ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

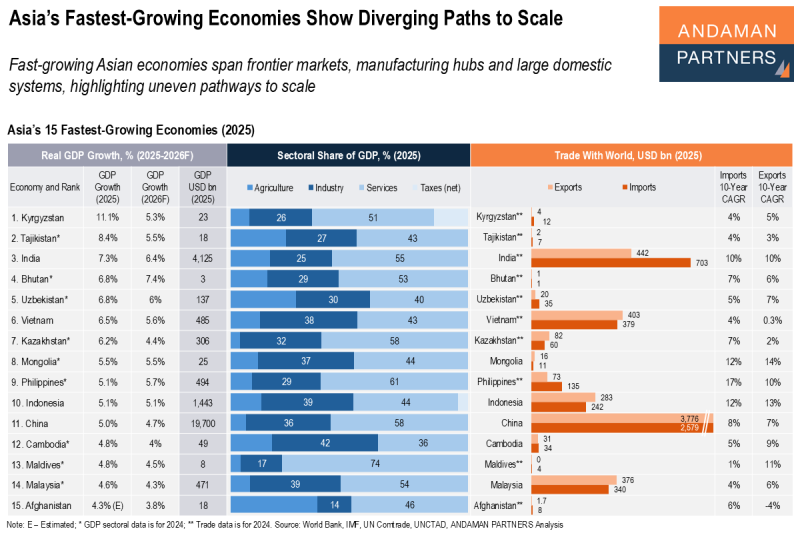

Asia’s Fastest-Growing Economies Show Diverging Paths to Scale

Fast-growing Asian economies span frontier markets, manufacturing hubs and large domestic systems, highlighting uneven pathways to scale.

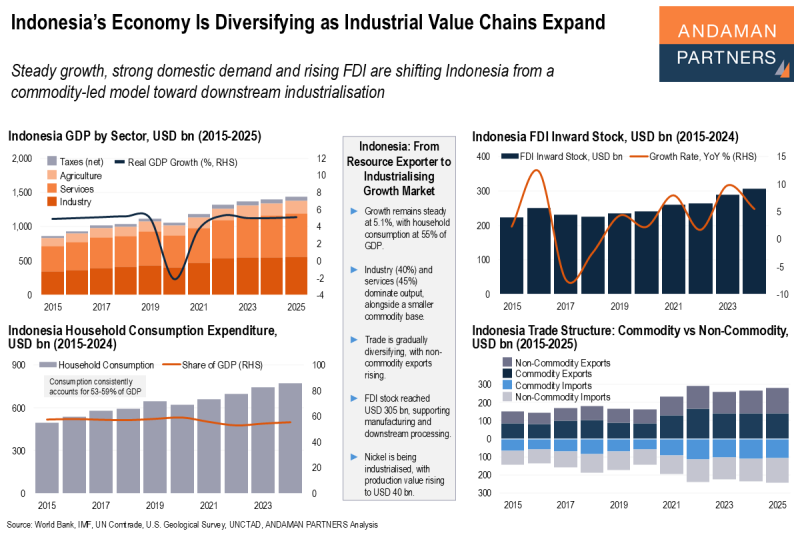

Indonesia’s Economy Is Diversifying as Industrial Value Chains Expand

Steady growth, strong domestic demand and rising FDI are shifting Indonesia from a commodity-led model toward downstream industrialisation.

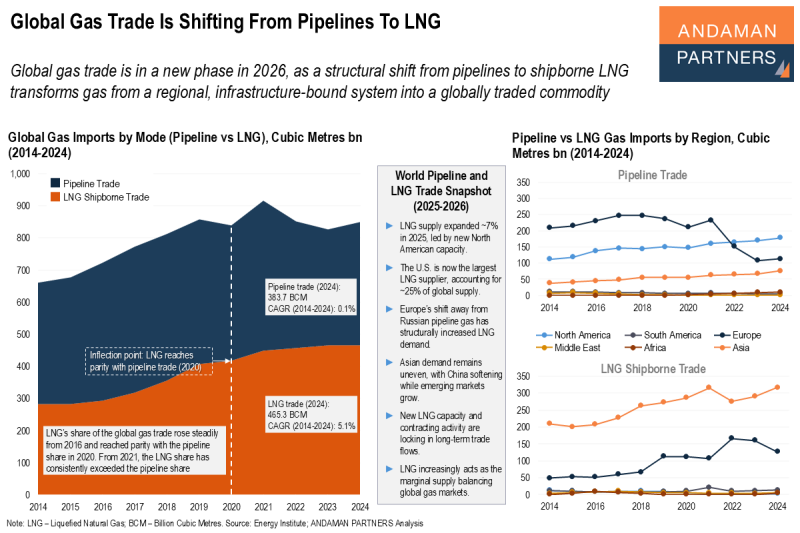

Global Gas Trade Is Shifting from Pipelines to LNG

Global gas trade is in a new phase in 2026 amid a structural shift from pipelines to shipborne LNG.