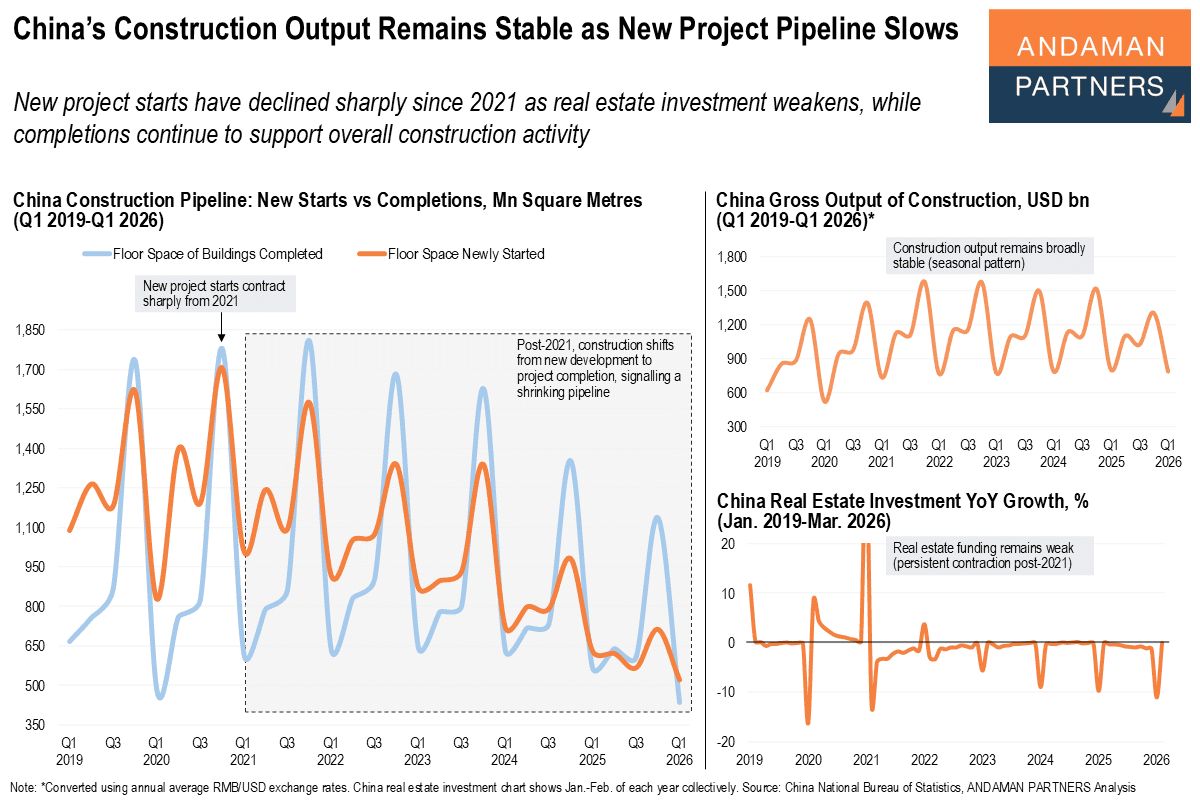

China’s Construction Output Remains Stable as New Project Pipeline Slows

New project starts have declined sharply since 2021 as real estate investment weakens, while completions continue to support overall construction activity.

New project starts have declined sharply since 2021 as real estate investment weakens, while completions continue to support overall construction activity.

