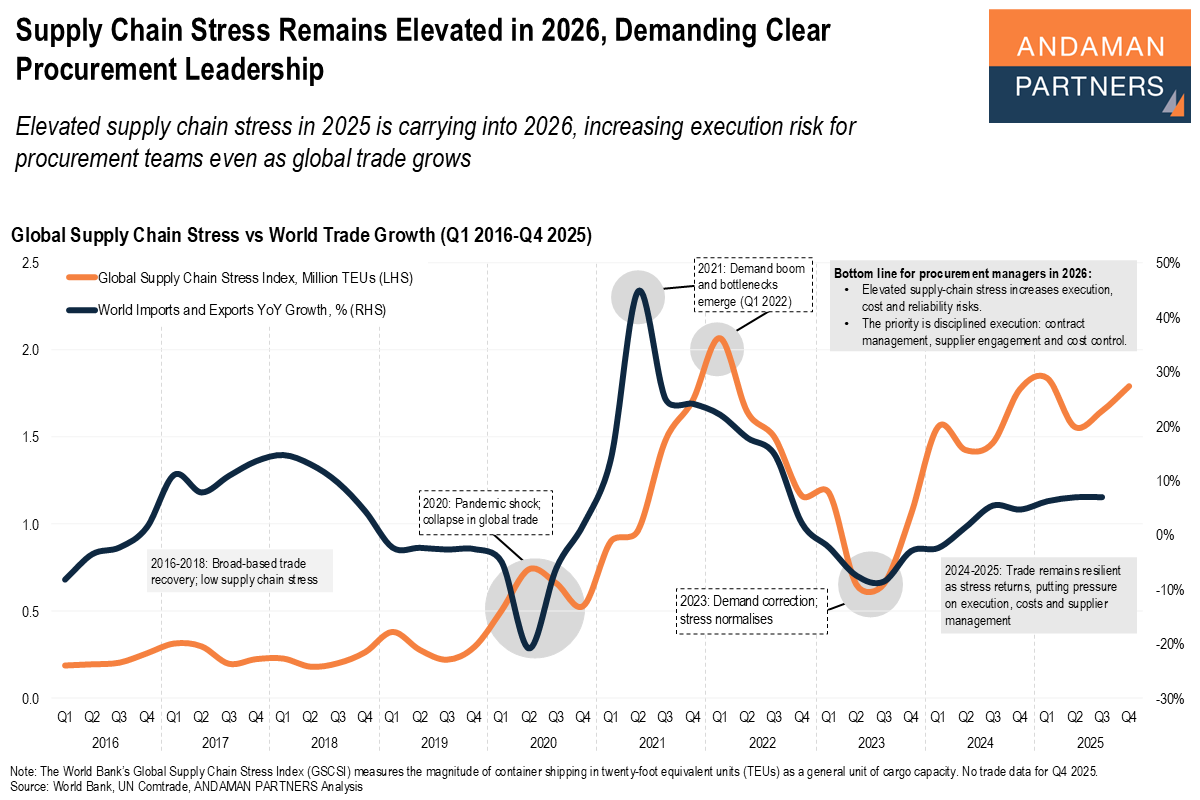

Supply Chain Stress Remains Elevated in 2026, Demanding Clear Procurement Leadership

Elevated supply chain stress in 2025 is carrying into 2026, increasing execution risk for procurement teams even as global trade grows.

Elevated supply chain stress in 2025 is carrying into 2026, increasing execution risk for procurement teams even as global trade grows.

