Africa’s Export Growth Accelerates as China’s Role Continues to Expand

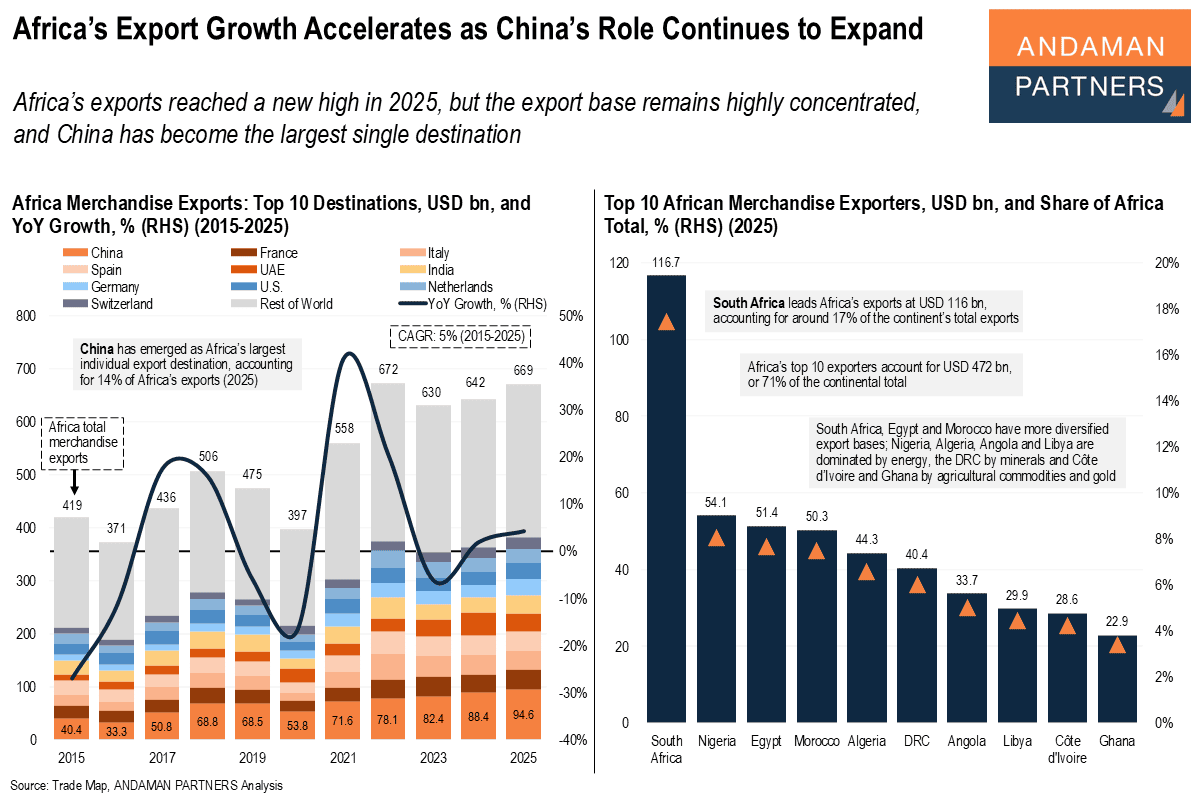

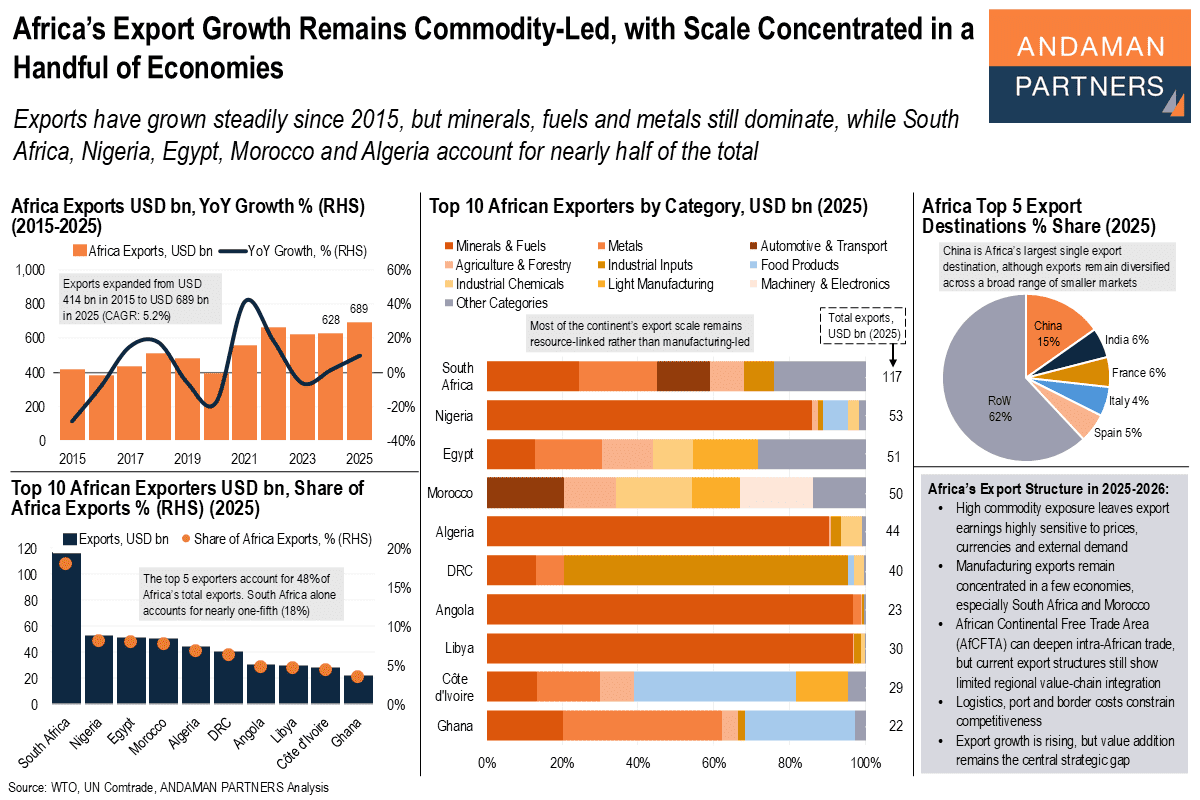

Africa’s exports reached a new high in 2025, but the export base remains highly concentrated, and China has become the largest single destination

Africa’s exports reached a new high in 2025, but the export base remains highly concentrated, and China has become the largest single destination

