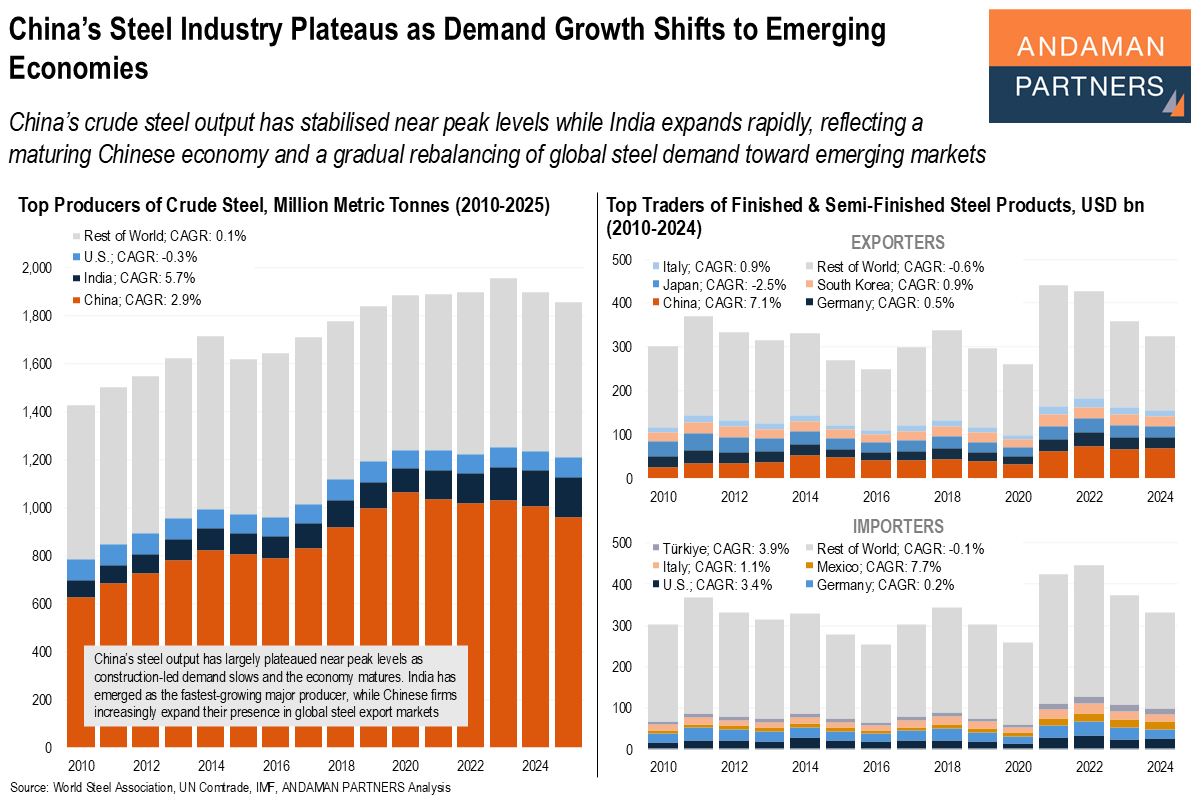

China’s Steel Industry Plateaus as Demand Growth Shifts to Emerging Economies

China’s crude steel output has stabilised near peak levels while India expands rapidly, reflecting a gradual rebalancing of global steel demand.

China’s crude steel output has stabilised near peak levels while India expands rapidly, reflecting a gradual rebalancing of global steel demand.