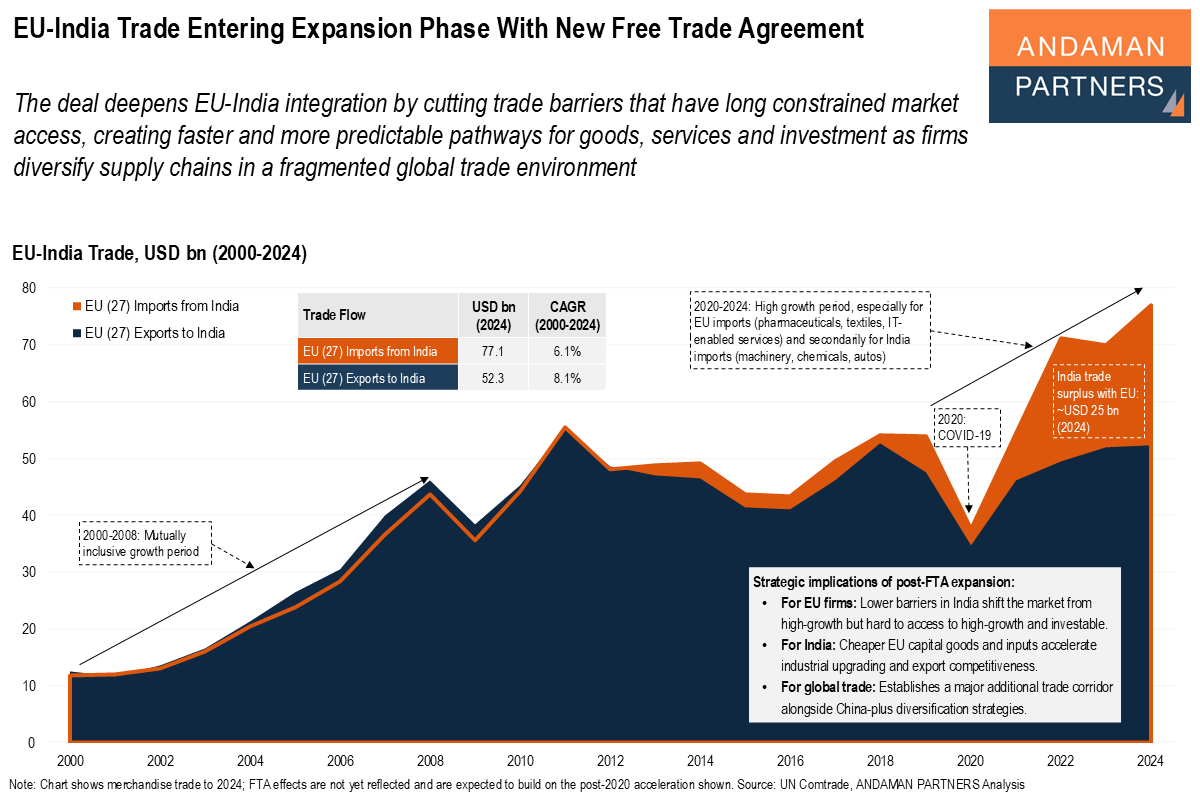

The deal deepens EU-India integration by cutting trade barriers that have long constrained market access.

