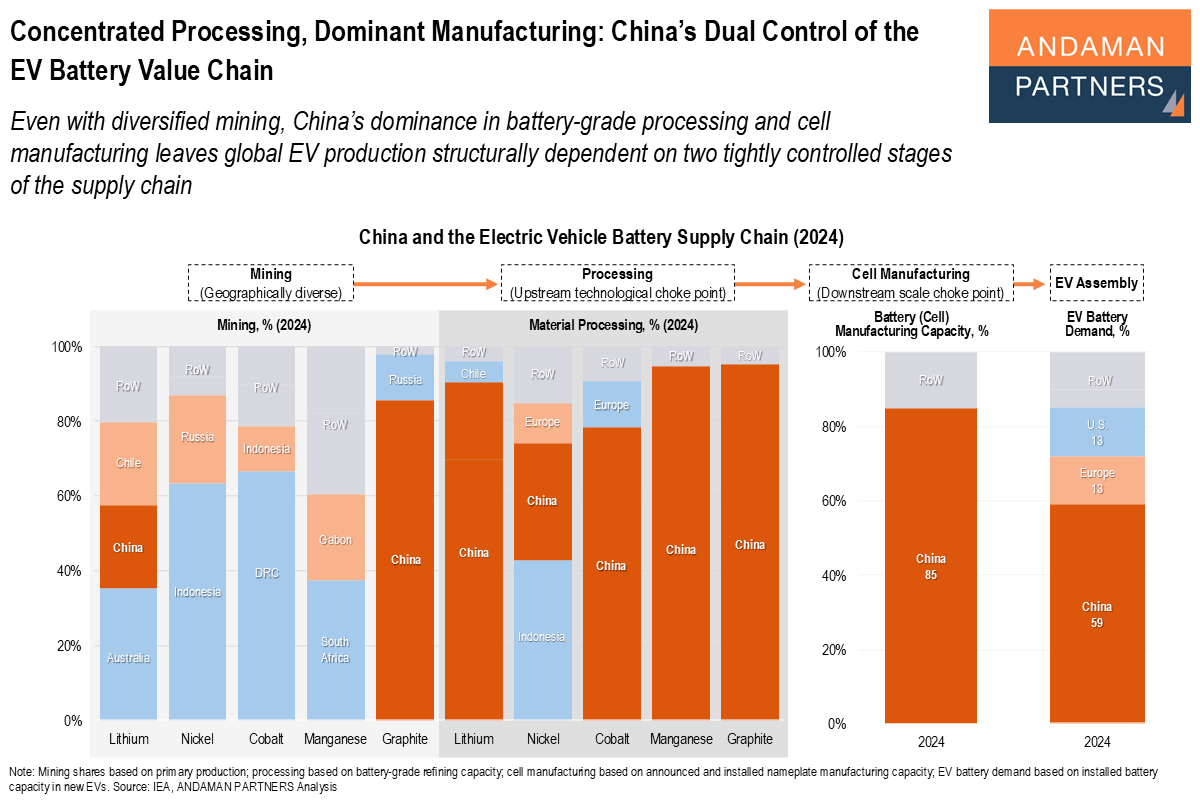

Concentrated Processing, Dominant Manufacturing: China’s Dual Control of the EV Battery Value Chain

China’s dominance in battery-grade processing and cell manufacturing leaves global EV production dependent on two stages of the supply chain.

China’s dominance in battery-grade processing and cell manufacturing leaves global EV production dependent on two stages of the supply chain.

