Global Copper Demand Rises as Mine Supply Tightens While China Anchors the Market

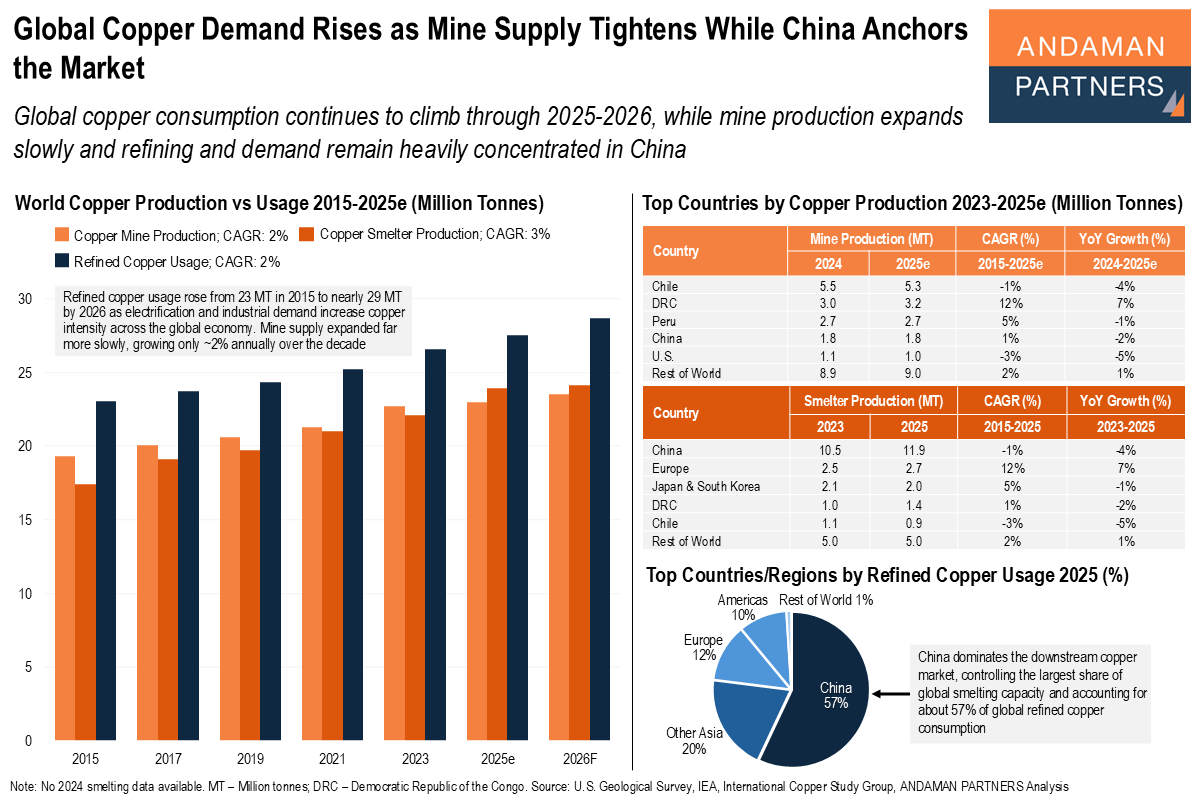

Global copper consumption continues to climb, and mine production expands slowly, while refining and demand remain heavily concentrated in China.

Global copper consumption continues to climb, and mine production expands slowly, while refining and demand remain heavily concentrated in China.