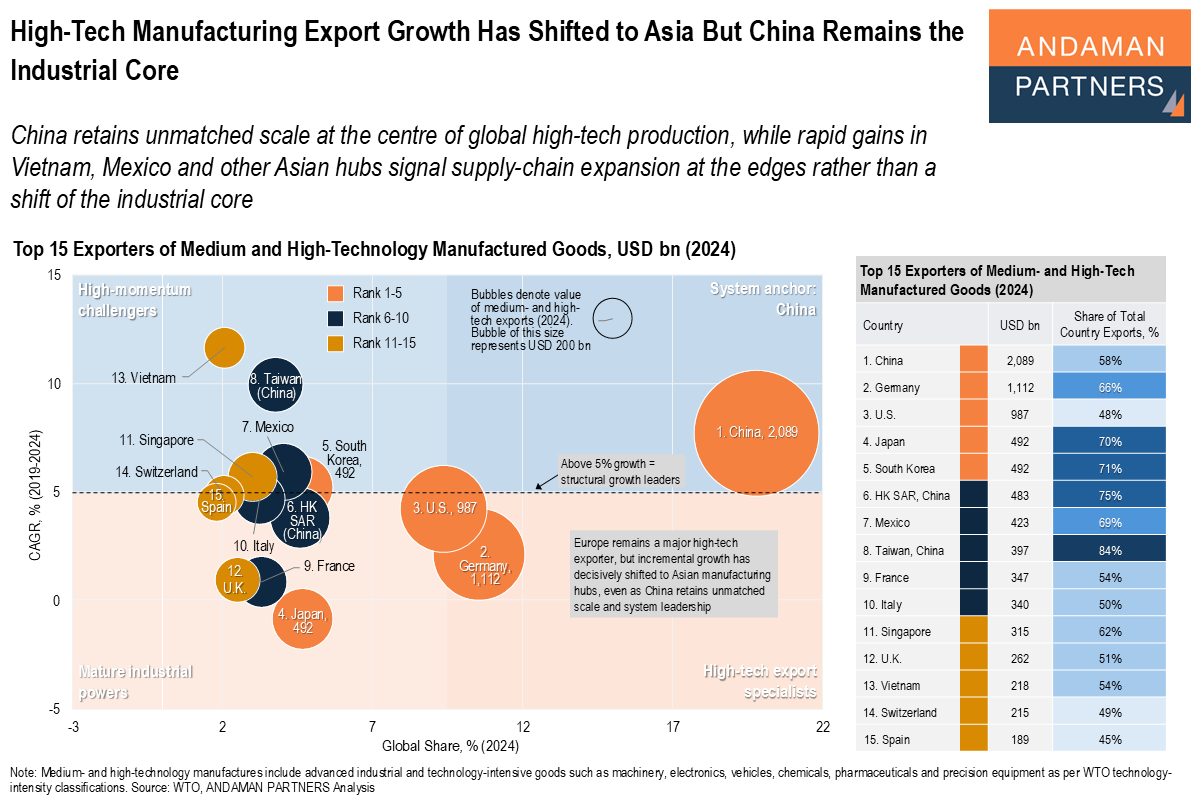

China retains unmatched scale at the centre of global high-tech production, while rapid gains in Vietnam, Mexico and other Asian hubs.

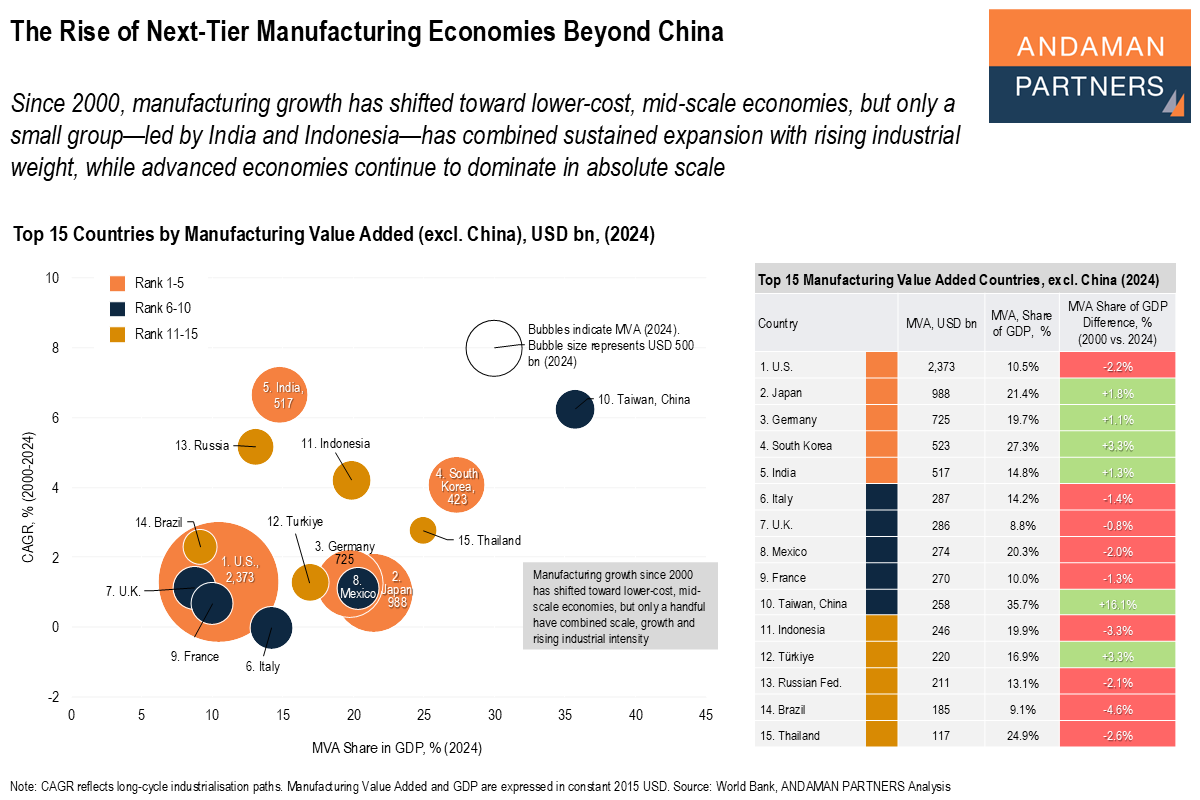

Manufacturing growth shifted toward lower-cost, mid-scale economies, but only a small group has combined sustained expansion with rising industrial weight.