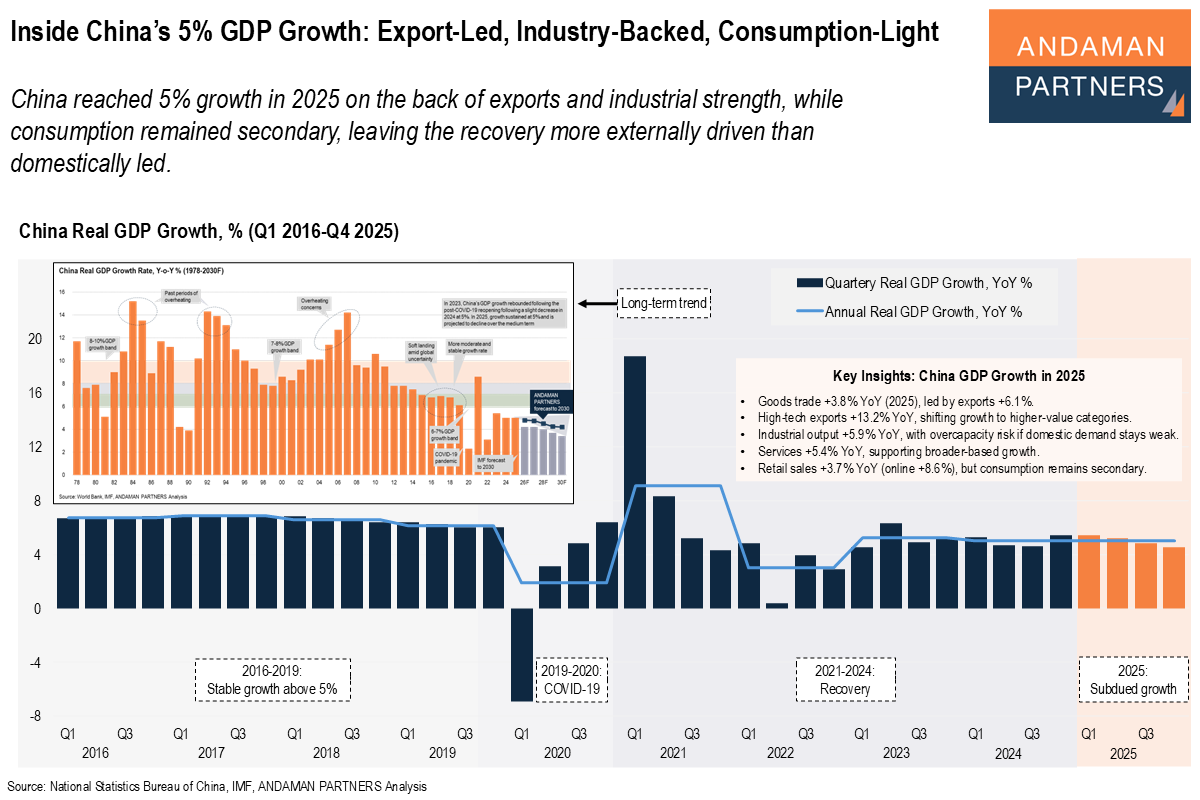

China reached 5% growth in 2025 on the back of exports and industrial strength, while consumption remained secondary.