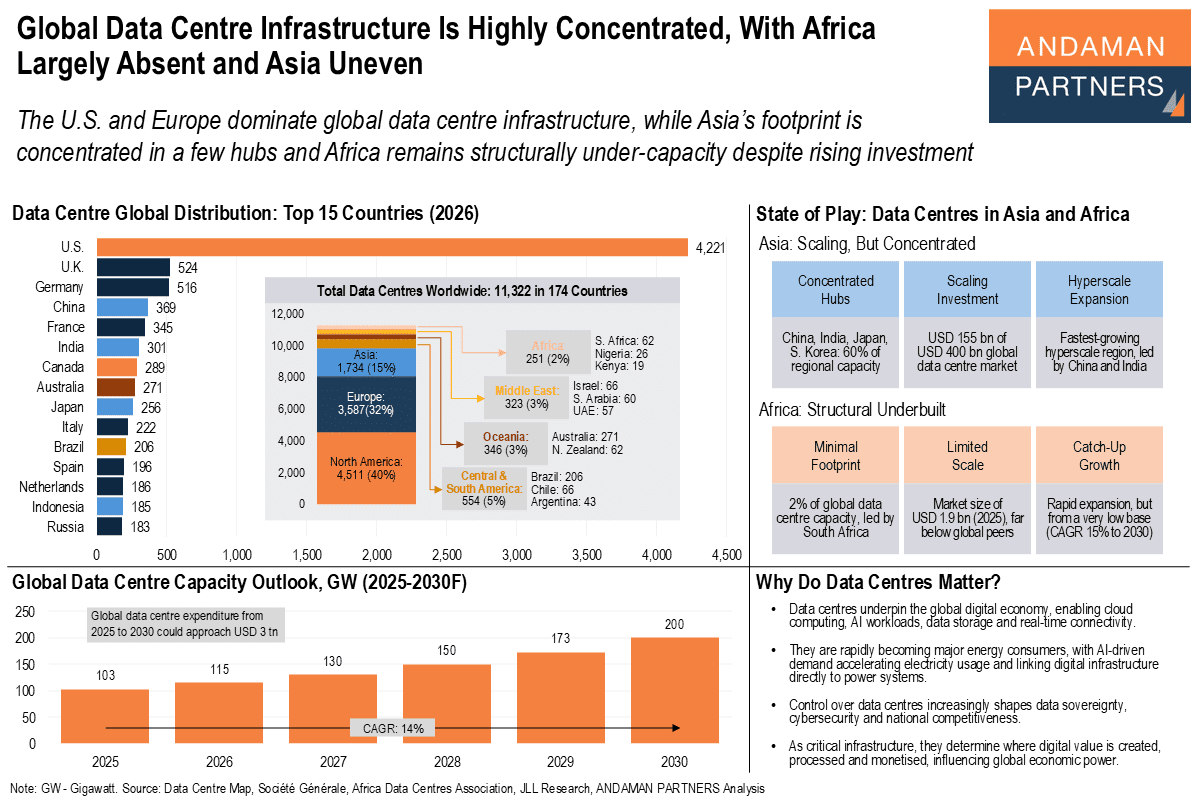

The U.S. and Europe dominate global data centre infrastructure, while Asia’s footprint is concentrated in a few hubs