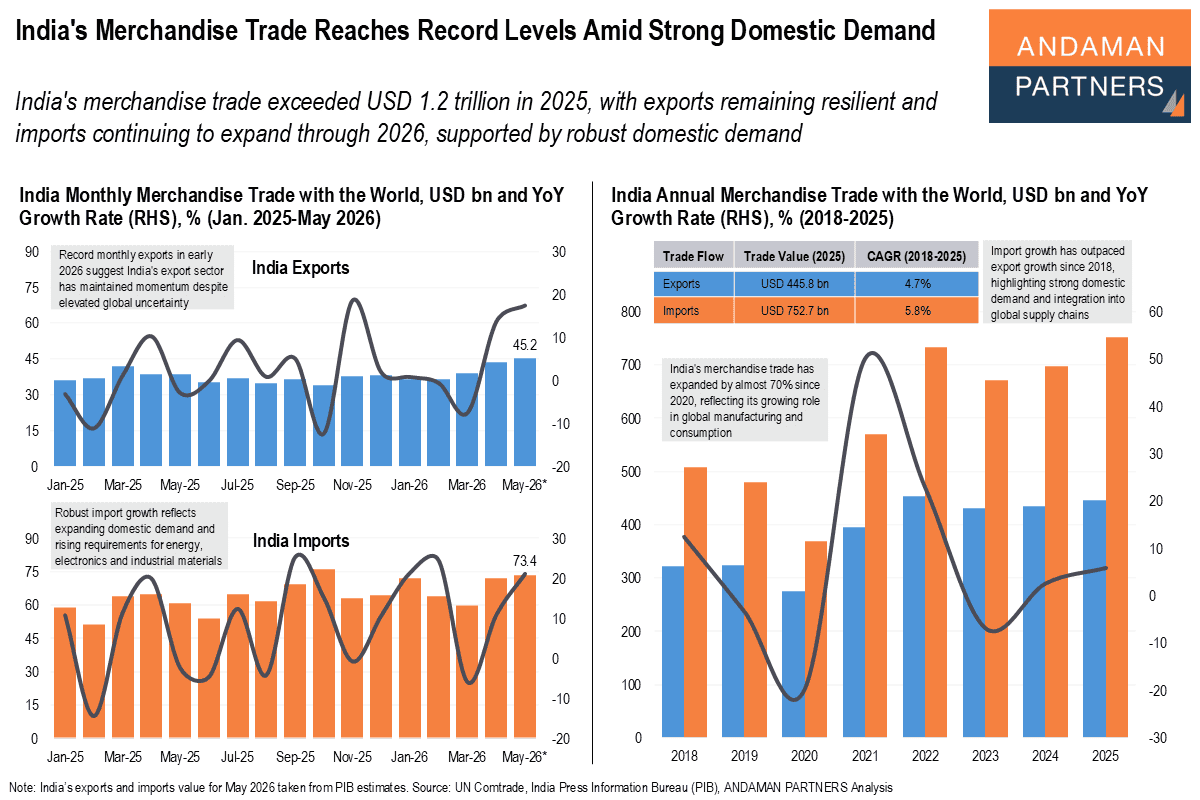

India's merchandise trade exceeded USD 1.2 trillion in 2025, with exports remaining resilient and imports continuing to expand through 2026