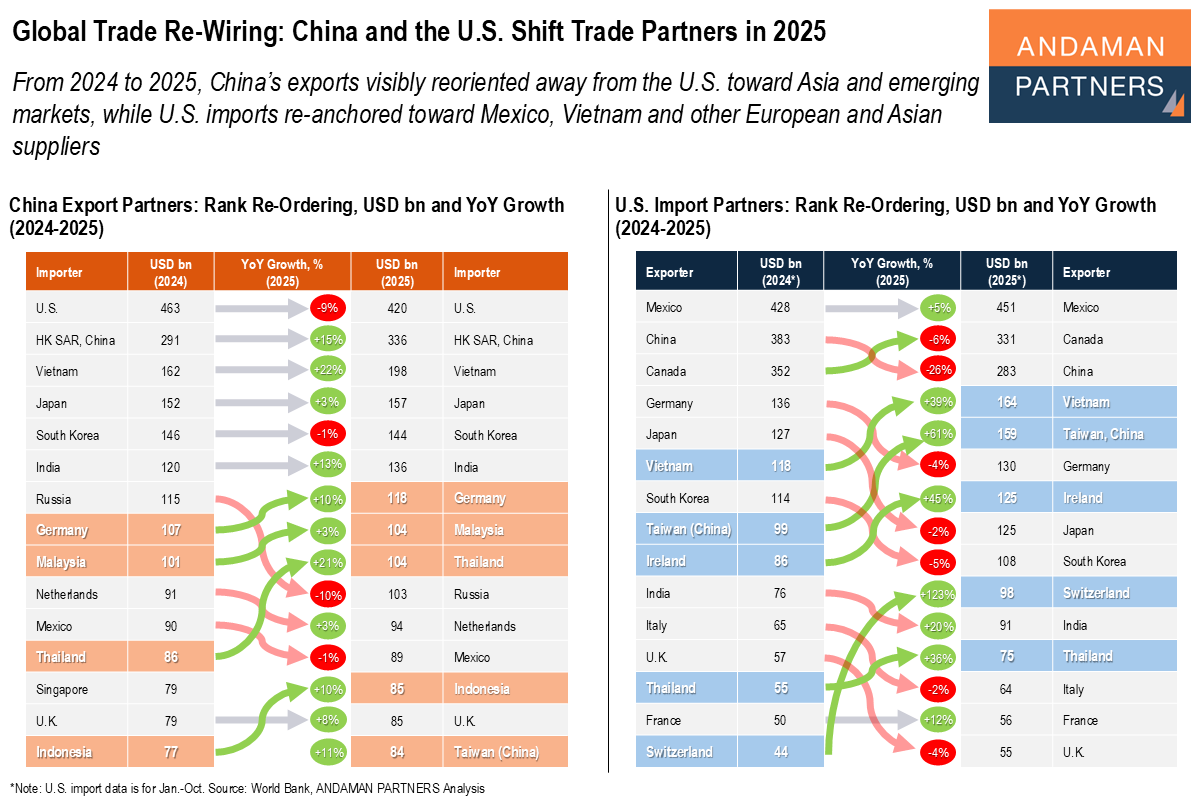

China’s exports reoriented away from the U.S. toward Asia and emerging markets, while U.S. imports re-anchored toward Mexico, Europe and Asia.