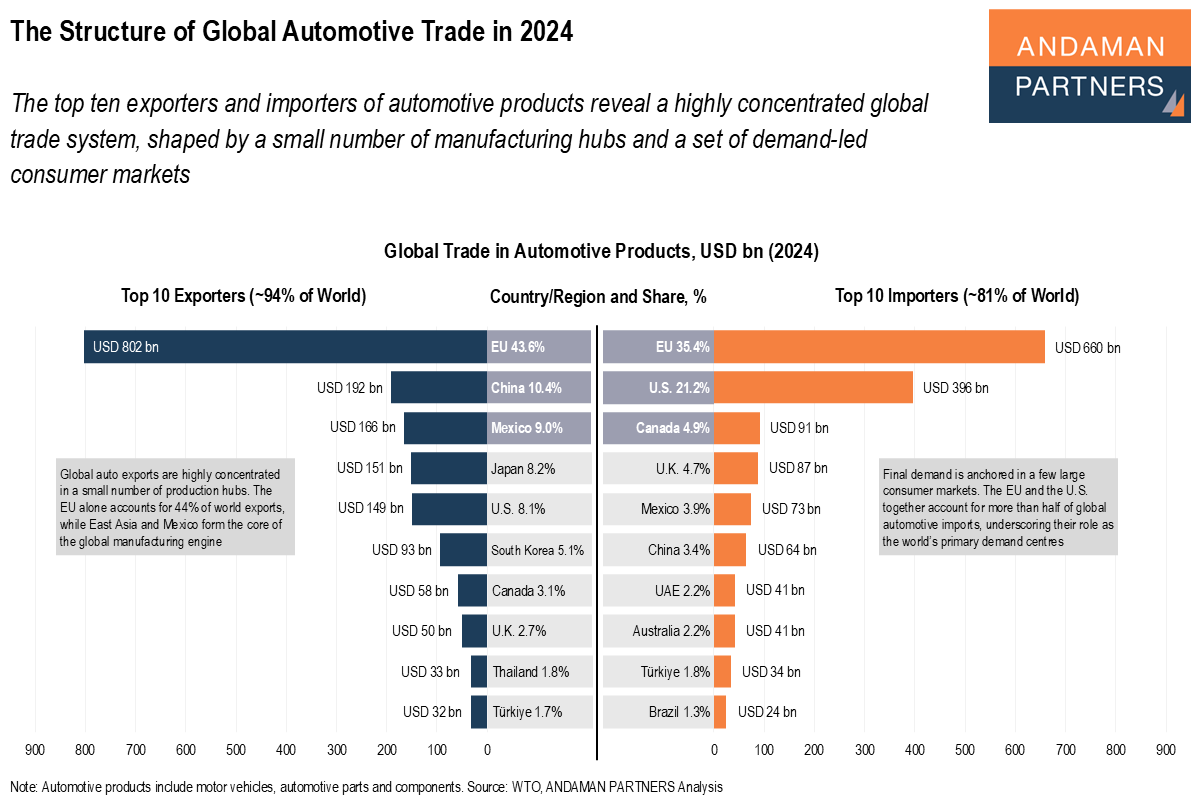

The top ten exporters and importers of automotive products reveal a highly concentrated global trade system.