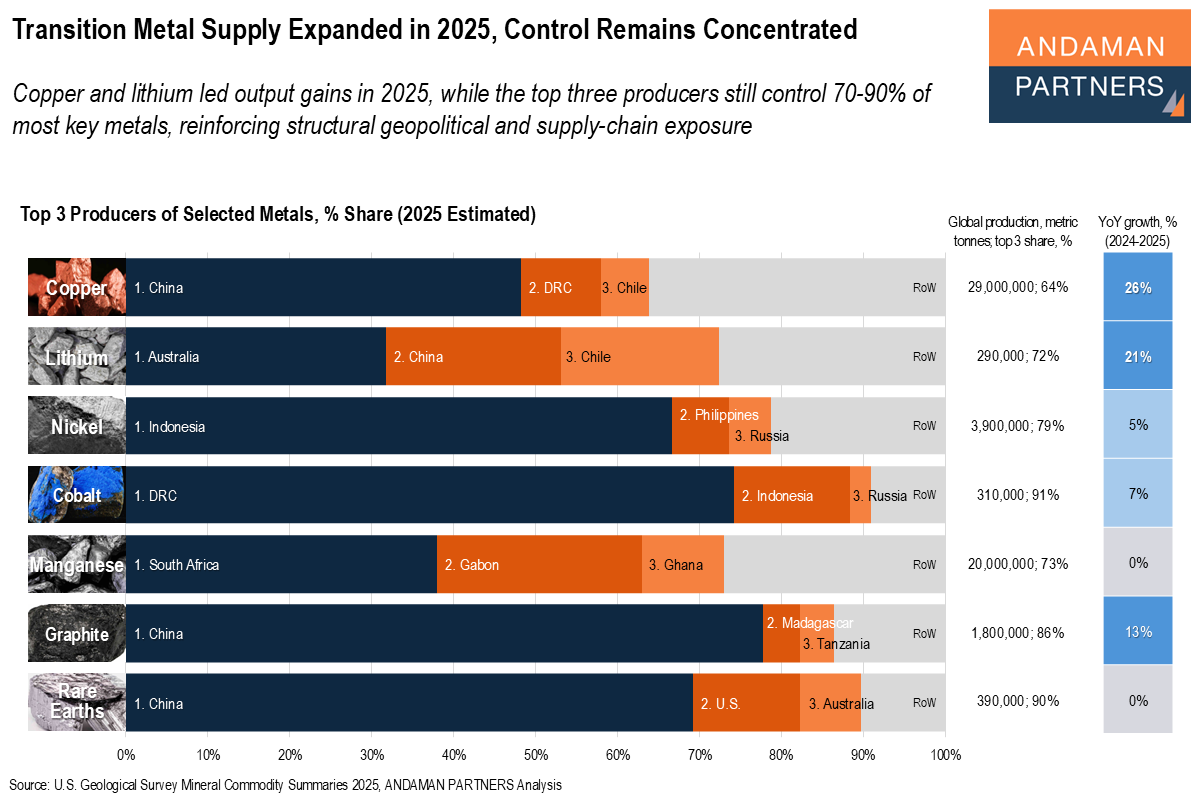

Copper and lithium led output gains in 2025, while the top three producers still control 70-90% of most key metals.

