Asia’s Energy Import Dependence Is Creating Distinct Investment and Growth Profiles

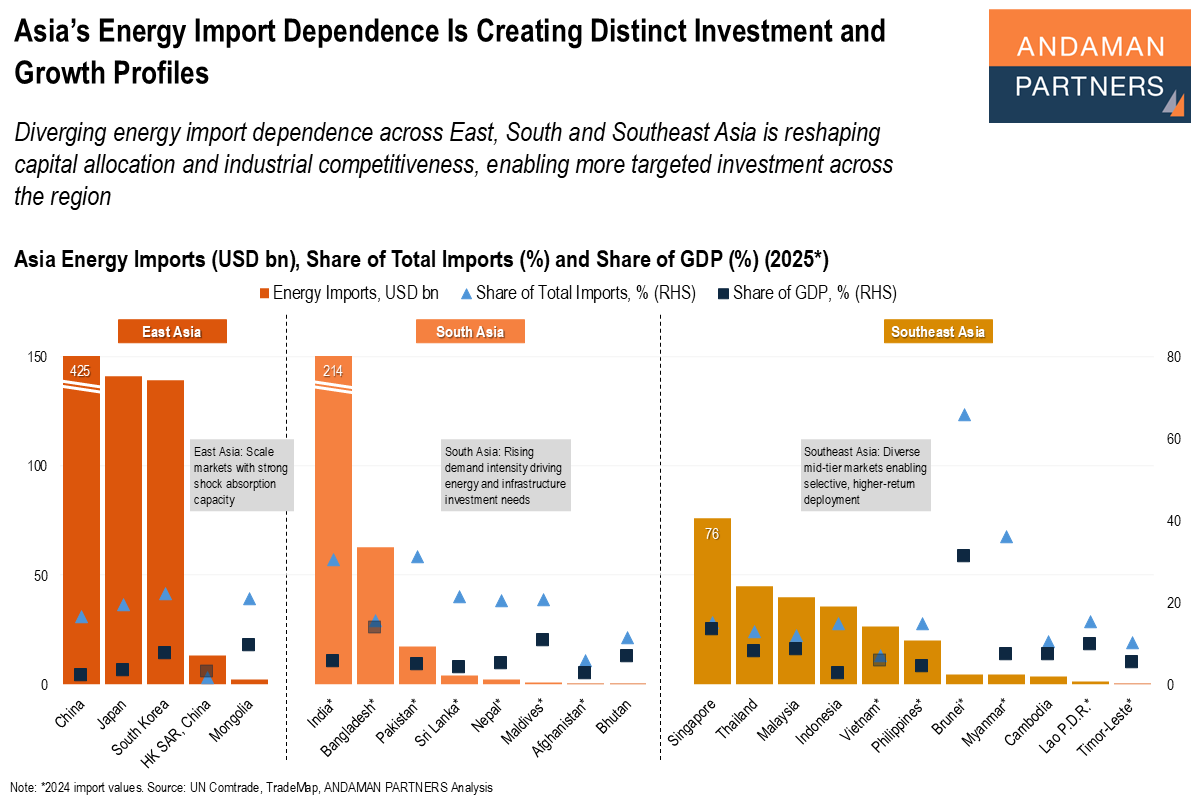

Diverging energy import dependence across Asia is enabling more targeted investment across the region.

Diverging energy import dependence across Asia is enabling more targeted investment across the region.