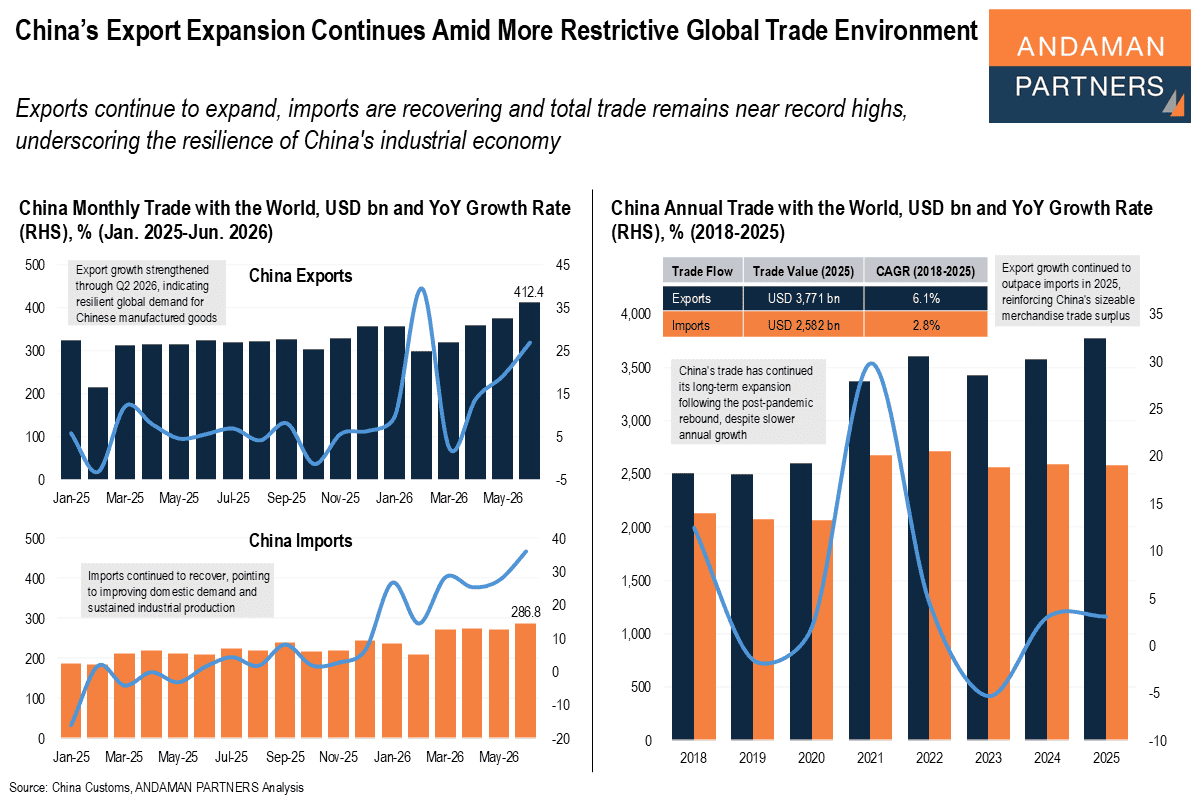

Exports continue to expand, imports are recovering and total trade remains near record highs

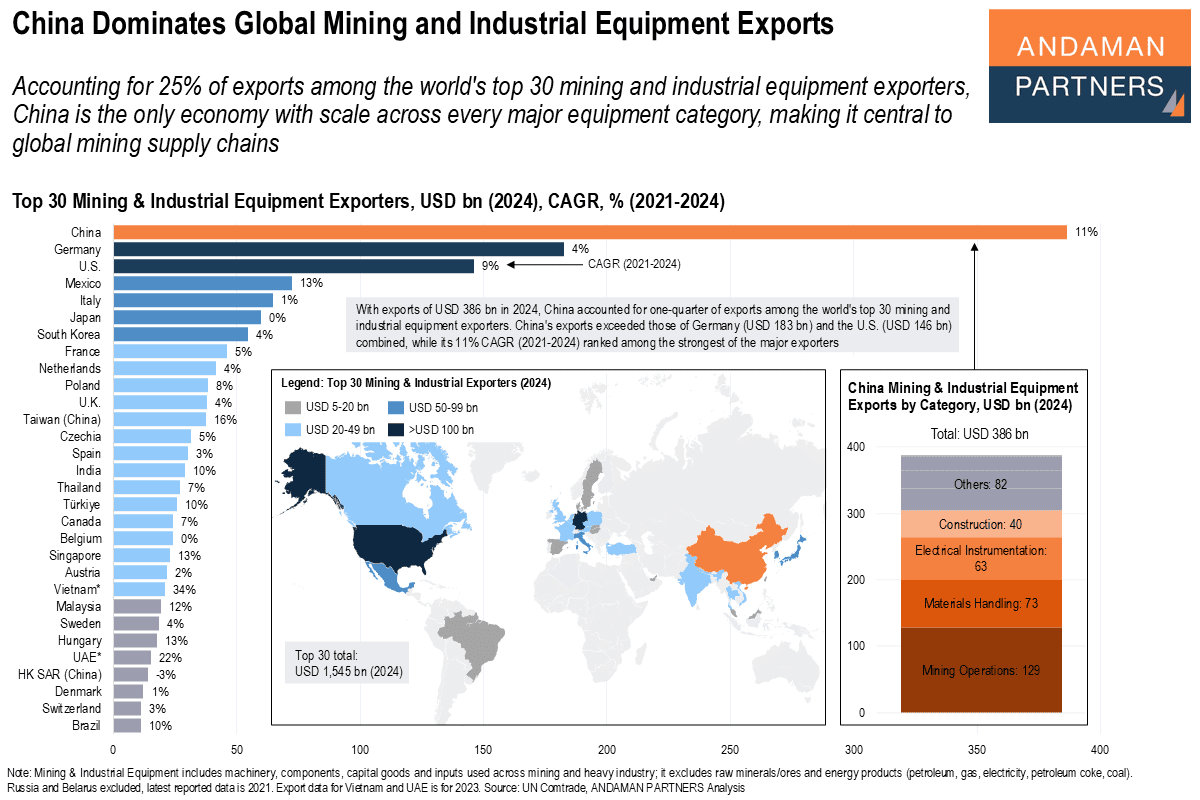

China is the only economy with scale across every major equipment category, making it central to global mining supply chains