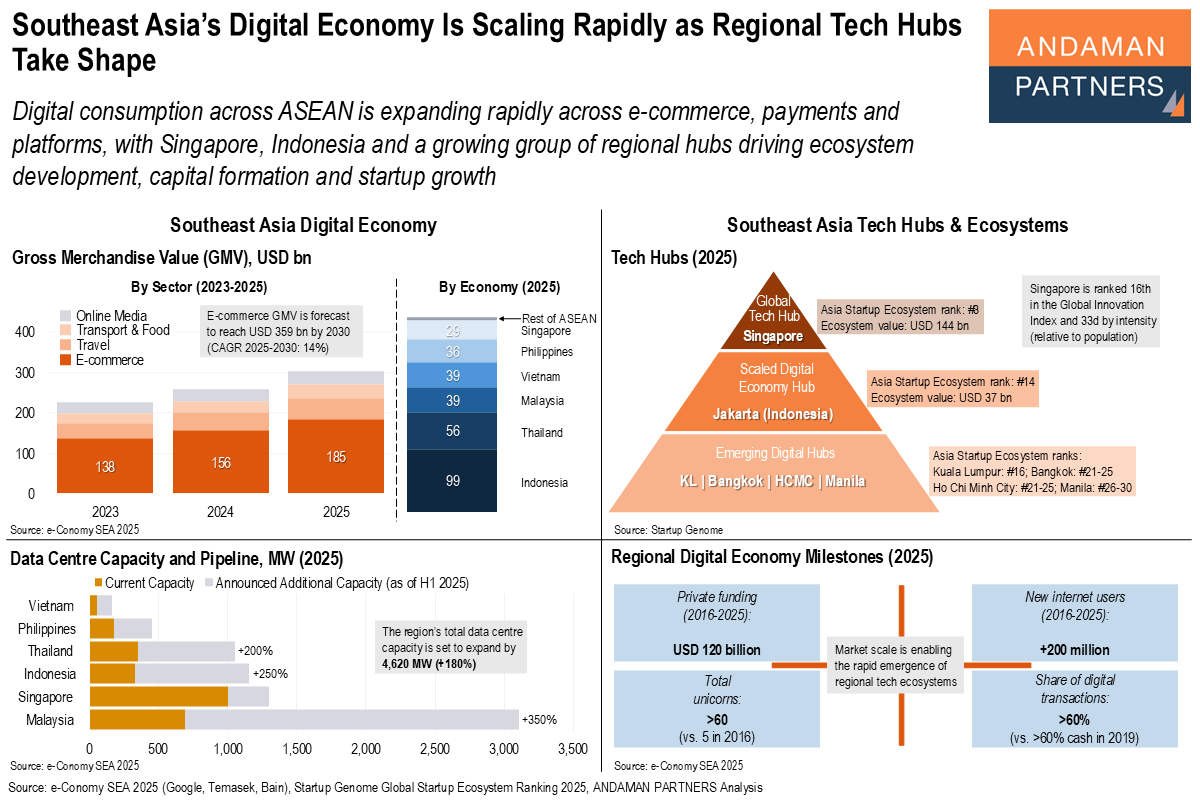

Digital consumption across Southeast Asia is expanding rapidly across e-commerce, payments and platforms.