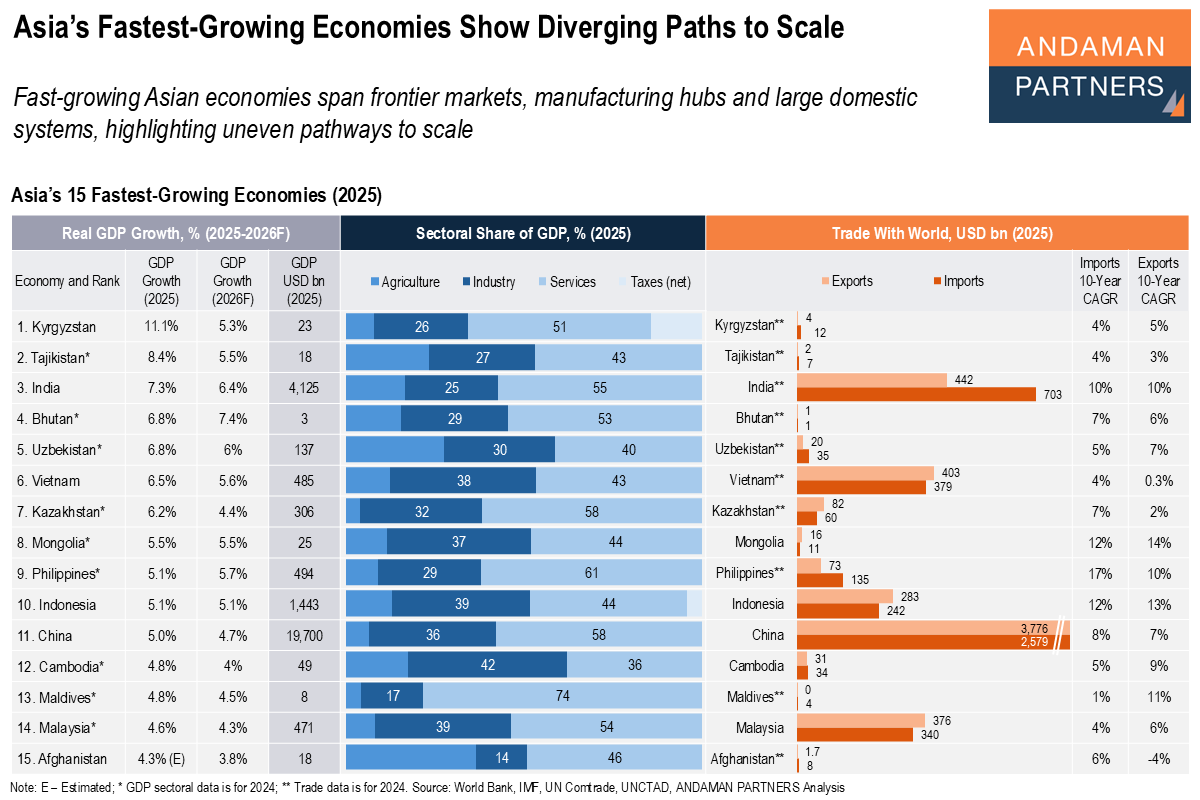

Fast-growing Asian economies span frontier markets, manufacturing hubs and large domestic systems, highlighting uneven pathways to scale.