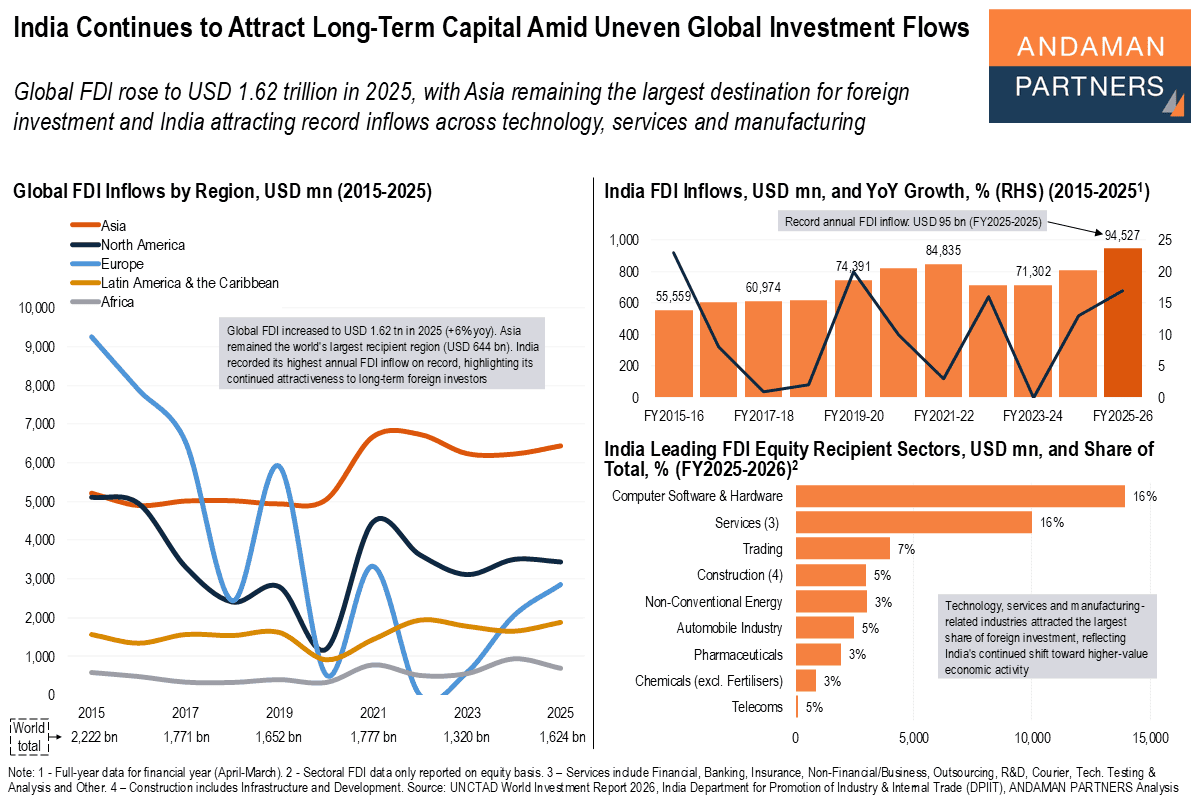

Global FDI rose to USD 1.62 trillion in 2025, with Asia remaining the largest destination and India attracting record inflows