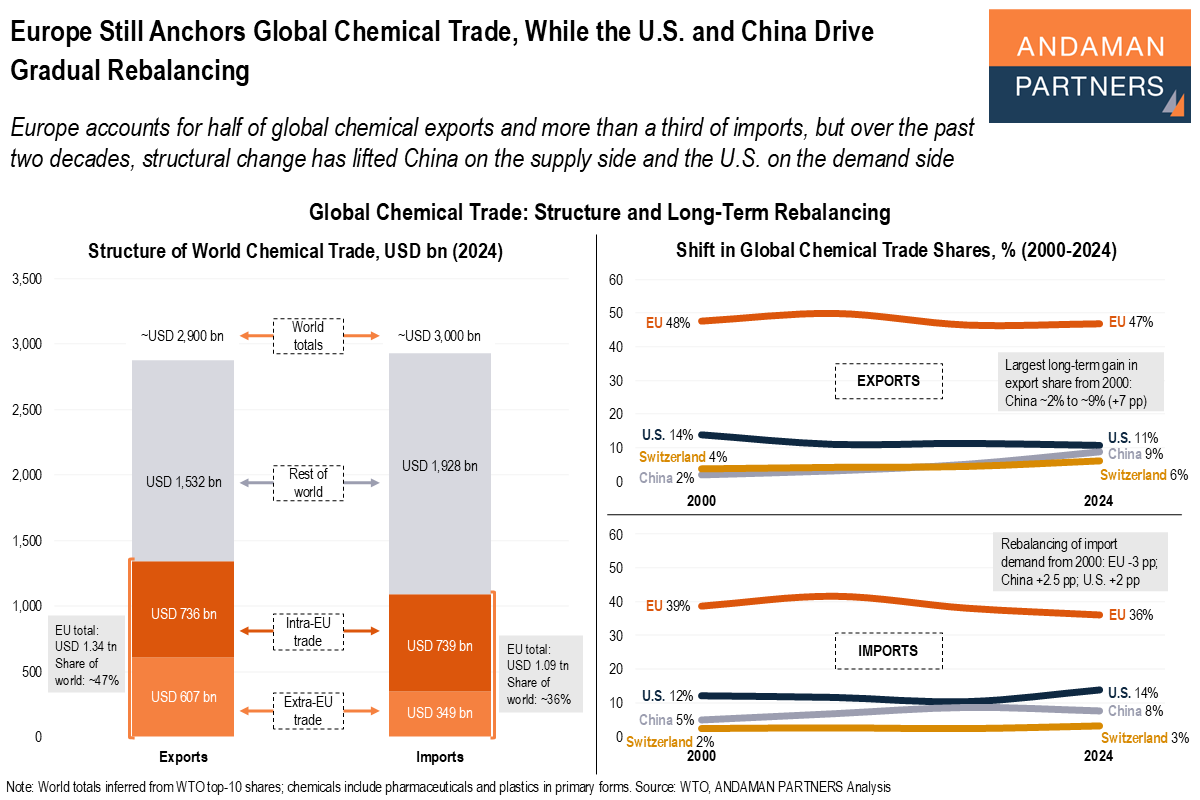

Europe accounts for half of global chemical exports and more than a third of imports, but over the past two decades, structural change has lifted China and the U.S.

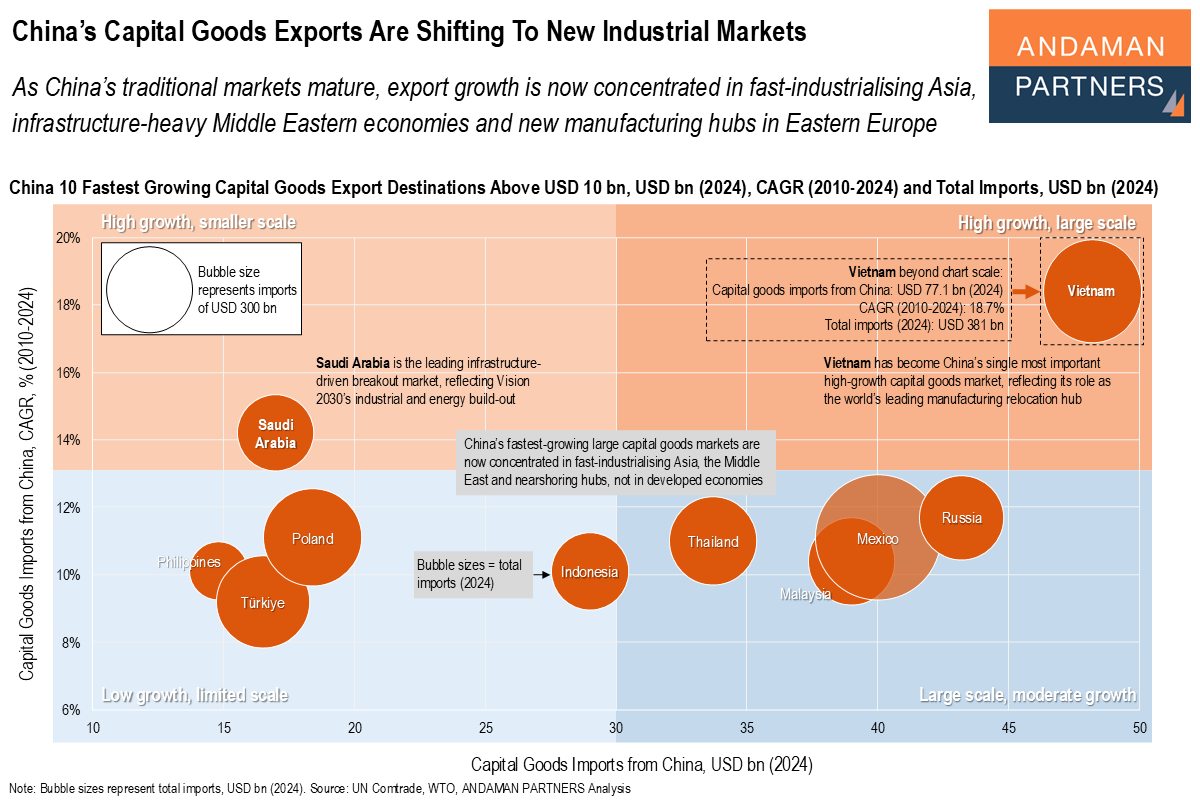

Export growth is now concentrated in fast-industrialising Asia, infrastructure-heavy Middle Eastern economies and new manufacturing hubs in Eastern Europe.