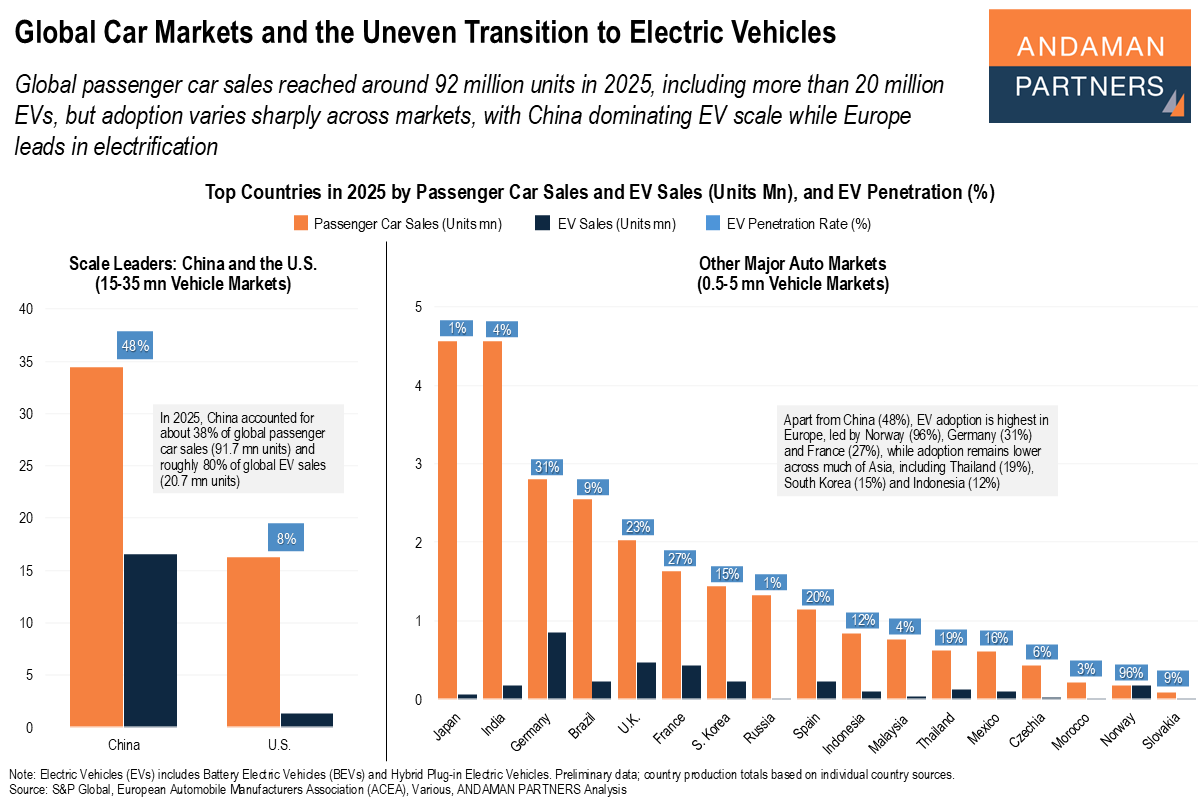

Global passenger car sales reached 92 million units in 2025, including more than 20 million EVs, but adoption varies widely across markets.