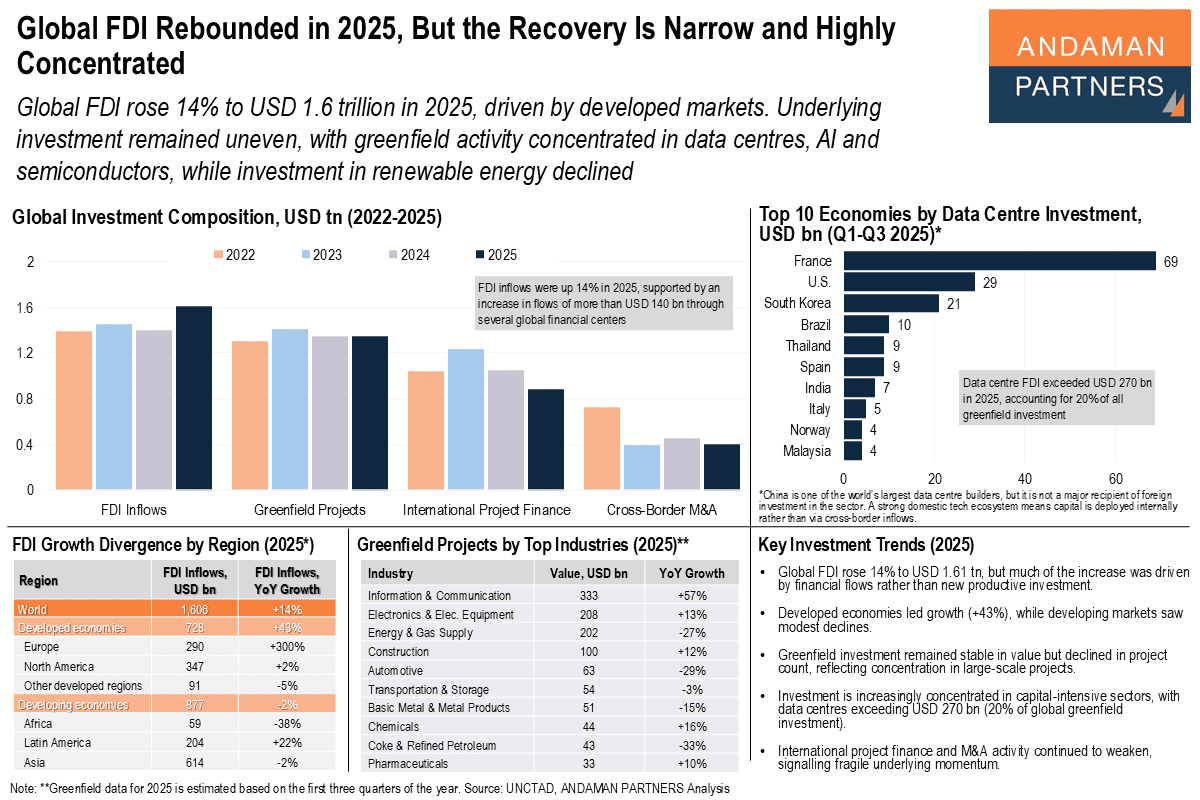

Investment remained uneven, with greenfield activity concentrated in data centres, AI and semiconductors.

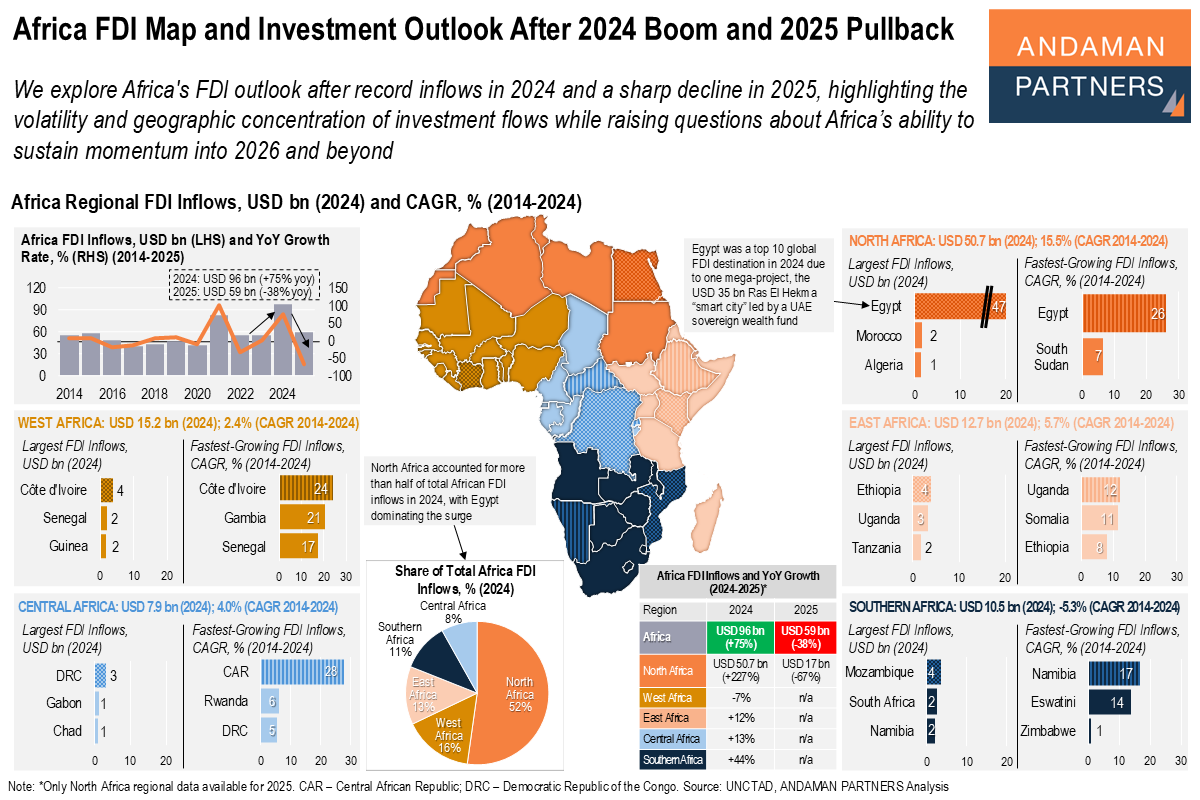

The volatility and geographic concentration of investment flows raises questions about Africa’s ability to sustain momentum into 2026 and beyond.