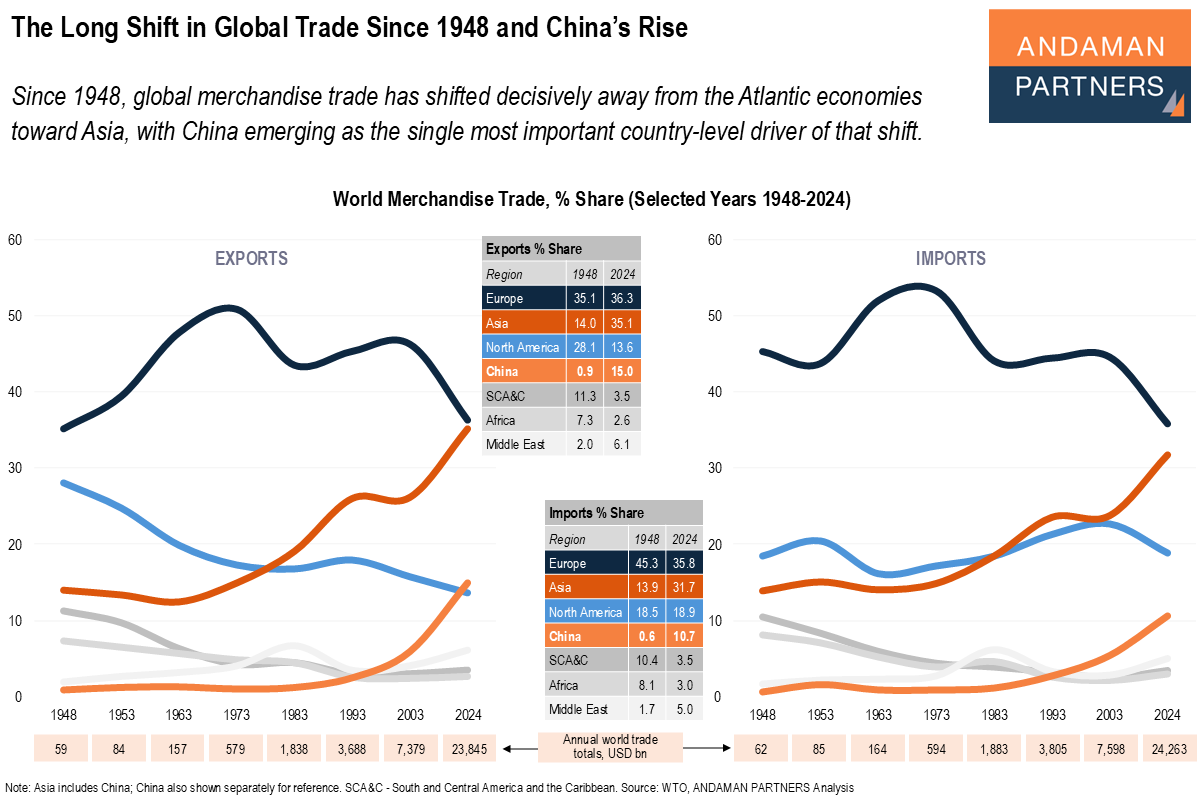

Since 1948, global merchandise trade has shifted decisively away from the Atlantic economies toward Asia.