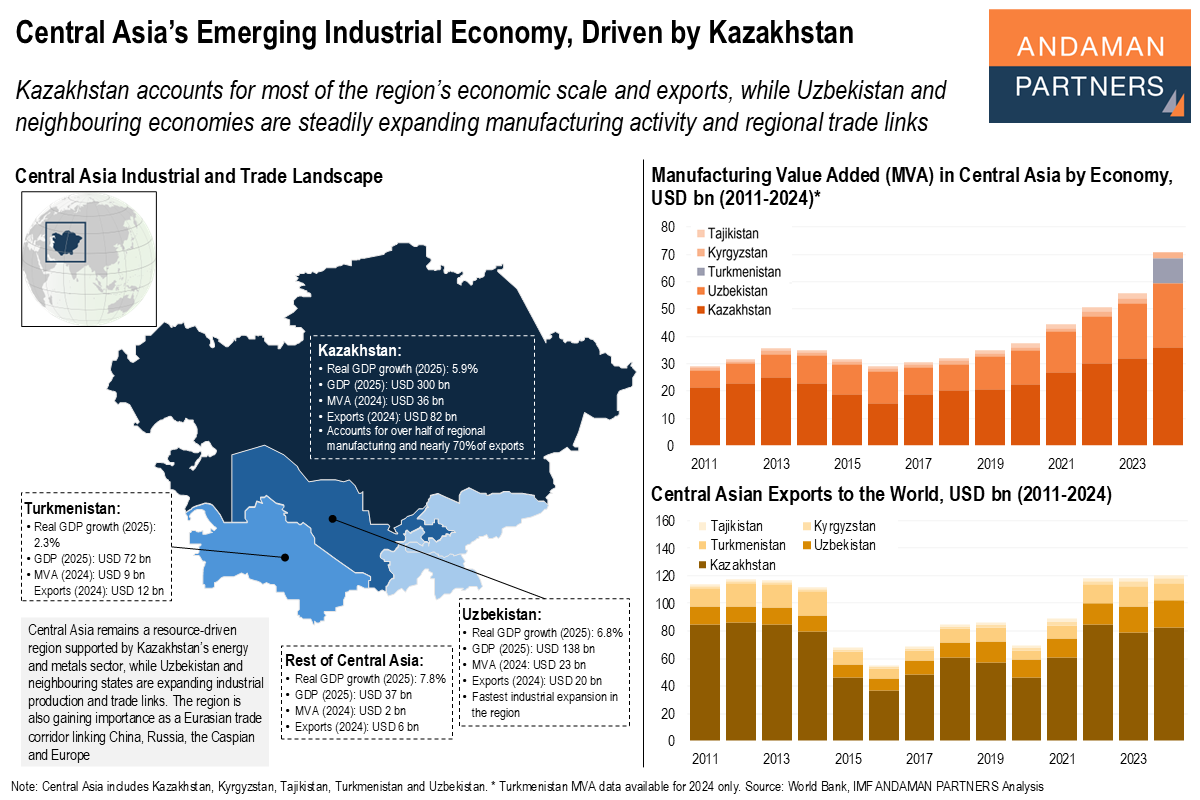

Kazakhstan accounts for the region’s economic scale, while Uzbekistan and neighbouring economies are expanding manufacturing and trade.

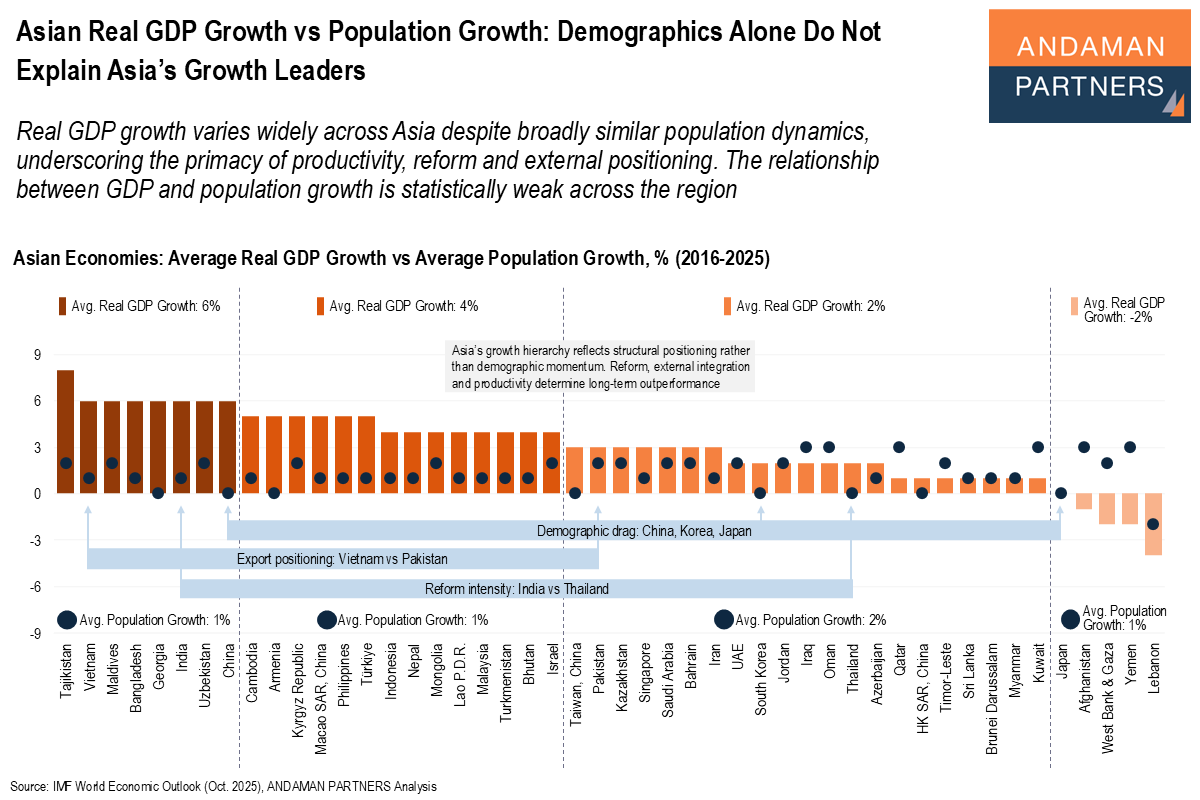

Real GDP growth varies widely across Asia despite broadly similar population dynamics.

