ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

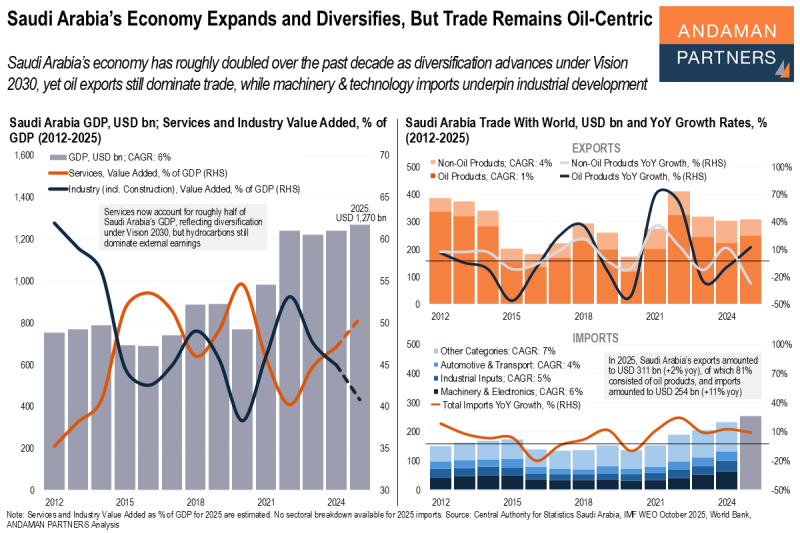

Saudi Arabia’s Economy Expands and Diversifies, But Trade Remains Oil-Centric

Saudi Arabia’s economy has roughly doubled over the past decade, yet oil exports still dominate trade.

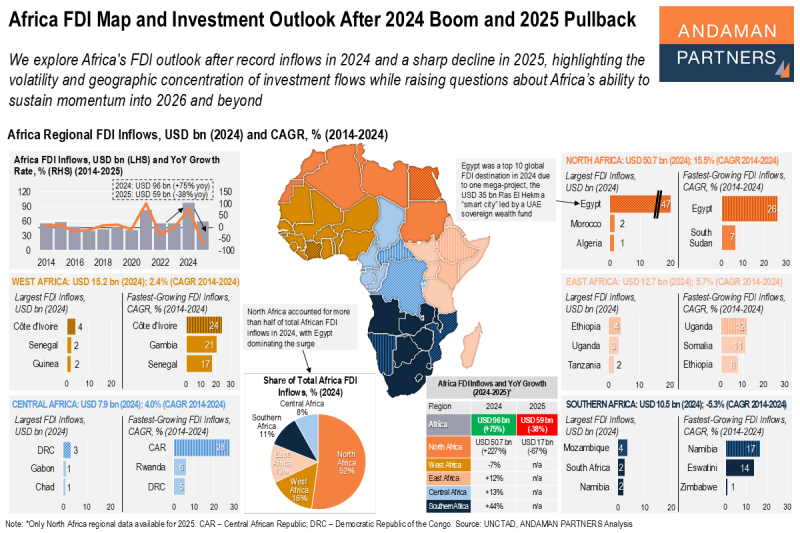

Africa FDI Map and Investment Outlook After 2024 Boom and 2025 Pullback

The volatility and geographic concentration of investment flows raises questions about Africa’s ability to sustain momentum into 2026 and beyond.