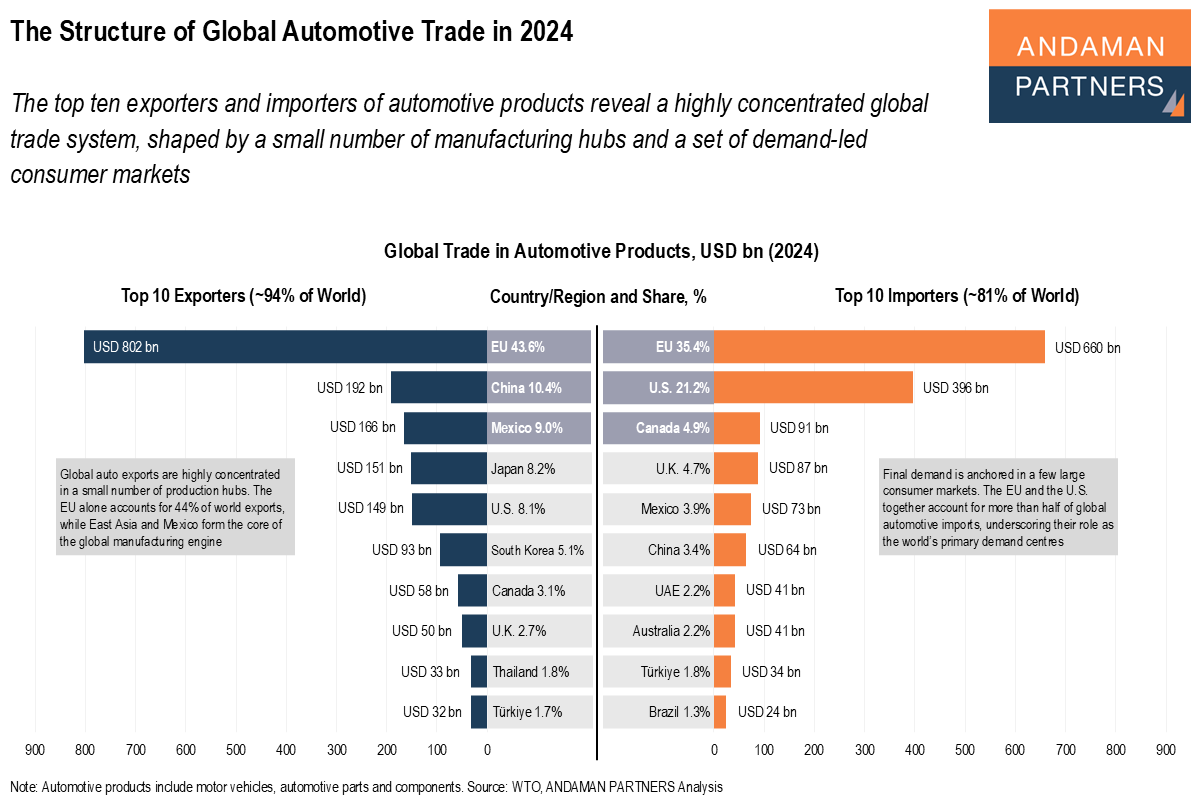

The top ten exporters and importers of automotive products reveal a highly concentrated global trade system.