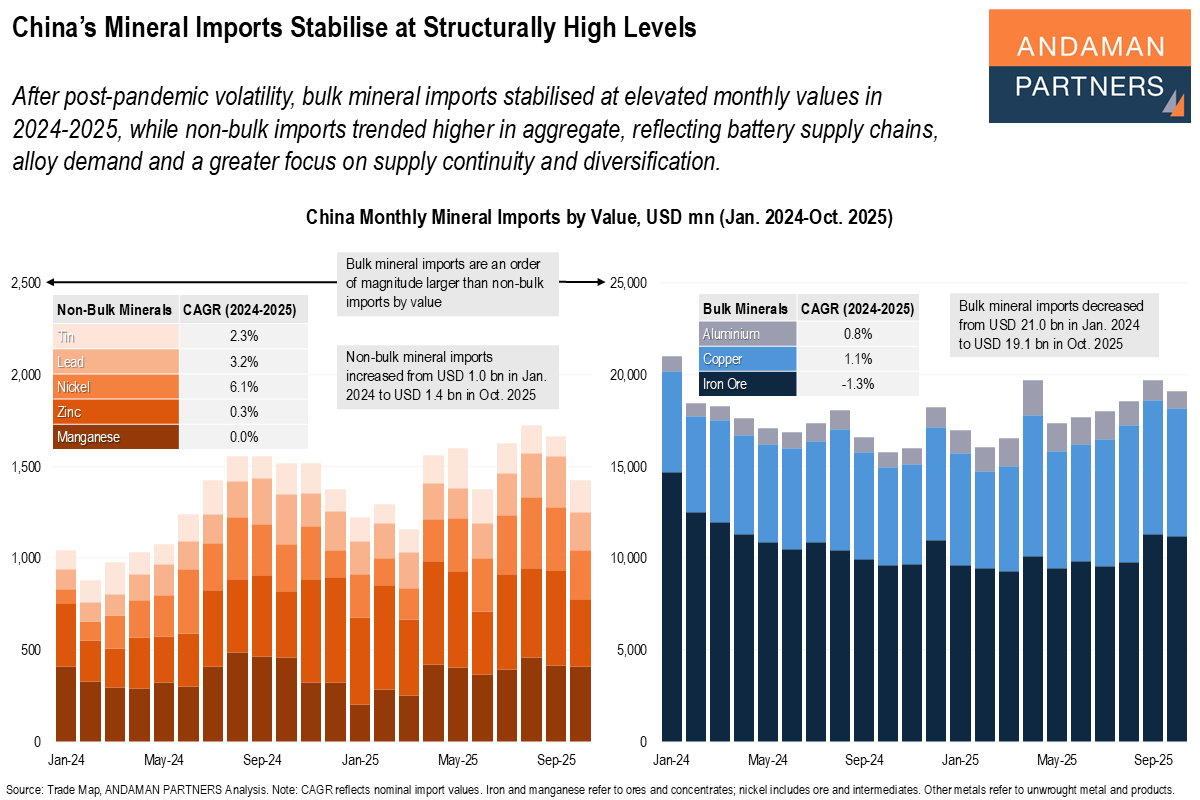

Bulk mineral imports stabilised at elevated monthly values in 2024-2025, while non-bulk imports trended higher in aggregate.