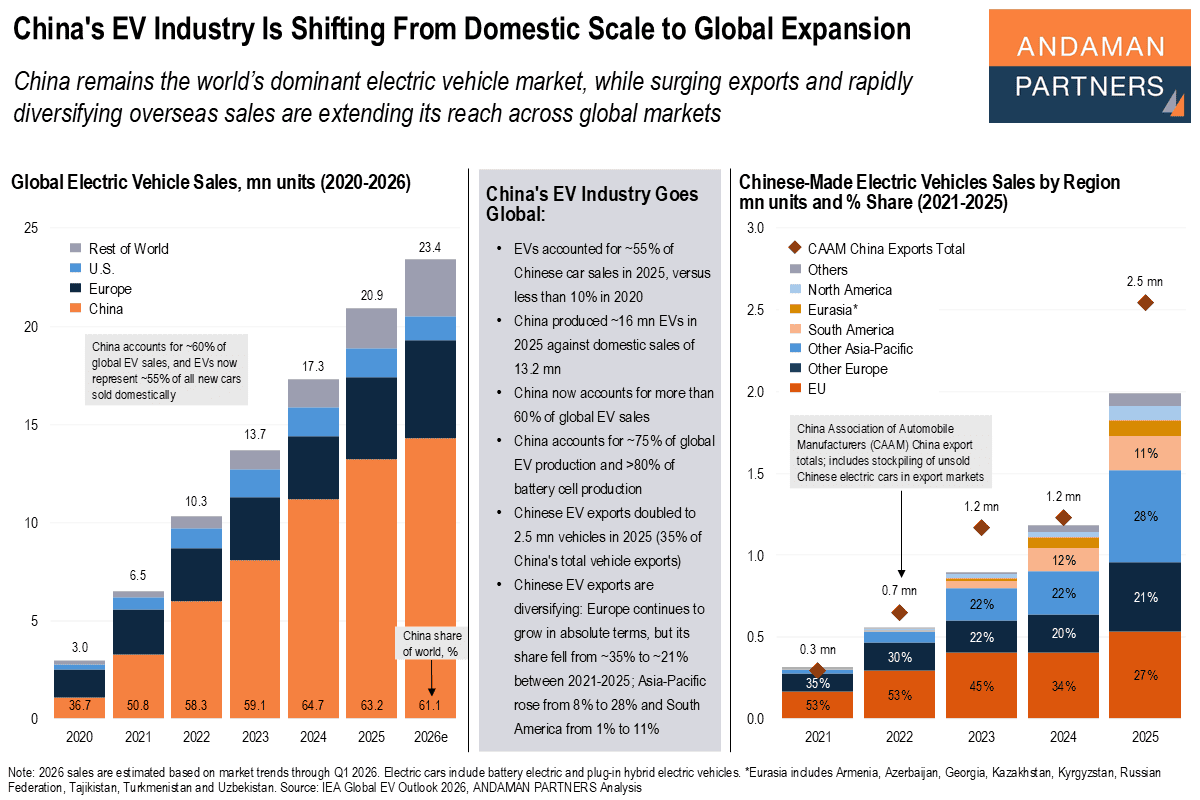

China is the world’s dominant EV market, and surging exports and diversifying overseas sales are extending its reach across global markets