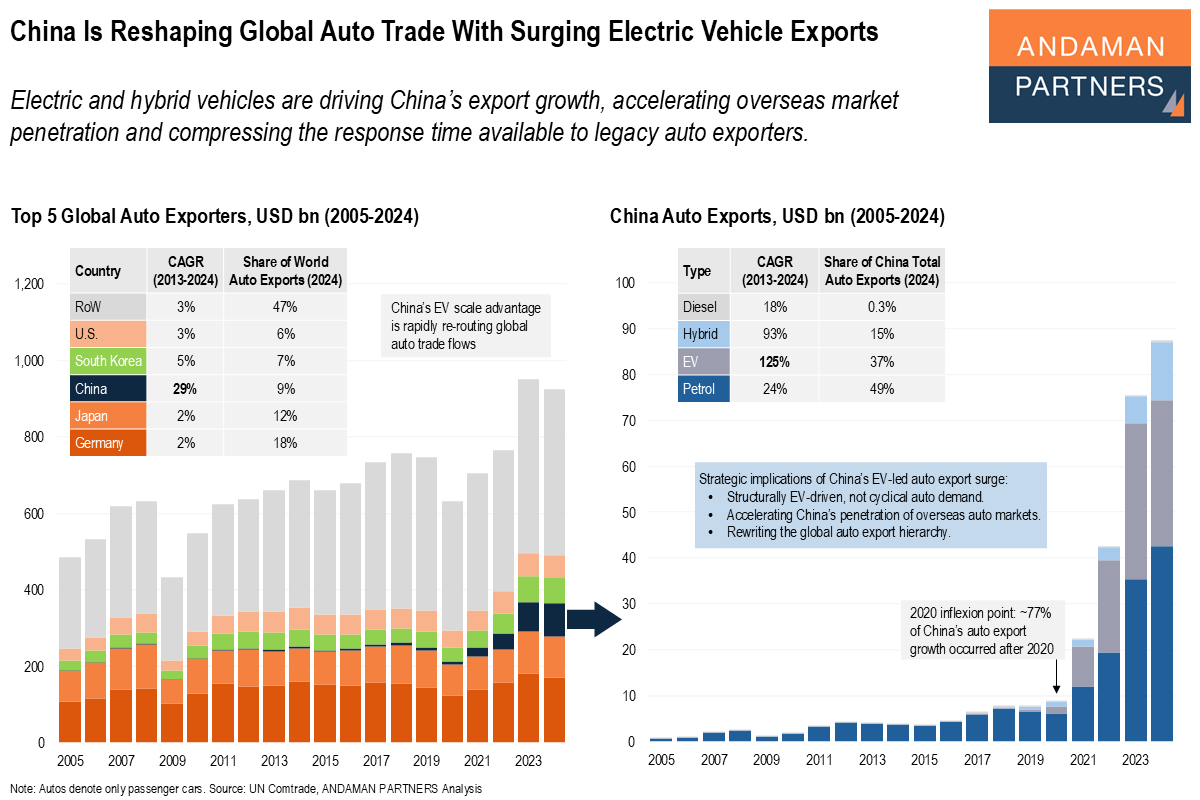

Electric and hybrid vehicles are driving China’s export growth, accelerating overseas market penetration and compressing the response time available to legacy auto exporters.

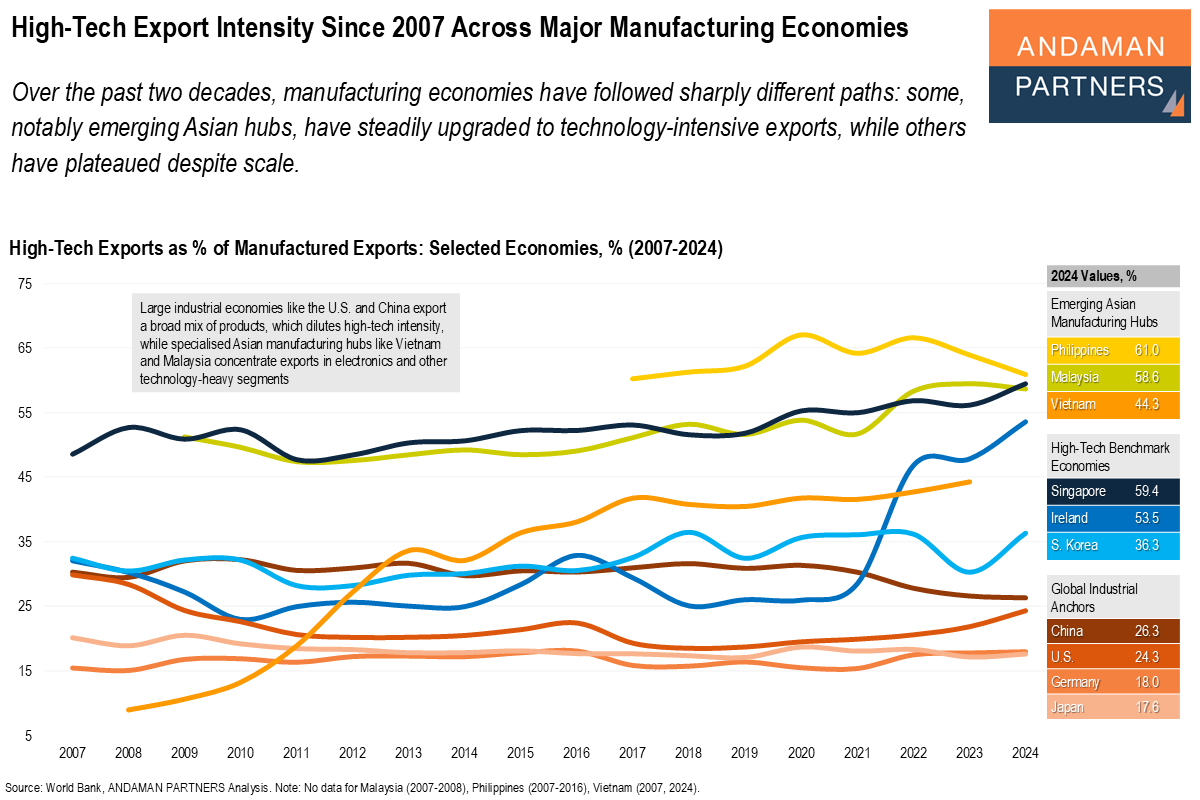

Some manufacturing economies have upgraded to tech-intensive exports while others have plateaued despite scale.