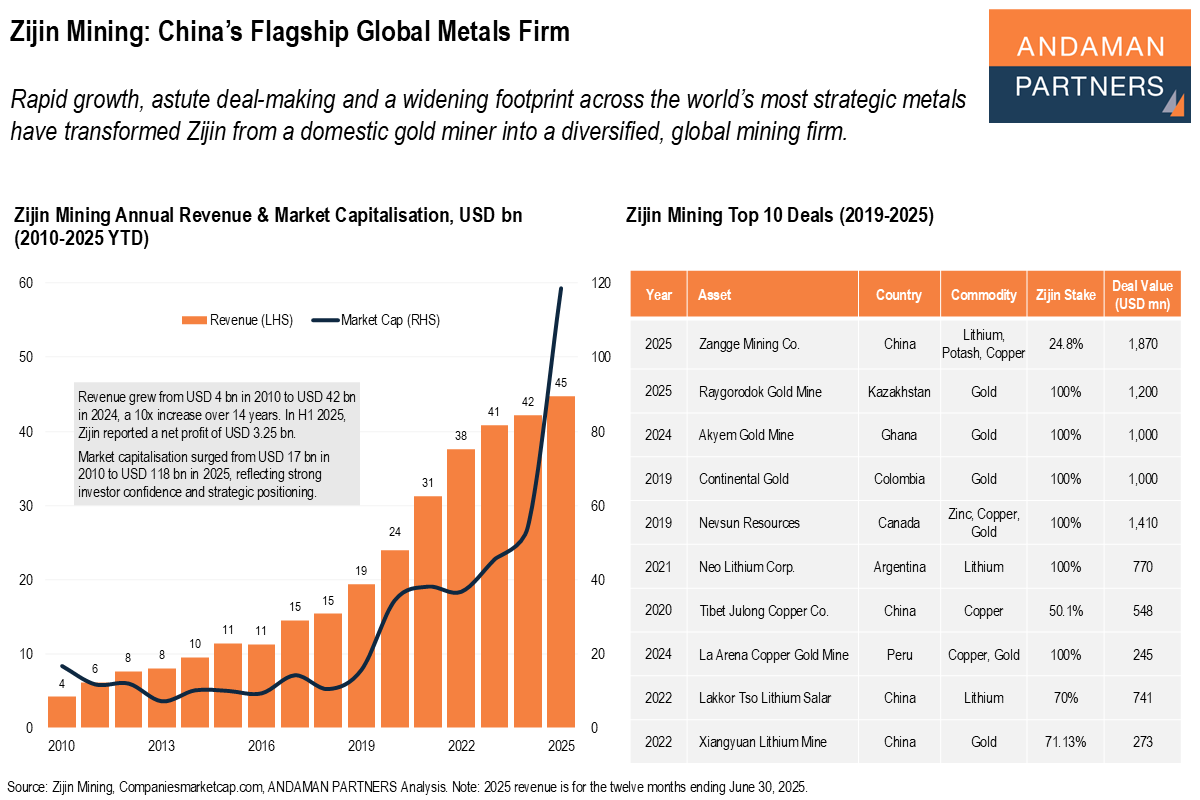

Rapid growth, astute deal-making and a widening footprint across strategic metals have transformed Zijin into a diversified, global mining firm.

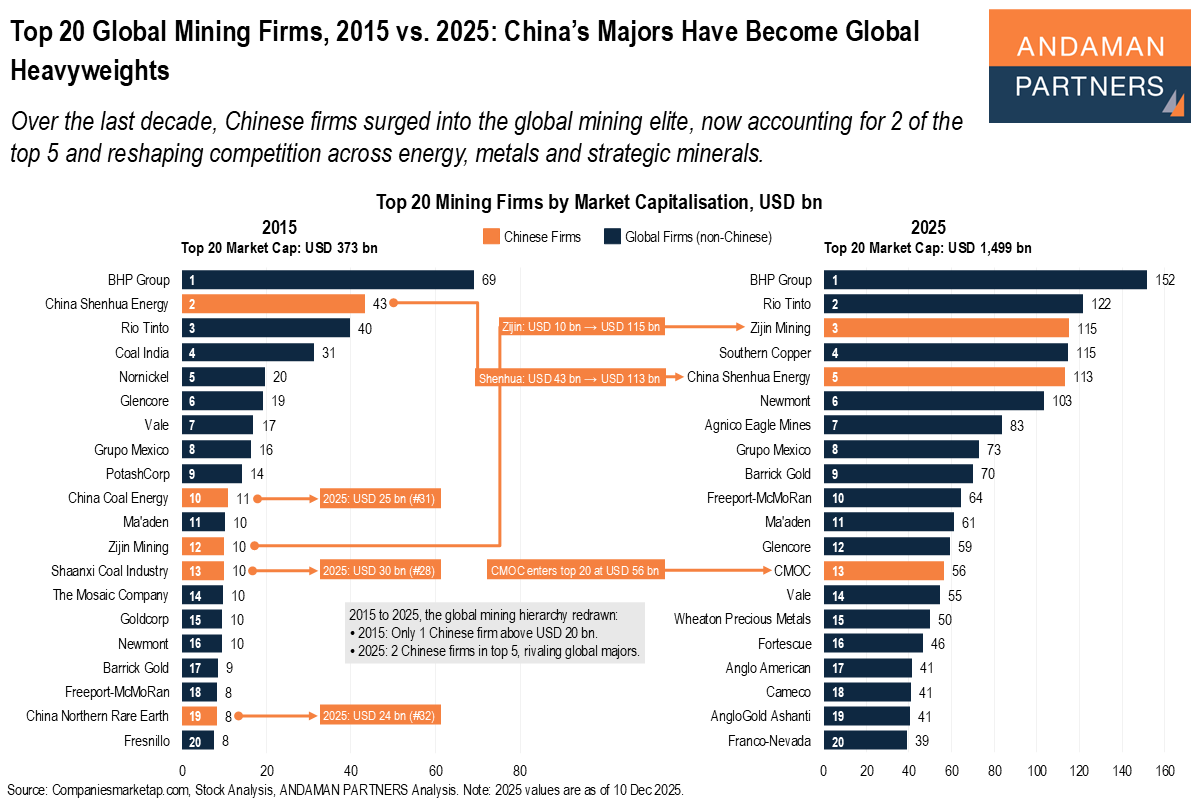

Over the last decade, Chinese firms surged into the global mining elite, now accounting for 2 of the top 5.