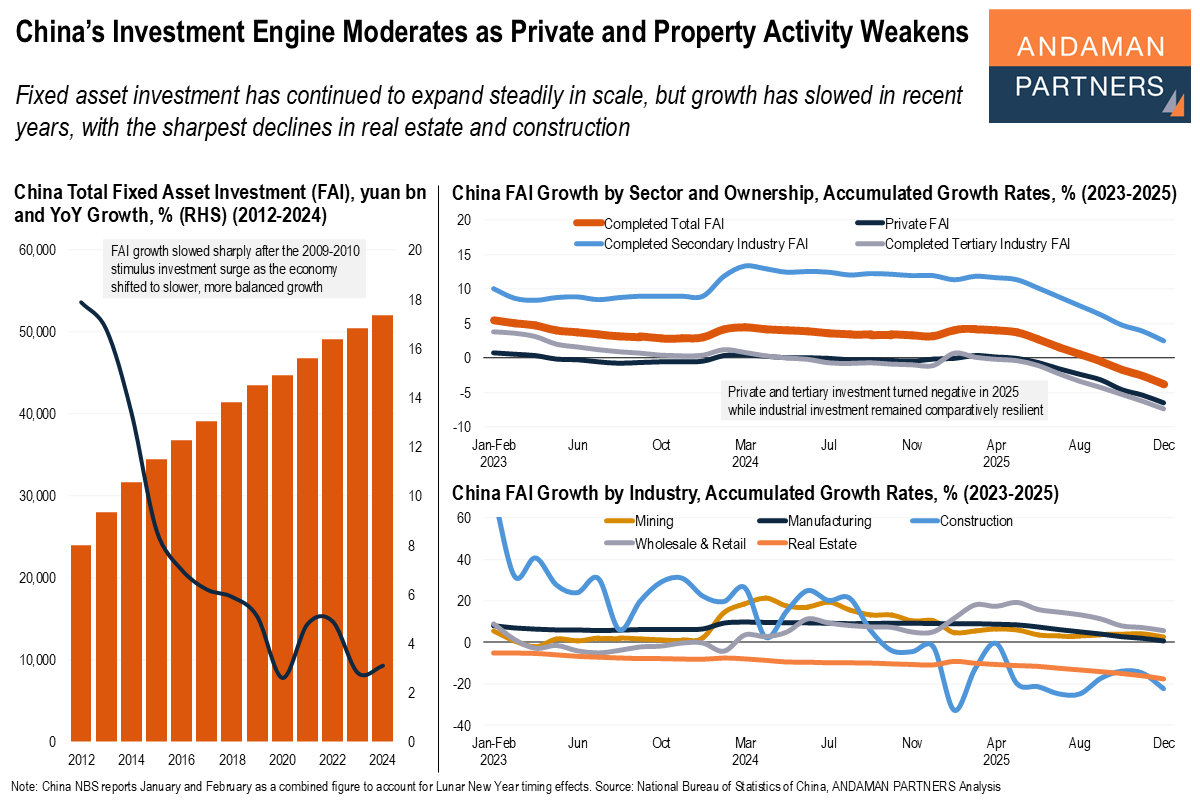

Fixed asset investment has continued to expand steadily, but growth has slowed in recent years, with the sharpest declines in real estate and construction.