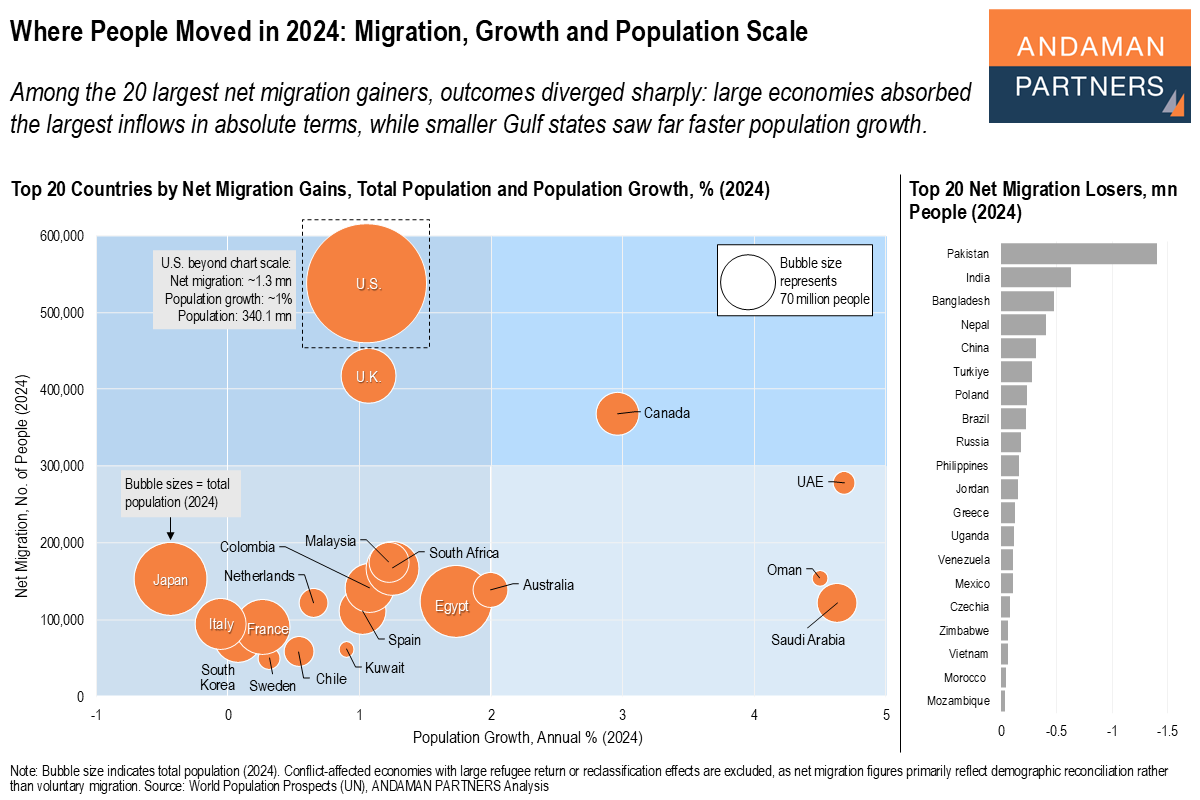

Among the 20 largest net migration gainers, outcomes diverged sharply: large economies absorbed the largest inflows; smaller Gulf states saw far faster growth.