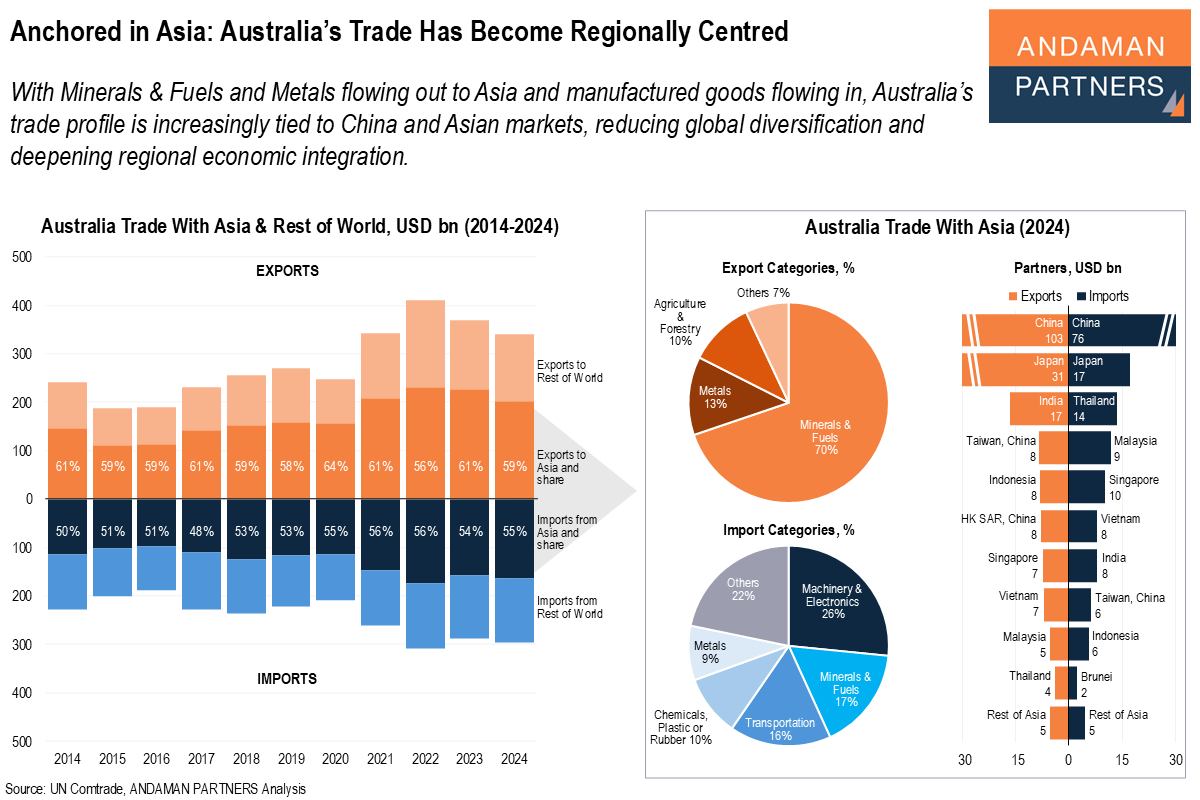

With Minerals & Fuels and Metals flowing out to Asia and manufactured goods flowing in, Australia’s trade profile is increasingly tied to China and Asian markets.