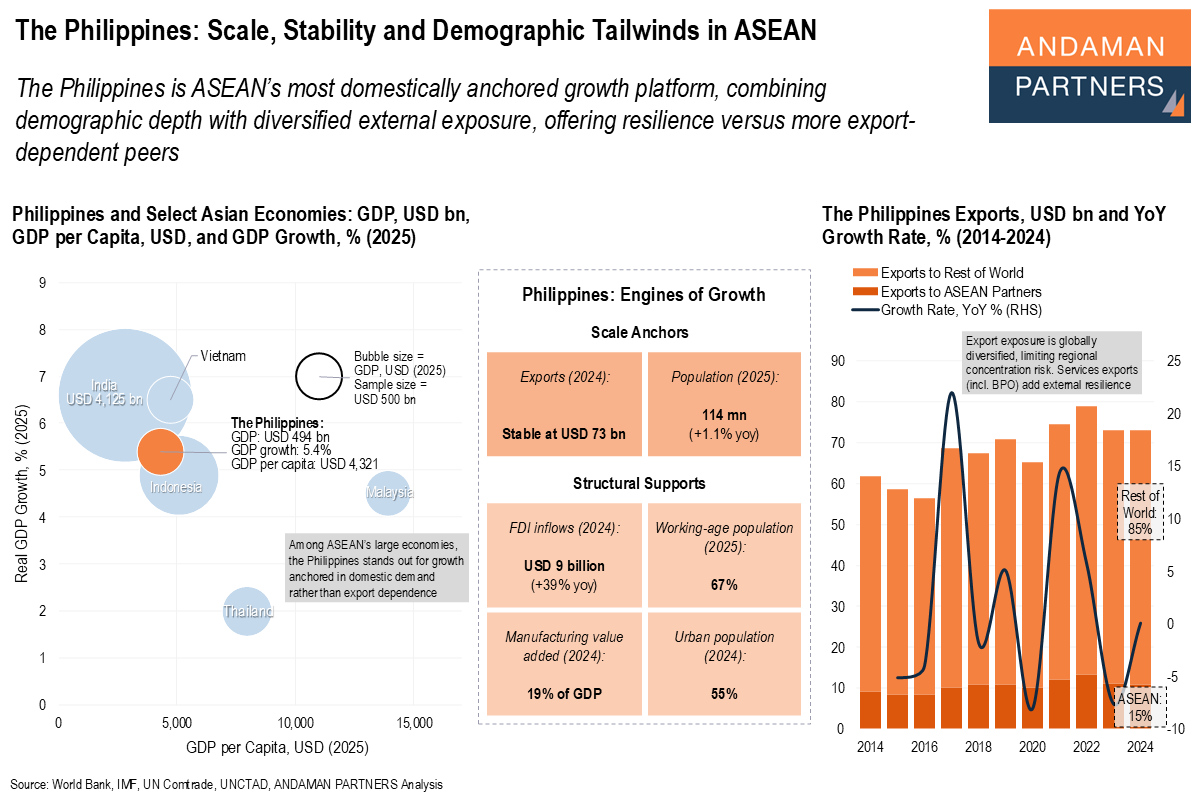

The Philippines is ASEAN’s most domestically anchored growth platform, combining demographic depth with diversified external exposure.

Diversified global trade exposure, strong manufacturing intensity and rising FDI underpin resilient growth with lower volatility than many regional peers.