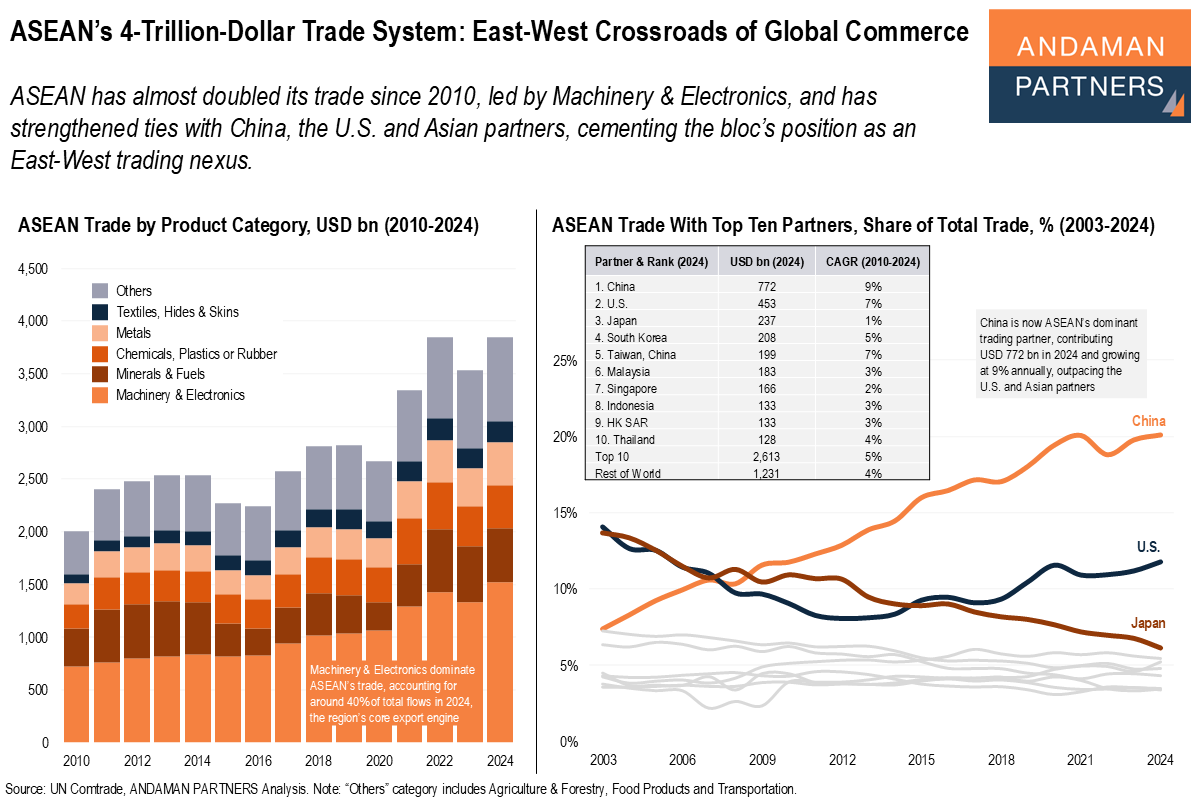

ASEAN has almost doubled its trade since 2010 and has strengthened ties with China and the U.S., cementing the bloc’s position as an East-West trading nexus.