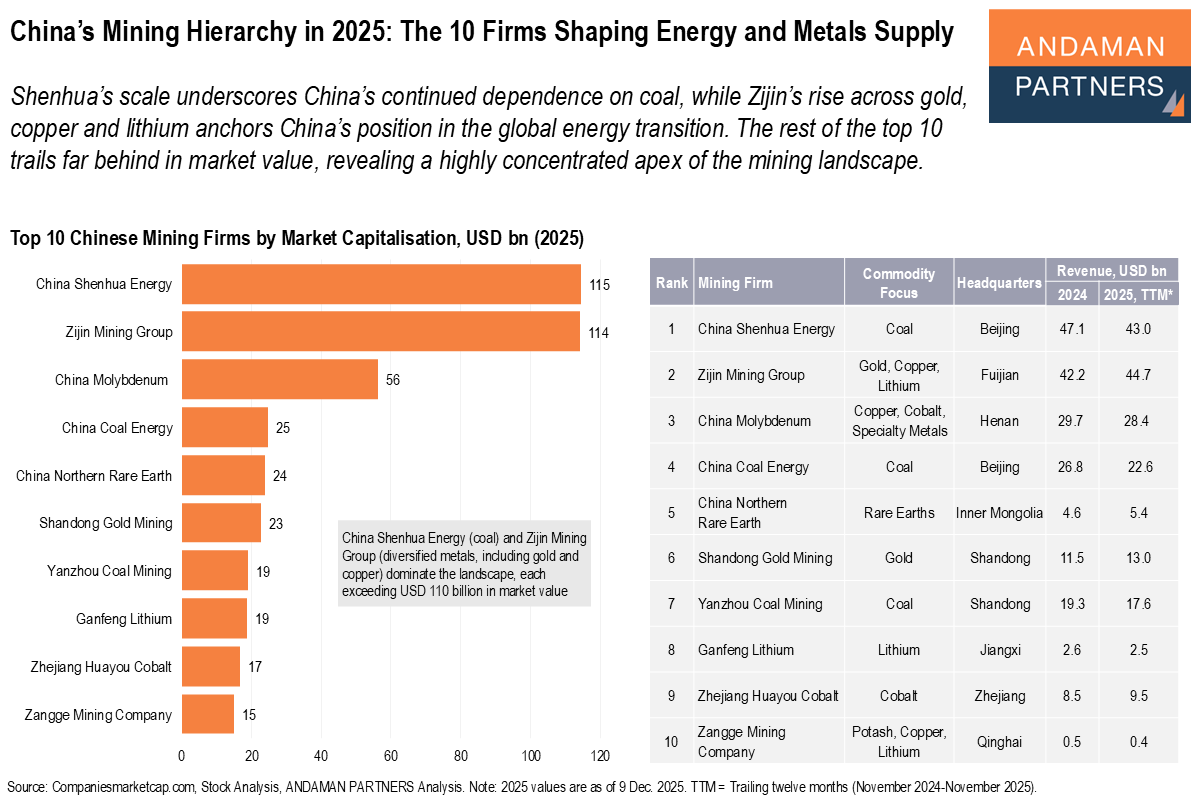

Shenhua’s scale underscores China’s continued dependence on coal, while Zijin’s rise anchors China’s position in the global energy transition.