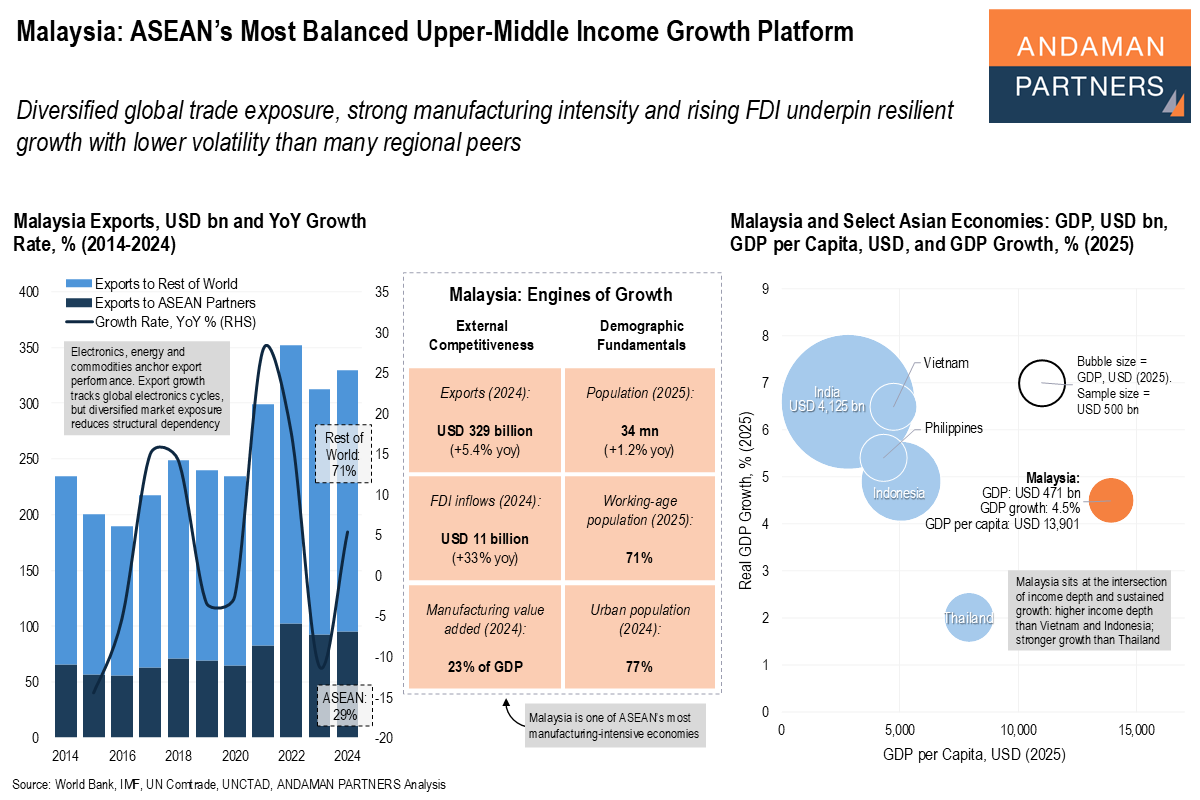

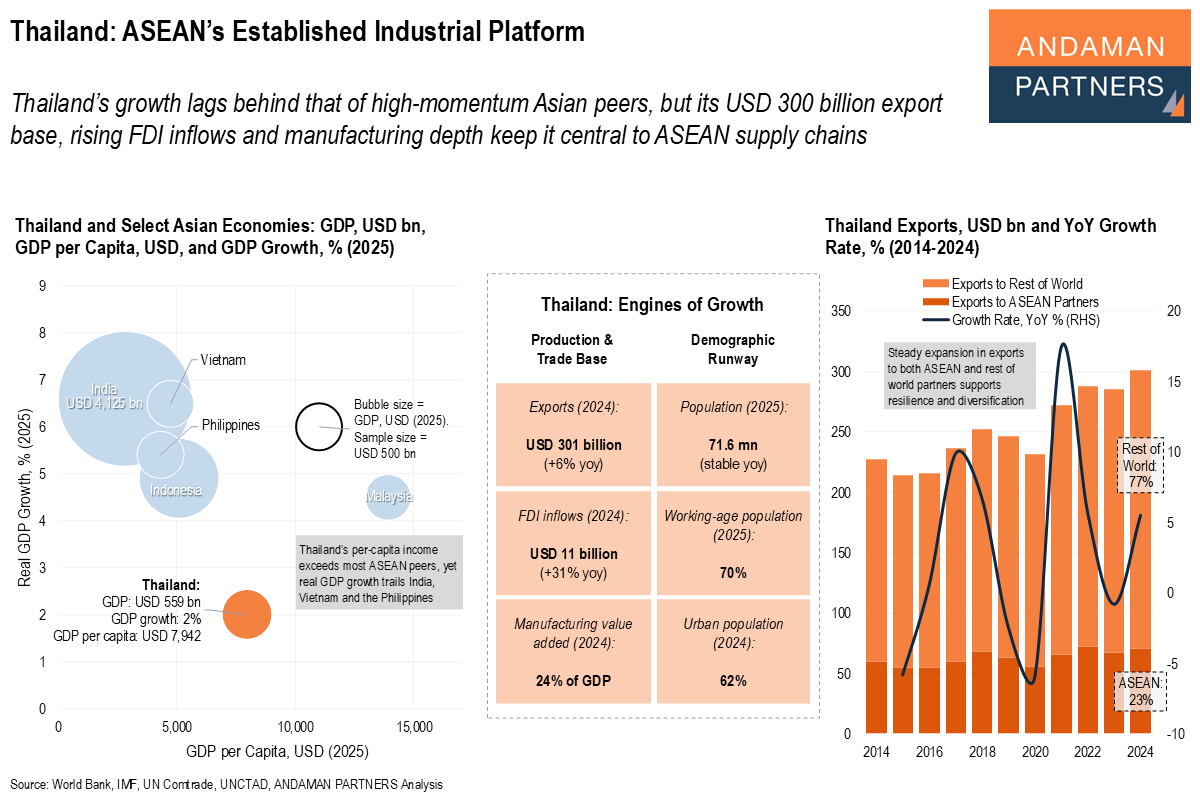

Thailand’s USD 300 billion export base, rising FDI inflows and manufacturing depth keep