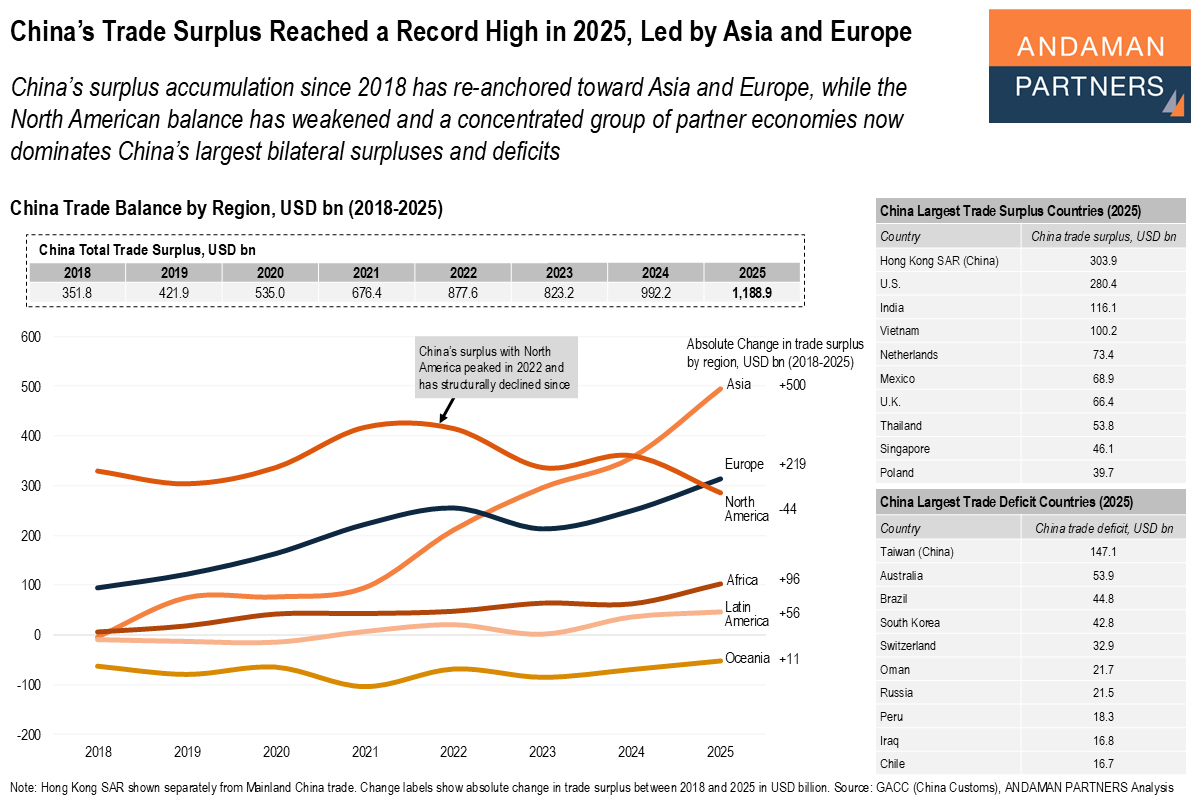

China’s surplus accumulation since 2018 has re-anchored toward Asia and Europe, while the North American balance has weakened.