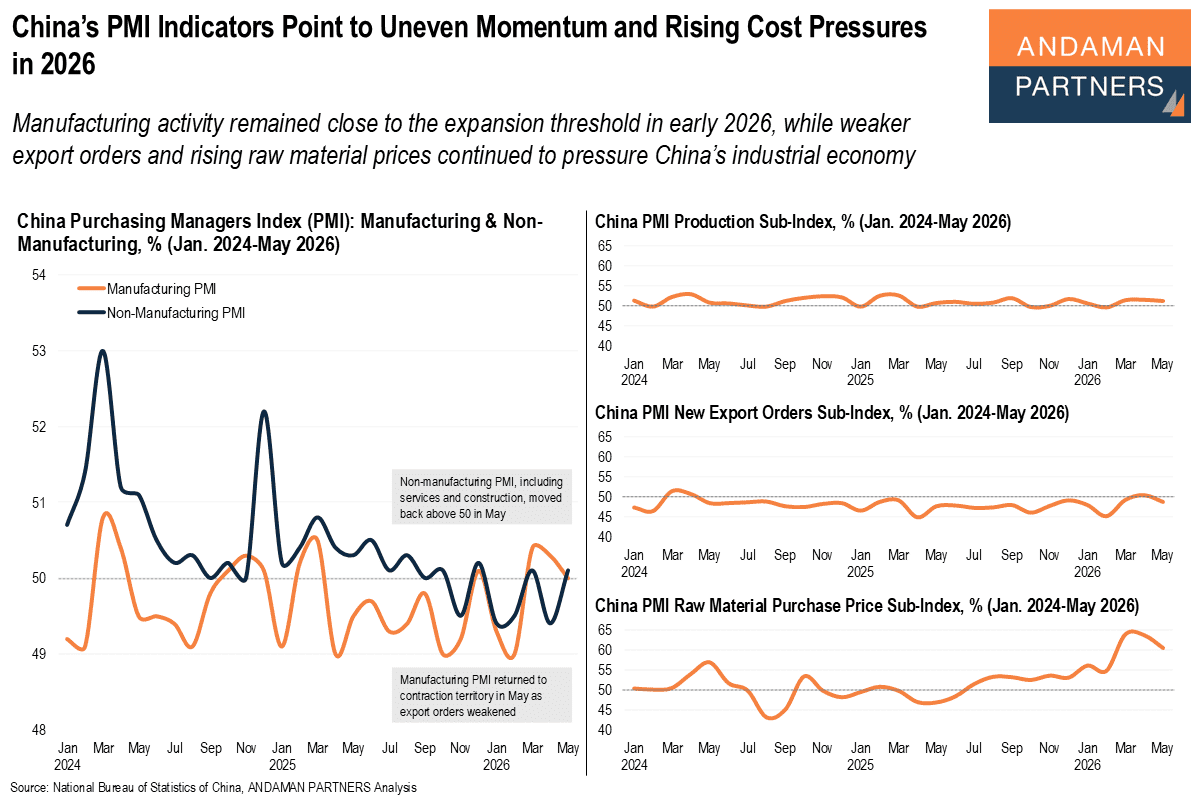

Manufacturing activity remained close to expansion in early 2026, while weaker export orders and raw material prices pressure the economy