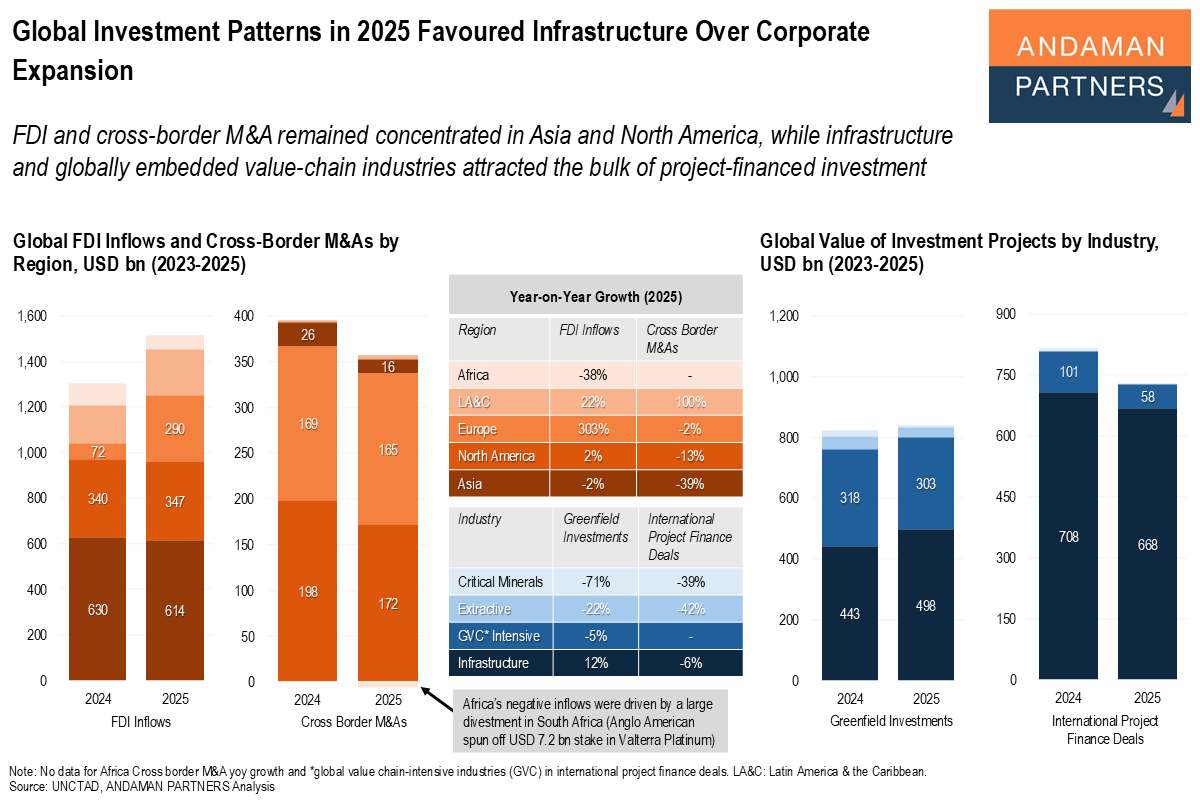

FDI and M&A remained concentrated in Asia and North America, while infrastructure attracted the bulk of project-financed investment.