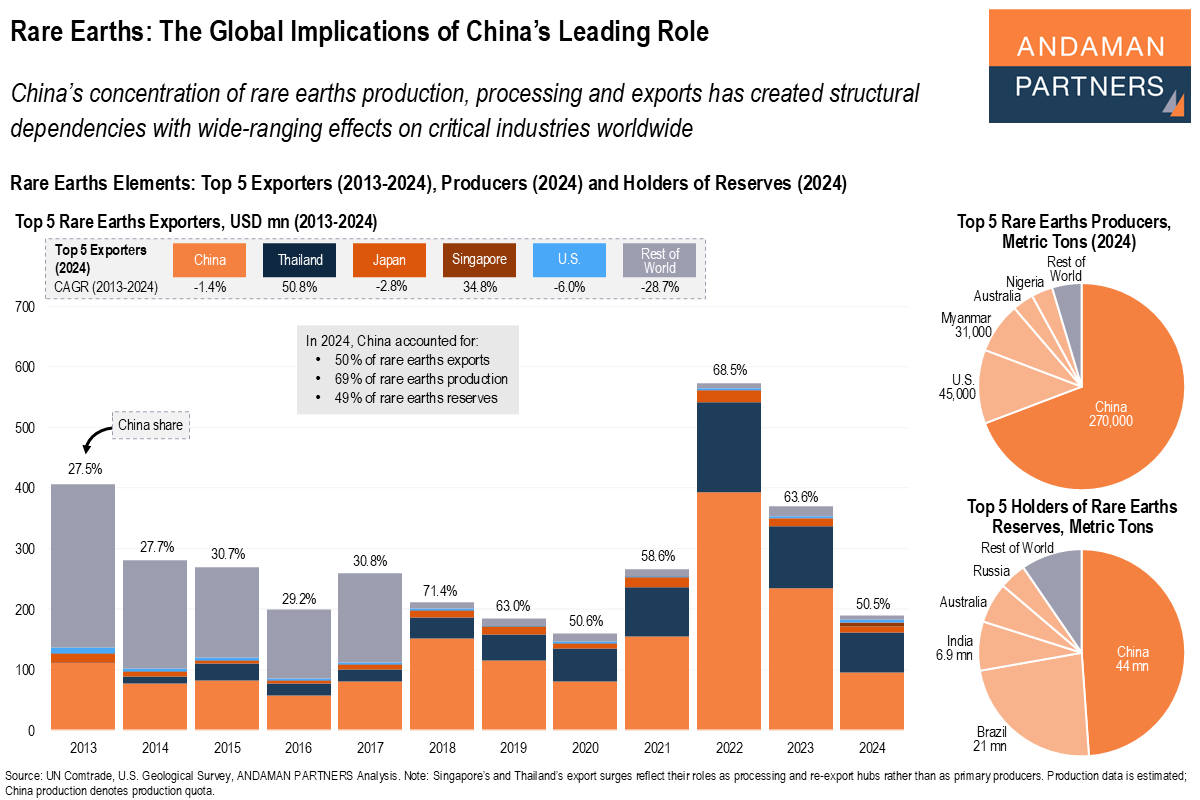

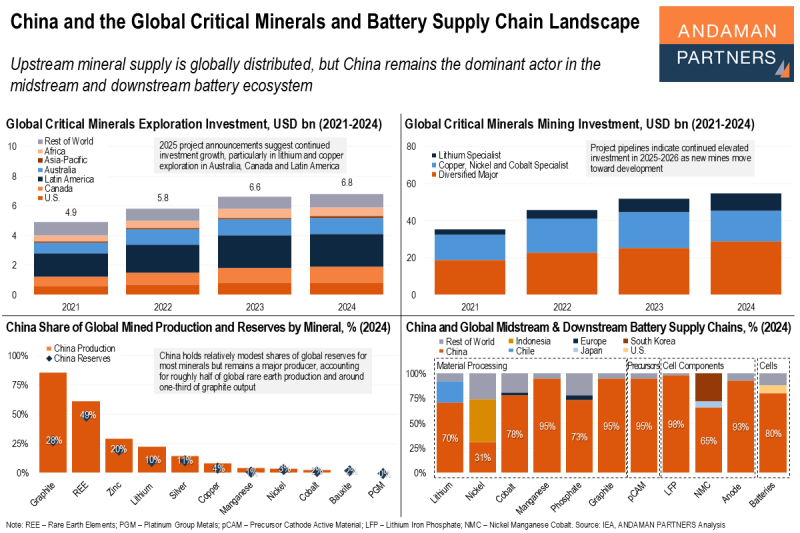

China and the Global Critical Minerals and Battery Supply Chain Landscape

Upstream mineral supply is globally distributed, but China remains the dominant actor in the midstream and downstream battery ecosystem.