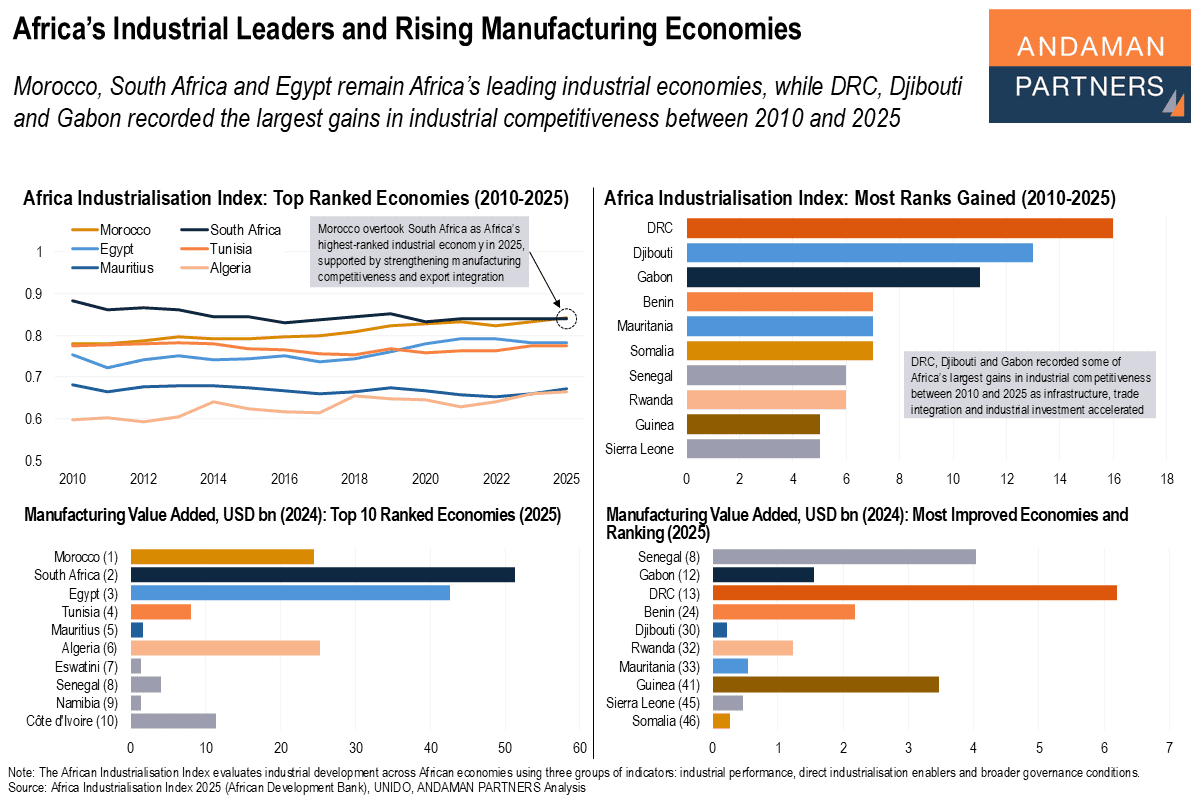

Morocco, South Africa and Egypt remain Africa’s leading industrial economies; DRC, Djibouti and Gabon recorded the largest gains in competitiveness

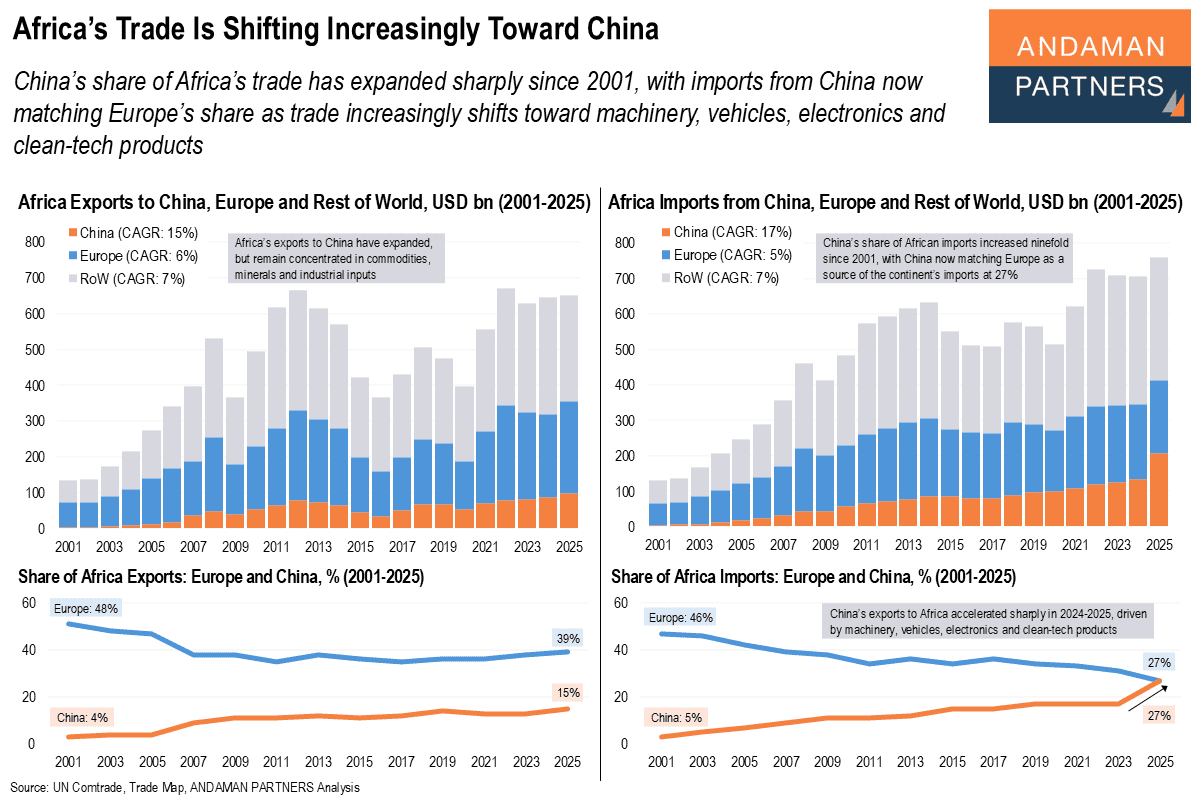

China’s share of Africa’s trade has expanded sharply since 2001, with imports from China now matching Europe’s share

Exports have grown steadily since 2015, but minerals, fuels and metals still dominate, while five countries account for half of the total