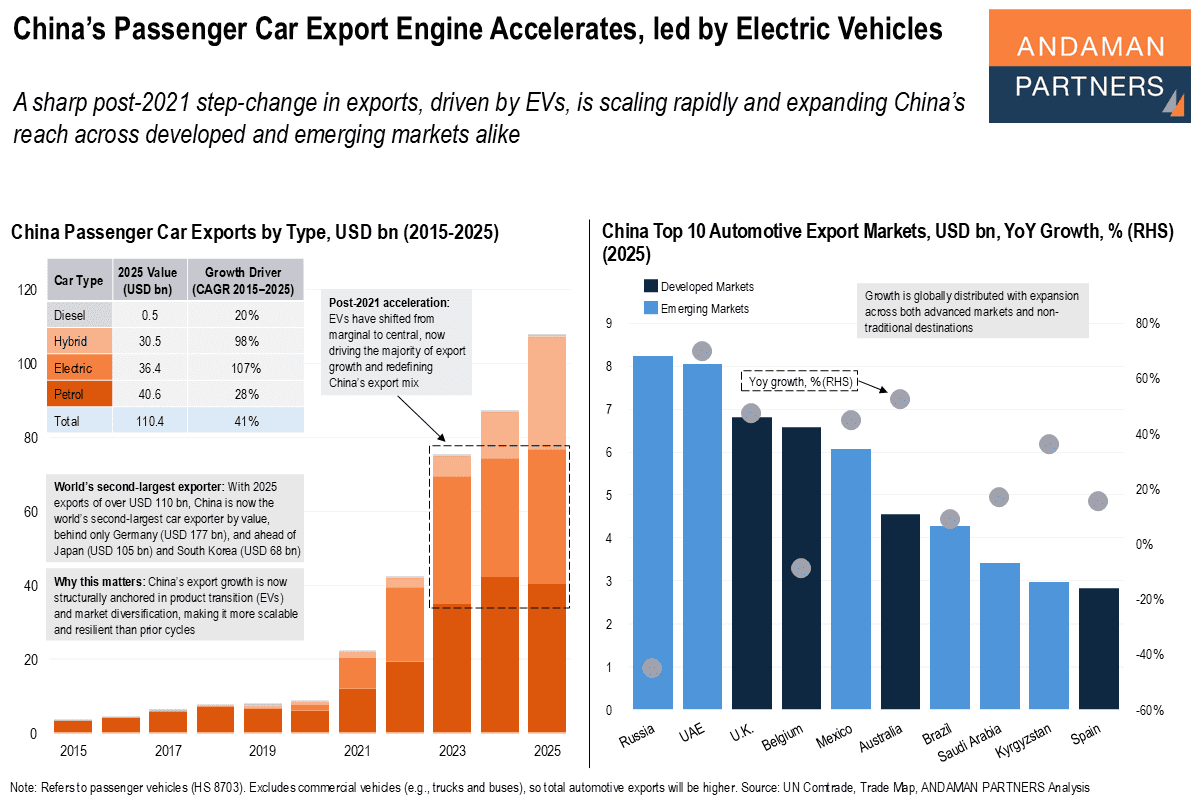

A sharp post-2021 step-change in car exports is scaling rapidly and expanding China’s reach across developed and emerging markets.