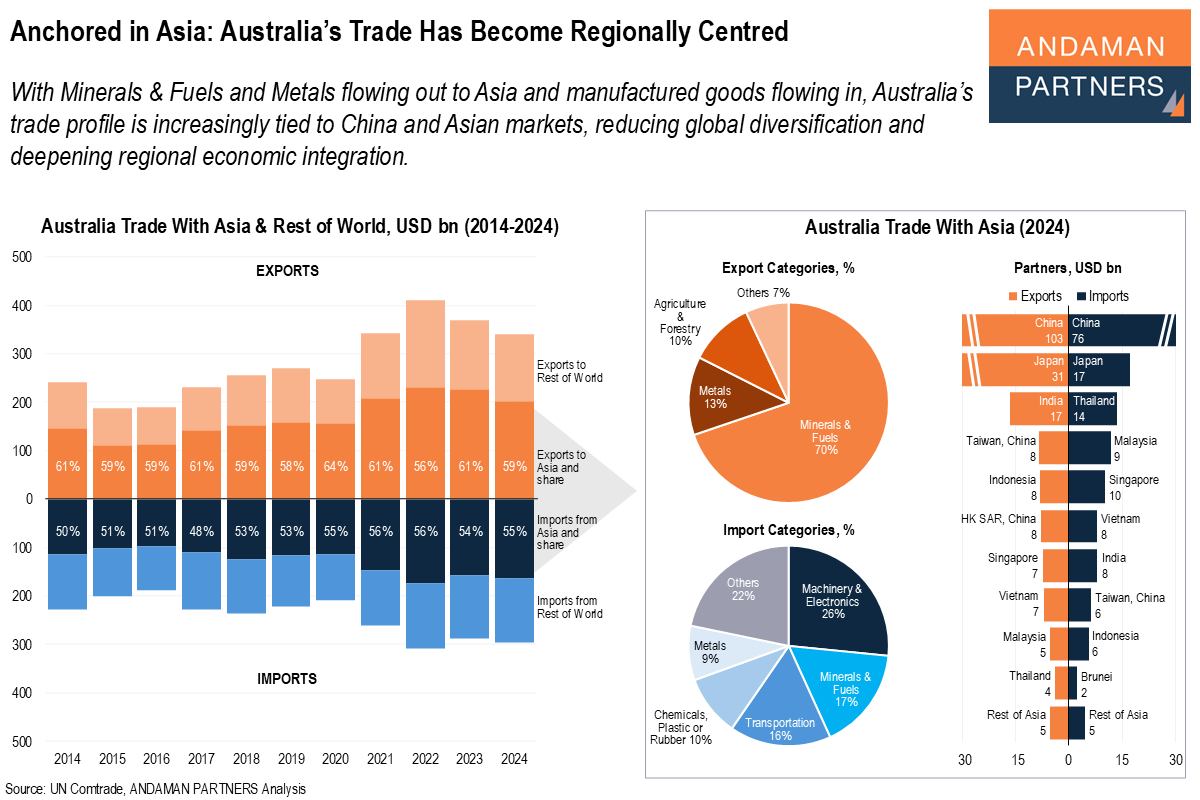

With Minerals & Fuels and Metals flowing out to Asia and manufactured goods flowing in, Australia’s trade profile is increasingly tied to China and Asian markets.