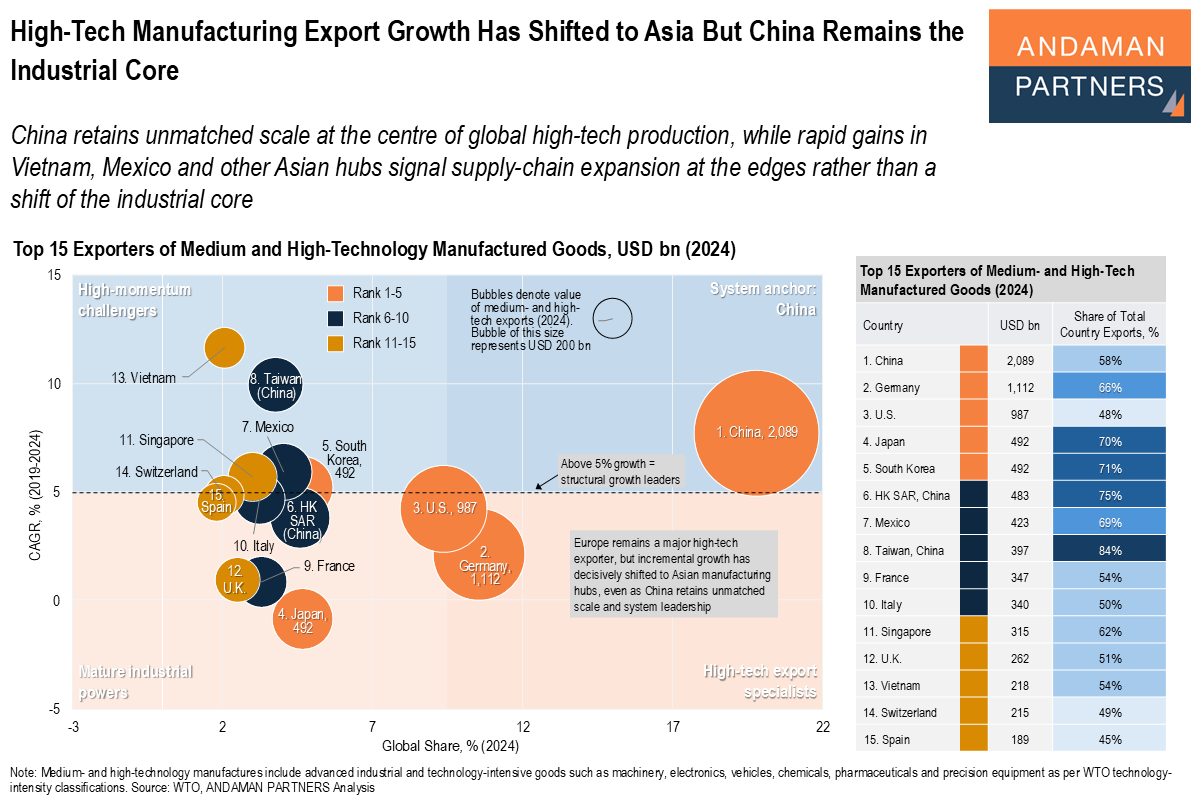

China retains unmatched scale at the centre of global high-tech production, while rapid gains in Vietnam, Mexico and other Asian hubs.