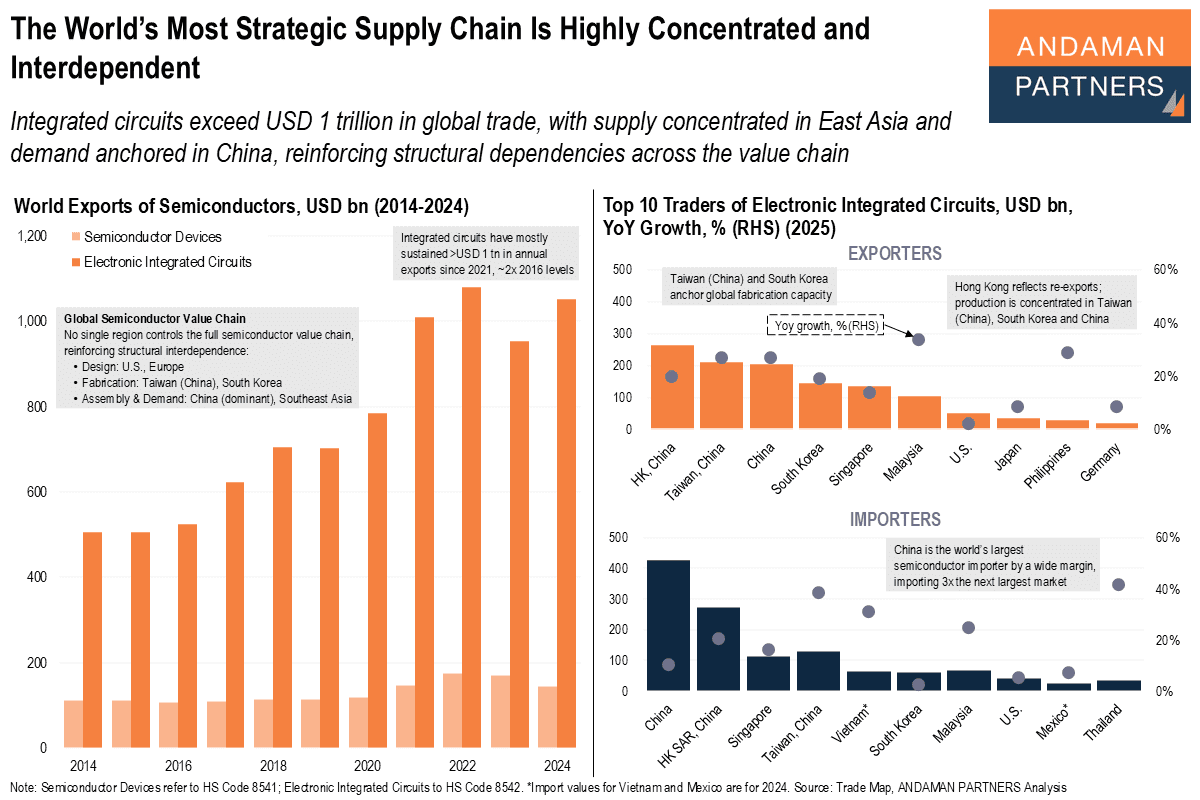

Integrated circuits exceed USD 1 trillion in global trade, with supply concentrated in Asia and demand in China, reinforcing structural dependencies.

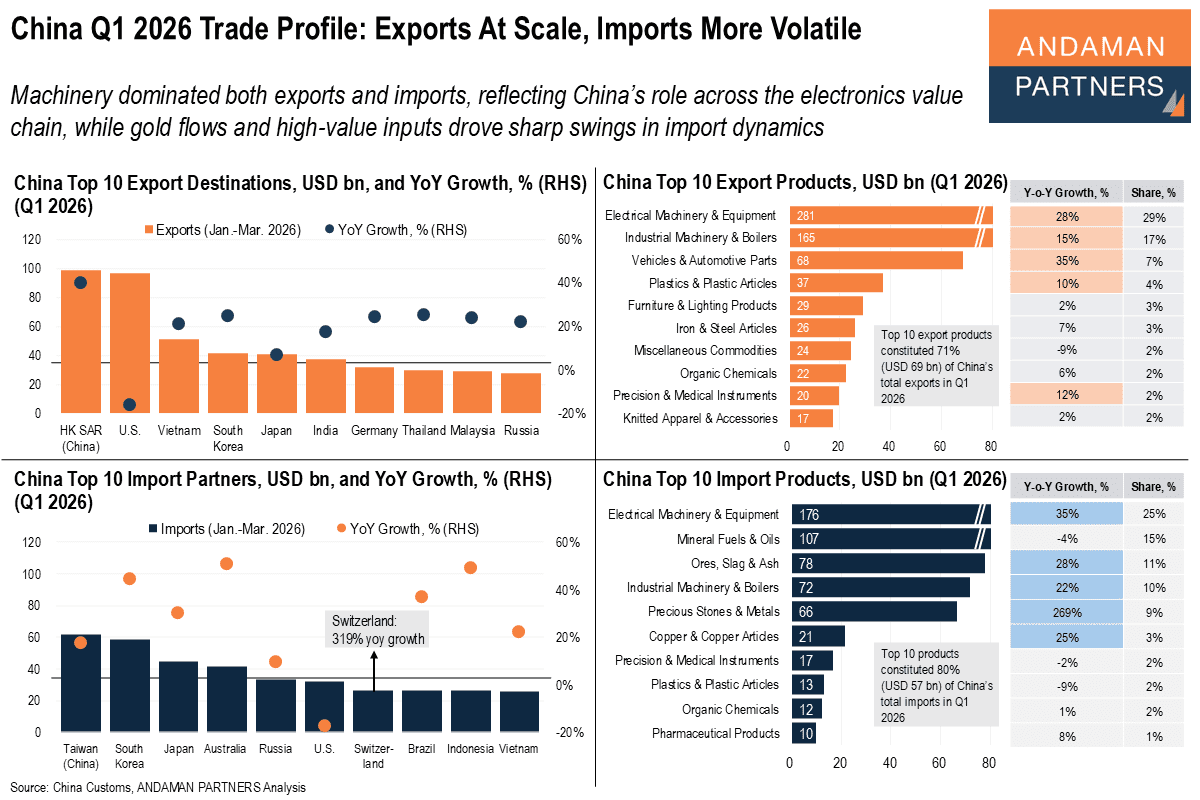

Machinery dominated exports and imports, reflecting China’s role across the electronics value chain; gold and high-value inputs drove import swings.