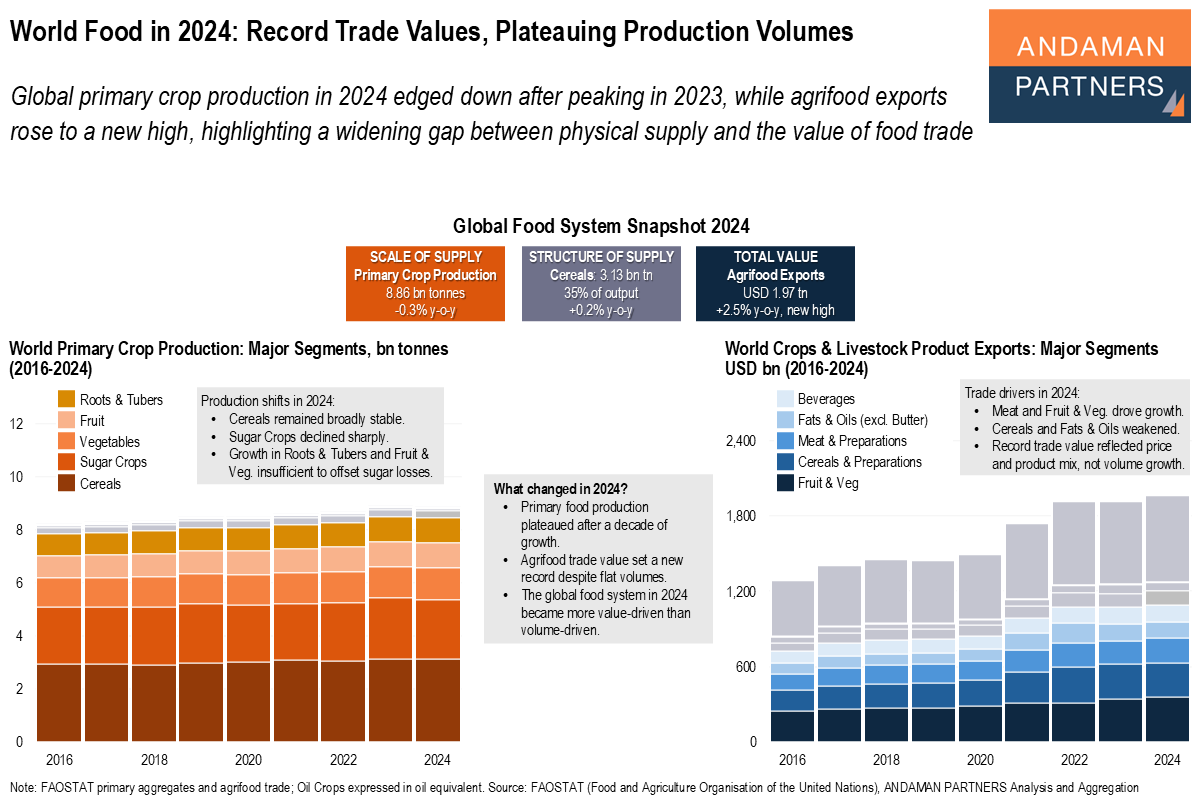

Global primary crop production in 2024 edged down after peaking in 2023, while agrifood exports rose to a new high.