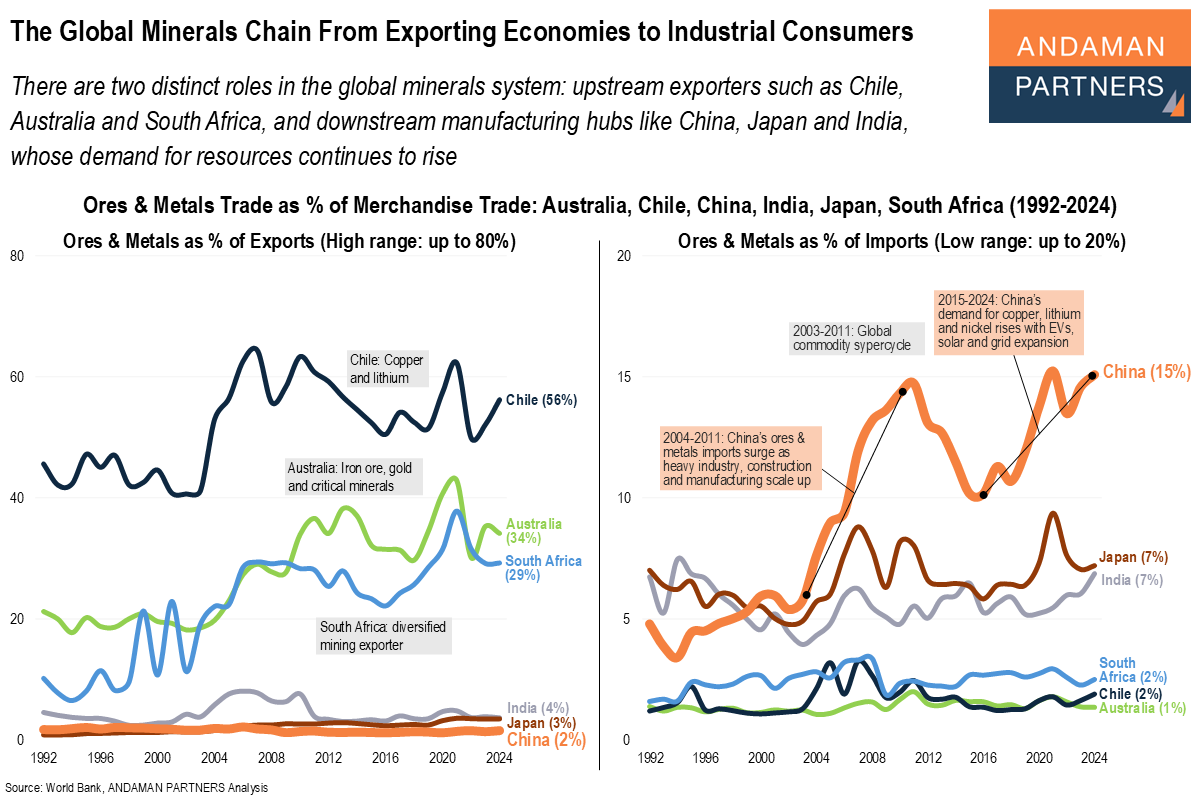

There are two distinct roles in the global minerals system: upstream exporters and downstream manufacturing hubs, whose demand for resources continues to rise.