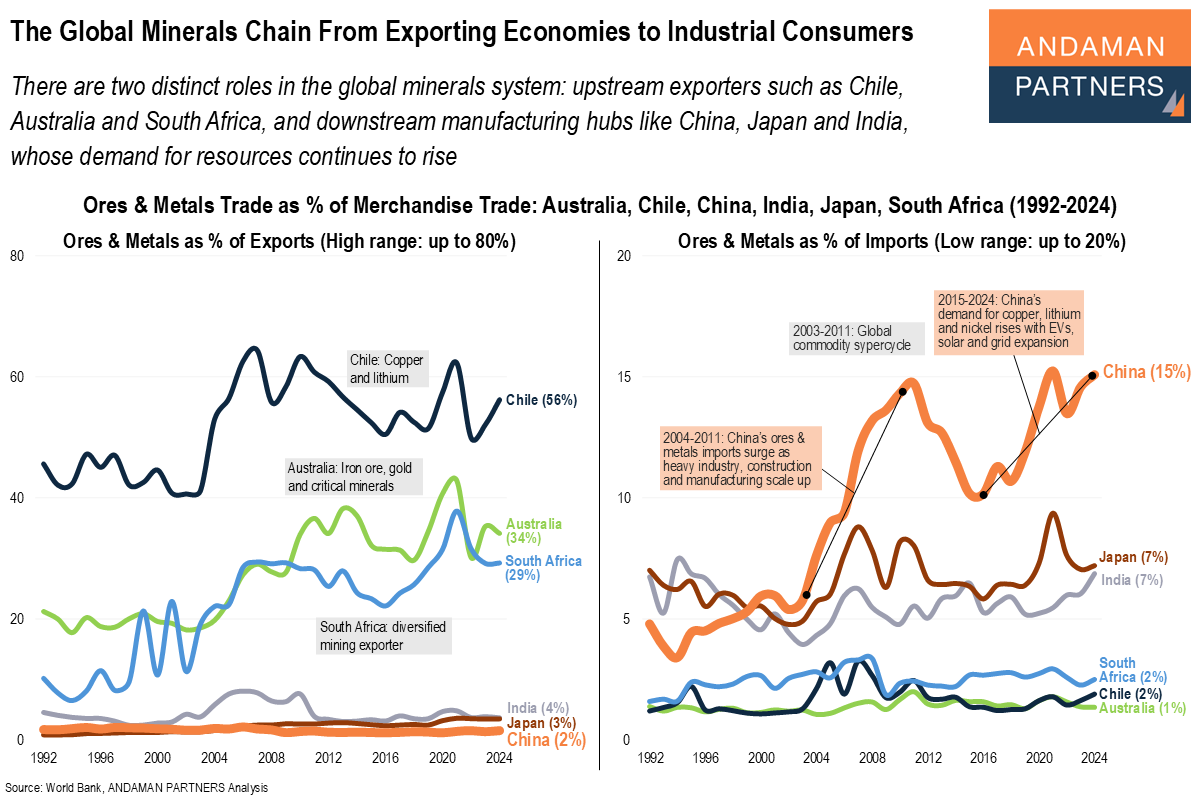

There are two distinct roles in the global minerals system: upstream exporters and downstream manufacturing hubs, whose demand for resources continues to rise.