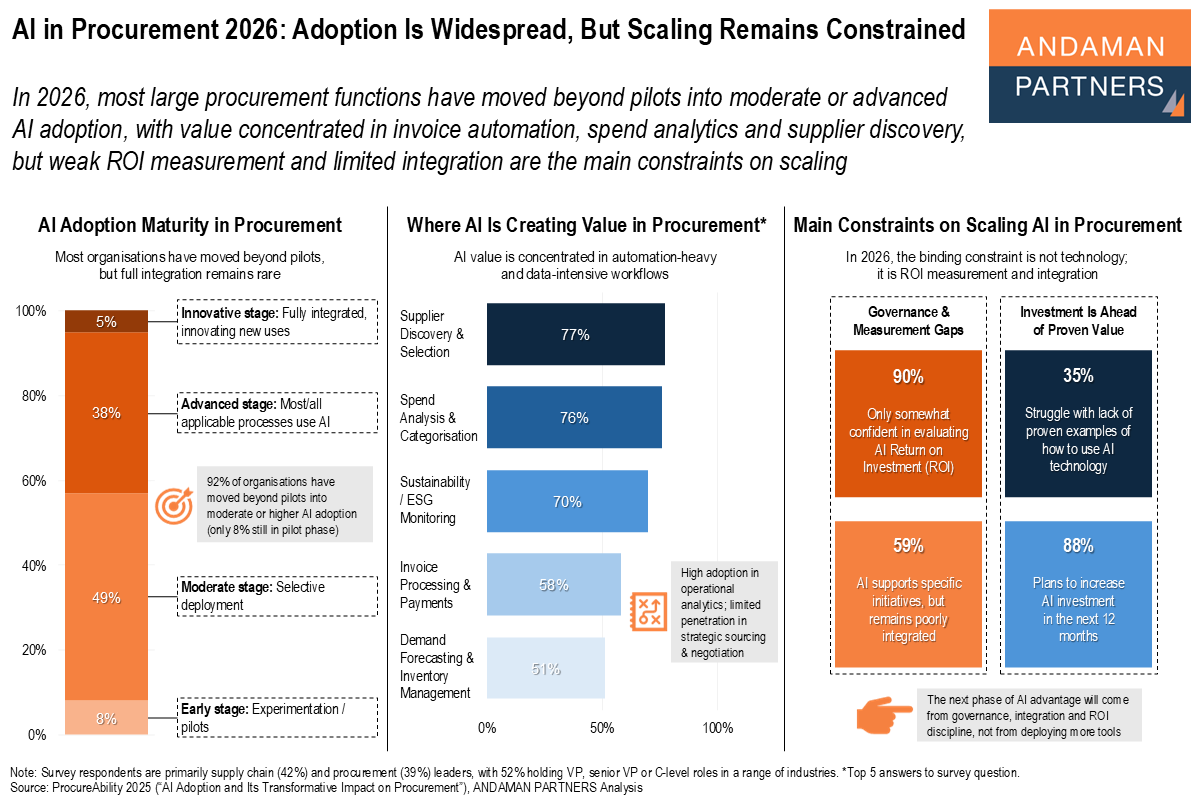

Procurement functions have moved into moderate or advanced AI adoption, but there are still constraints on scaling.

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

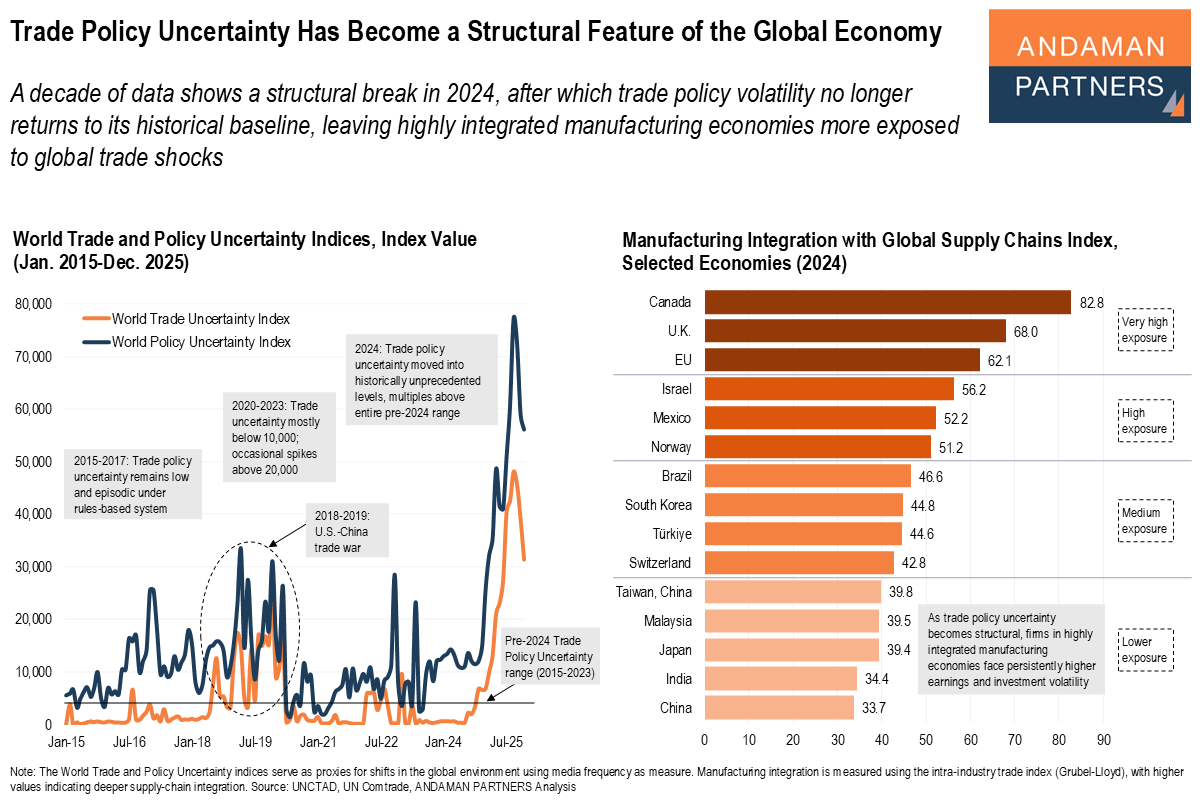

A decade of data shows a structural break in 2024, after which trade policy volatility no longer returns to its historical baseline.