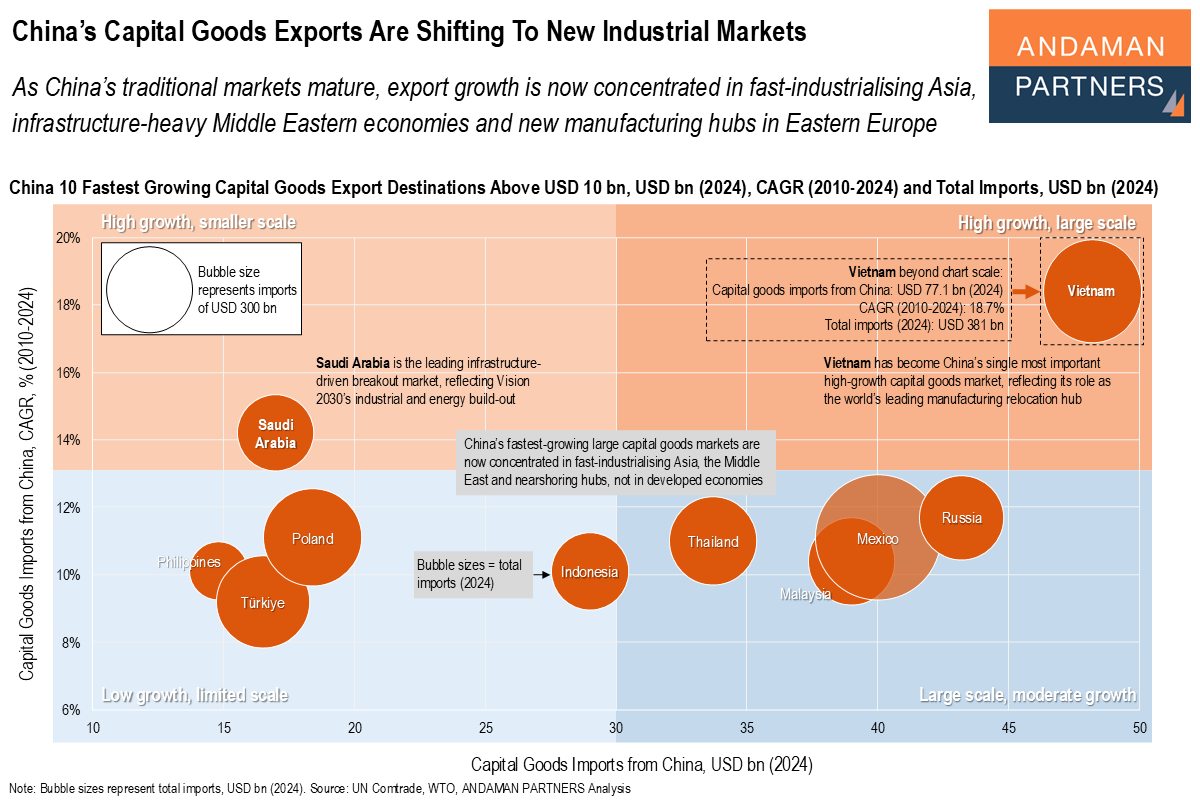

Export growth is now concentrated in fast-industrialising Asia, infrastructure-heavy Middle Eastern economies and new manufacturing hubs in Eastern Europe.