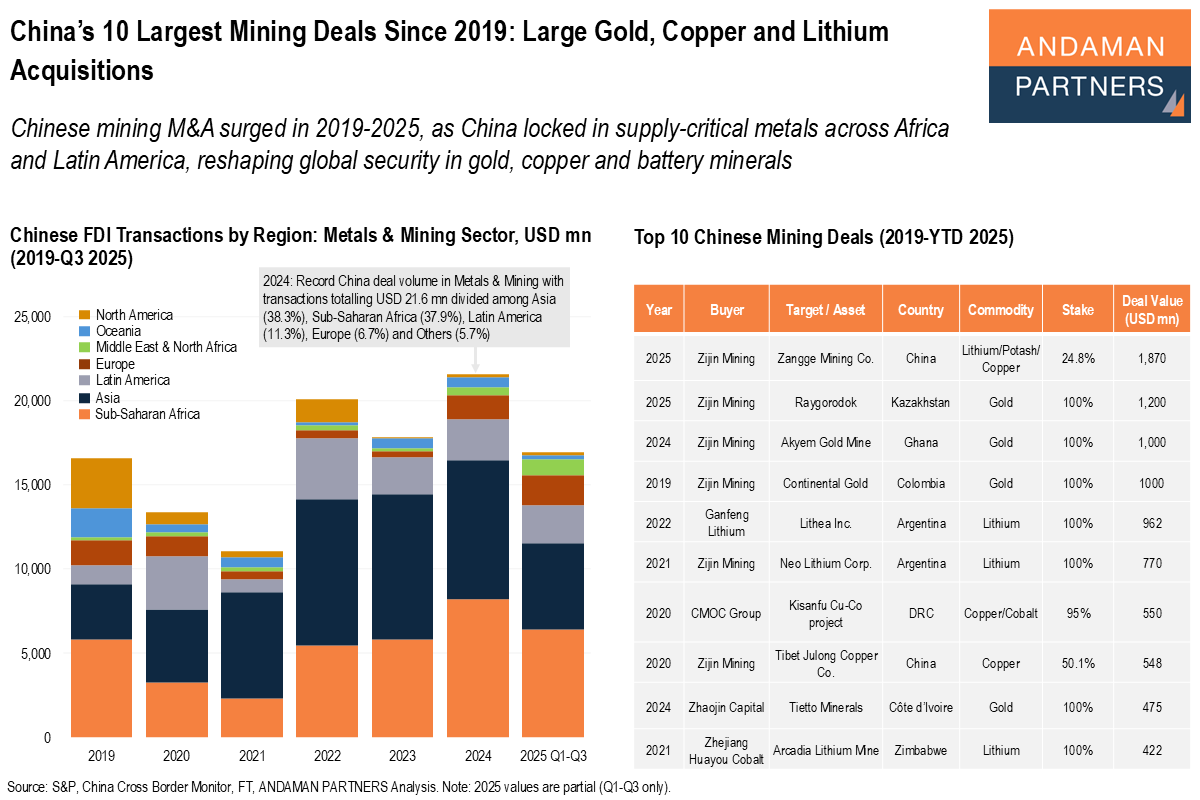

Chinese mining M&A surged in 2019-2025, as China locked in supply-critical metals across Africa and Latin America.

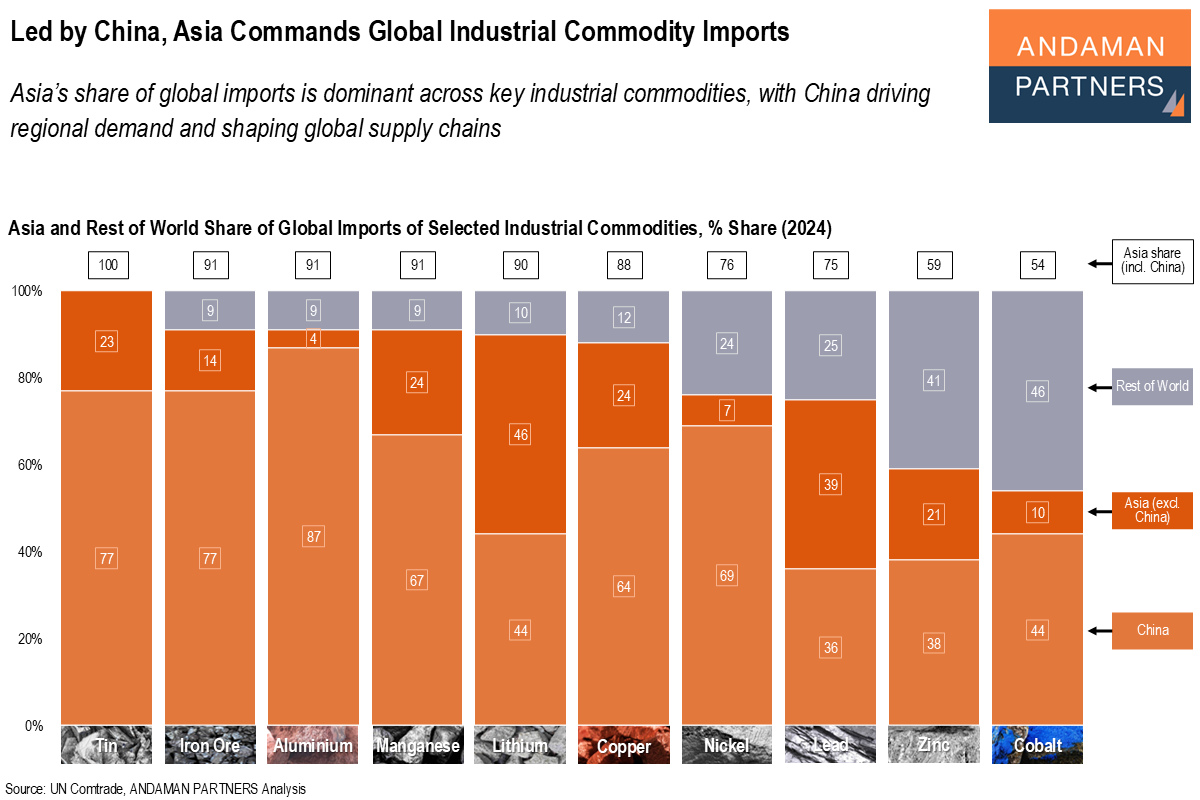

Asia’s share of global imports is dominant across key industrial commodities, with China driving regional demand and shaping global supply chains.