ANDAMAN PARTNERS is Hiring: Research Analyst (Brazil)

ANDAMAN PARTNERS is hiring a Research Analyst in Brazil (Full-time; Location Flexible/Virtual).

ANDAMAN PARTNERS Was a Co-Sponsor of the South African National Day Reception in Shanghai on 30 May 2025

ANDAMAN PARTNERS was a cosponsor of the South African National Day Reception in Shanghai on 30 May 2025.

Asia’s Shifting Role in Global Supply Chains — Perspectives by ANDAMAN PARTNERS Co-Founder Rachel Wu

Analysis by ANDAMAN PARTNERS Co-Founder Rachel Wu on changing patterns in global supply chains.

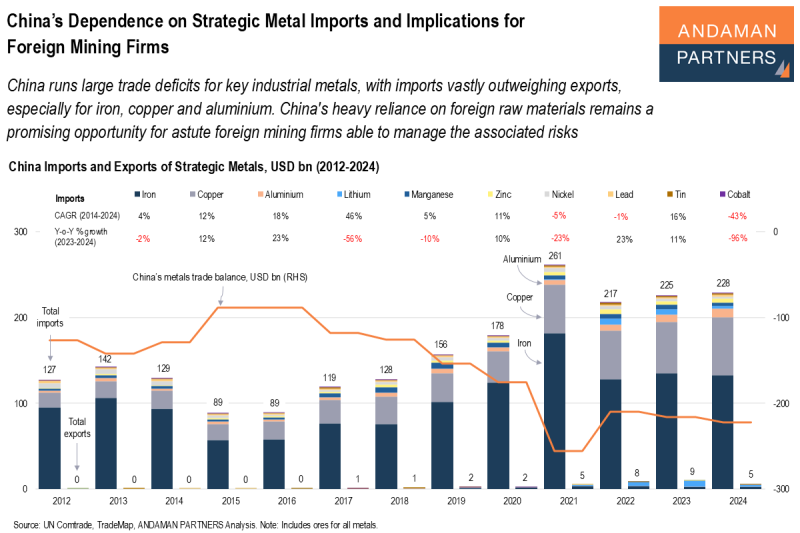

China’s Dependence on Strategic Metal Imports and Implications for Foreign Mining Firms

China runs large trade deficits for key industrial metals, which remains a promising opportunity for astute foreign mining firms.

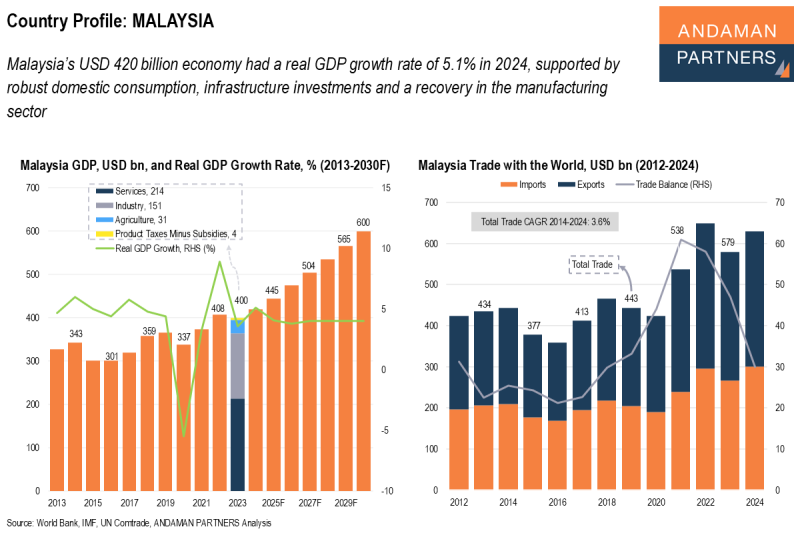

Country Profile – Malaysia

Malaysia has a USD 420 billion economy (2024) and real GDP growth of 5.1%.

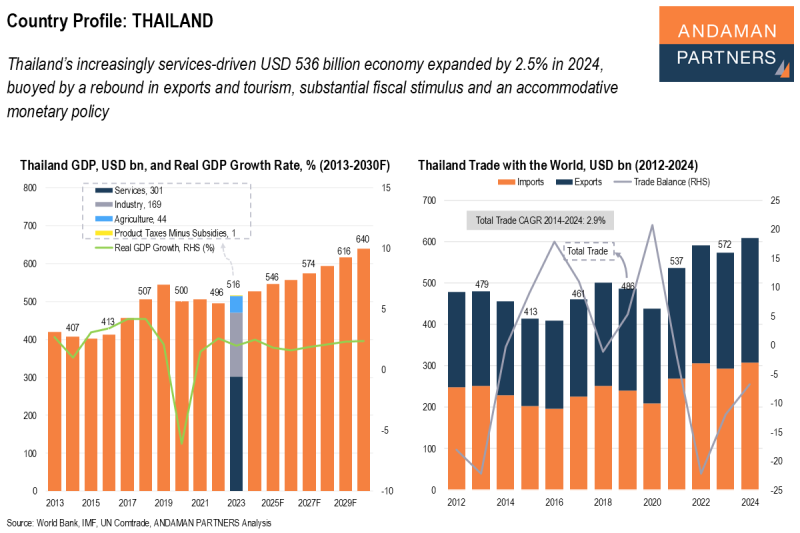

Country Profile – Thailand

Thailand has a USD 536 billion economy (2024) and real GDP growth of 2.5%.