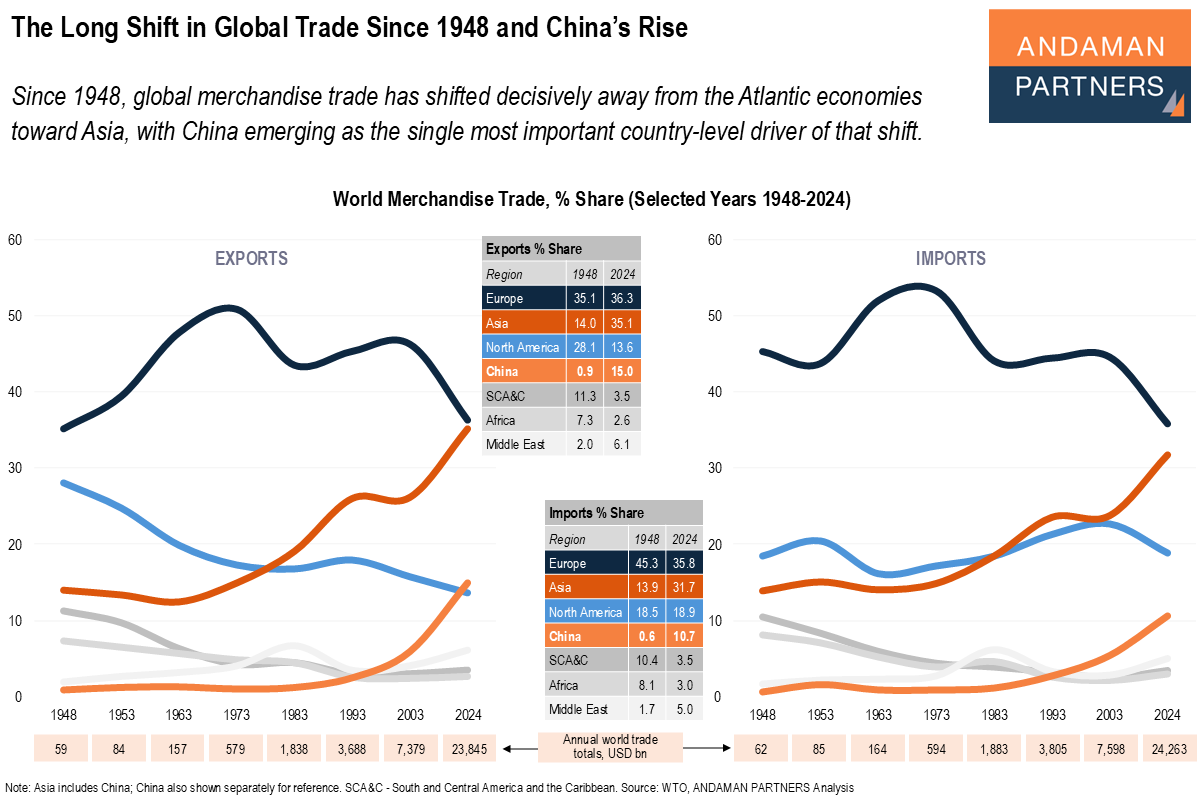

Since 1948, global merchandise trade has shifted decisively away from the Atlantic economies toward Asia.

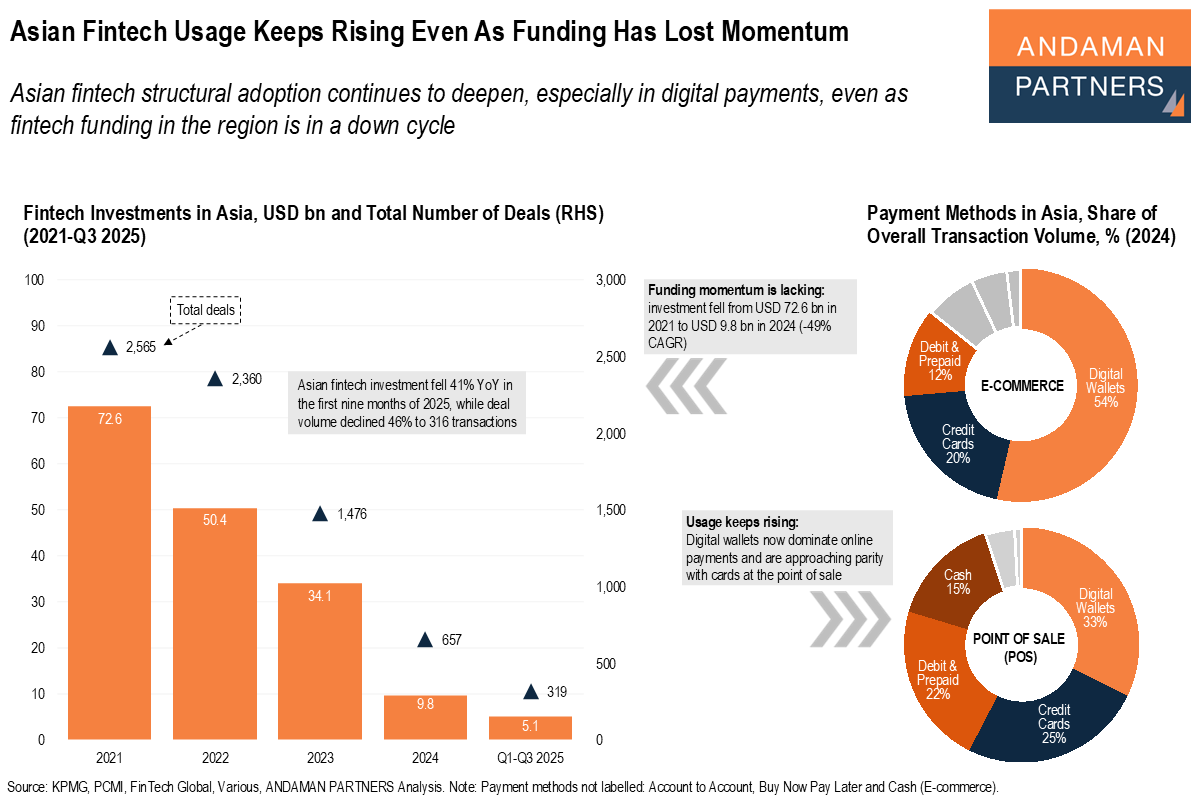

Asian fintech structural adoption continues to deepen, especially in digital payments, even as fintech funding in the region is in a down cycle.