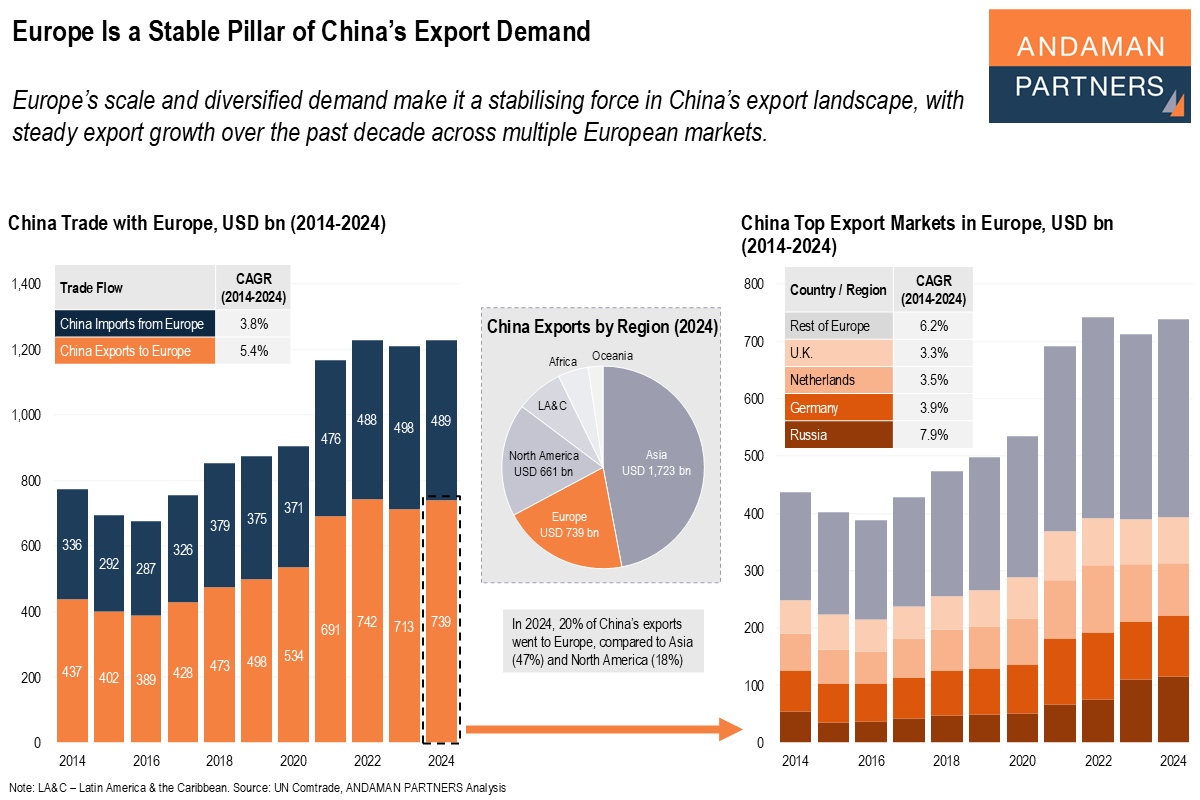

Europe’s scale and diversified demand make it a stabilising force in China’s export landscape, with steady export growth over the past decade.