it central to ASEAN supply chains.

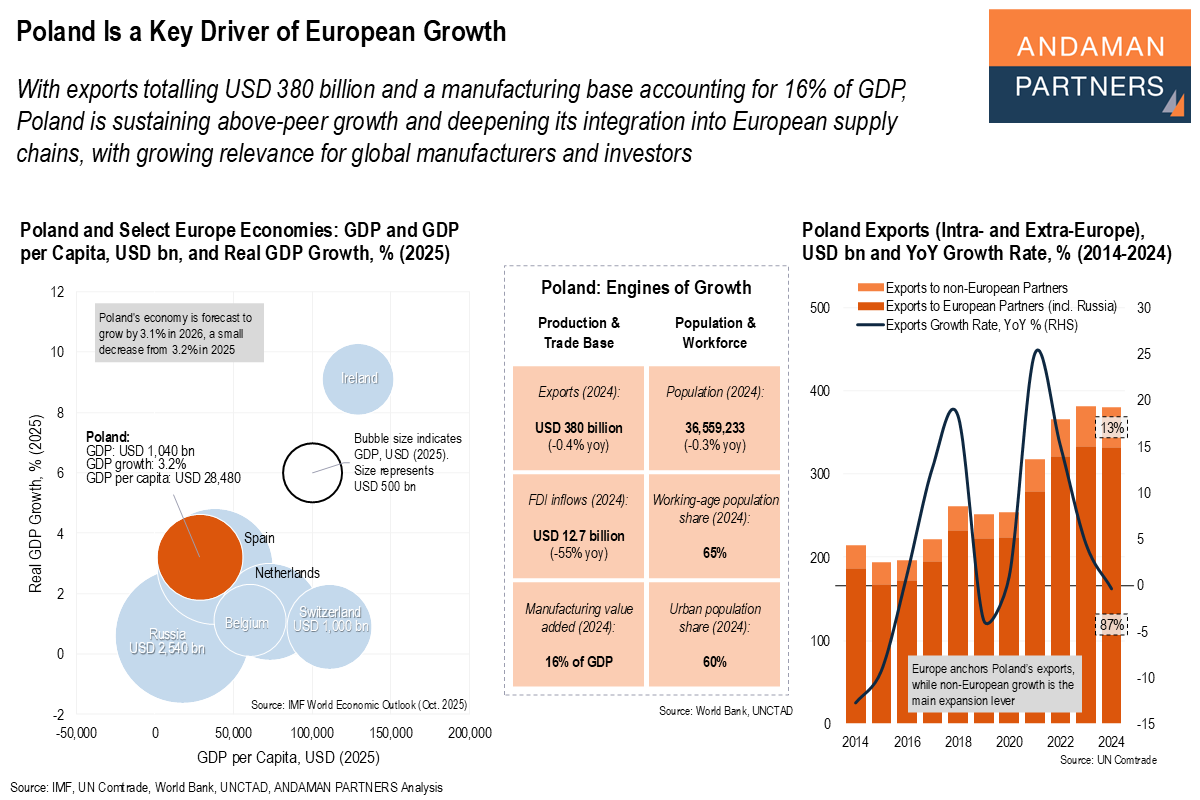

Poland is sustaining above-peer growth and deepening its integration into European supply chains.