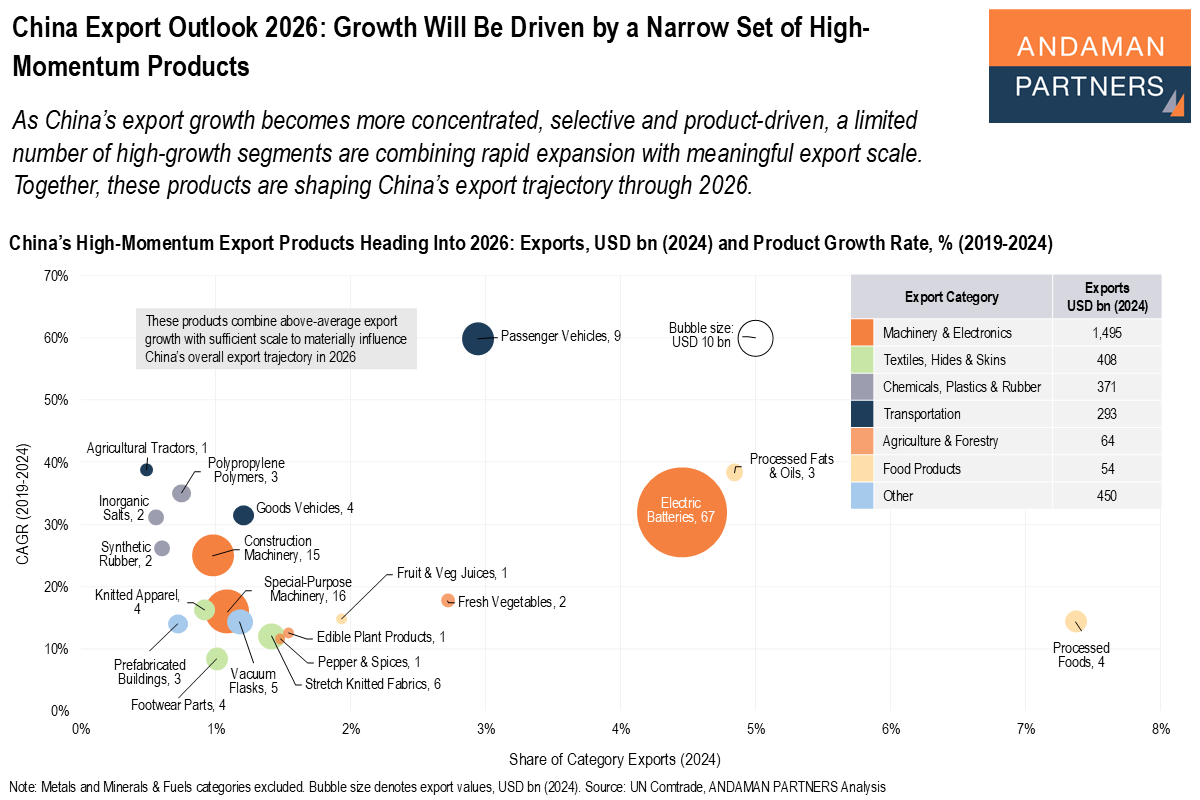

As China’s export growth becomes more concentrated, a limited number of high-growth segments are combining rapid expansion with meaningful export scale.

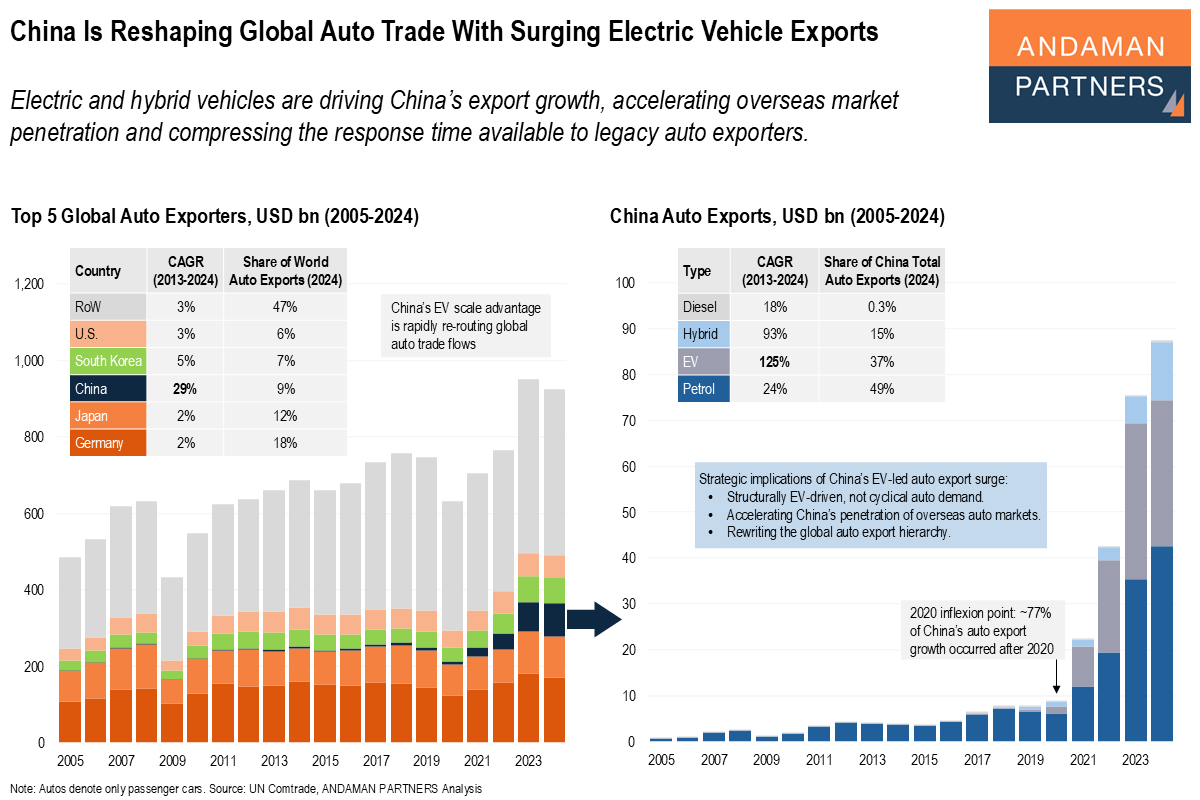

Electric and hybrid vehicles are driving China’s export growth, accelerating overseas market penetration and compressing the response time available to legacy auto exporters.