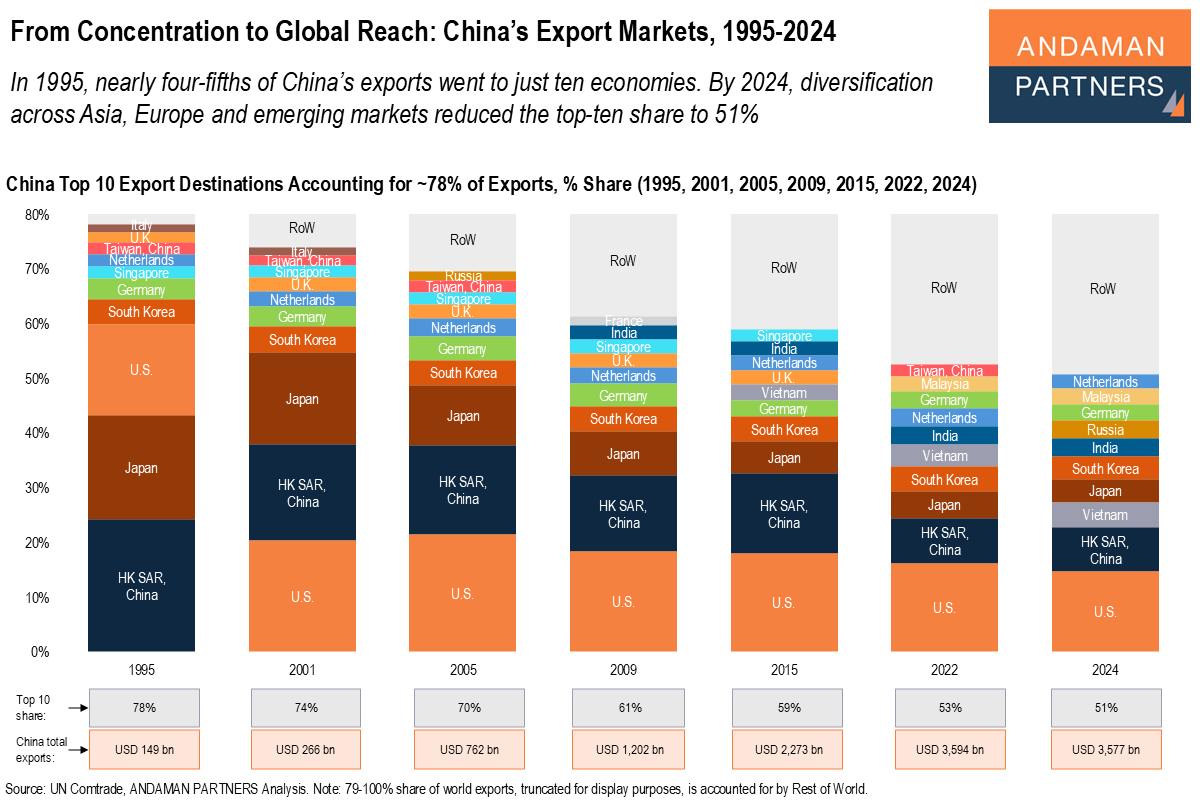

In 1995, nearly four-fifths of China’s exports went to just ten economies. By 2024, the top-ten's share was reduced to 51%.

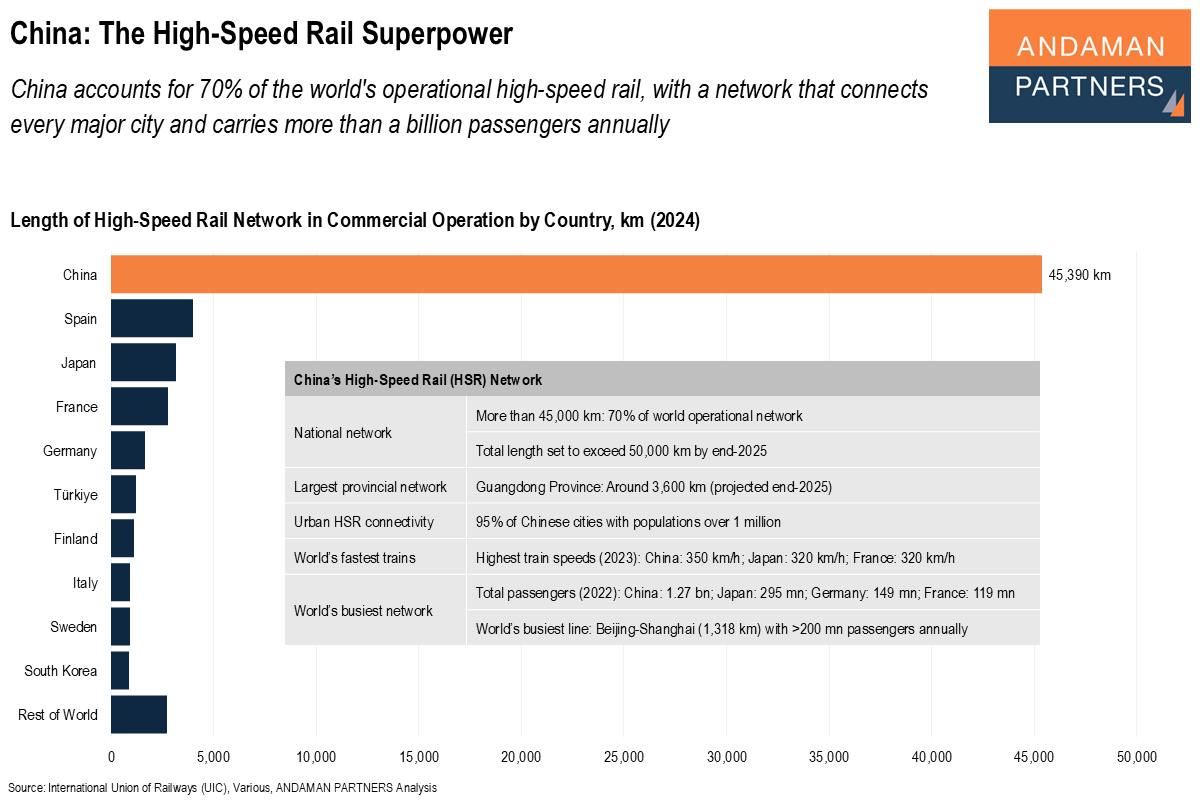

China accounts for 70% of the world's operational high-speed rail, with a network that connects every major city and carries a billion passengers.

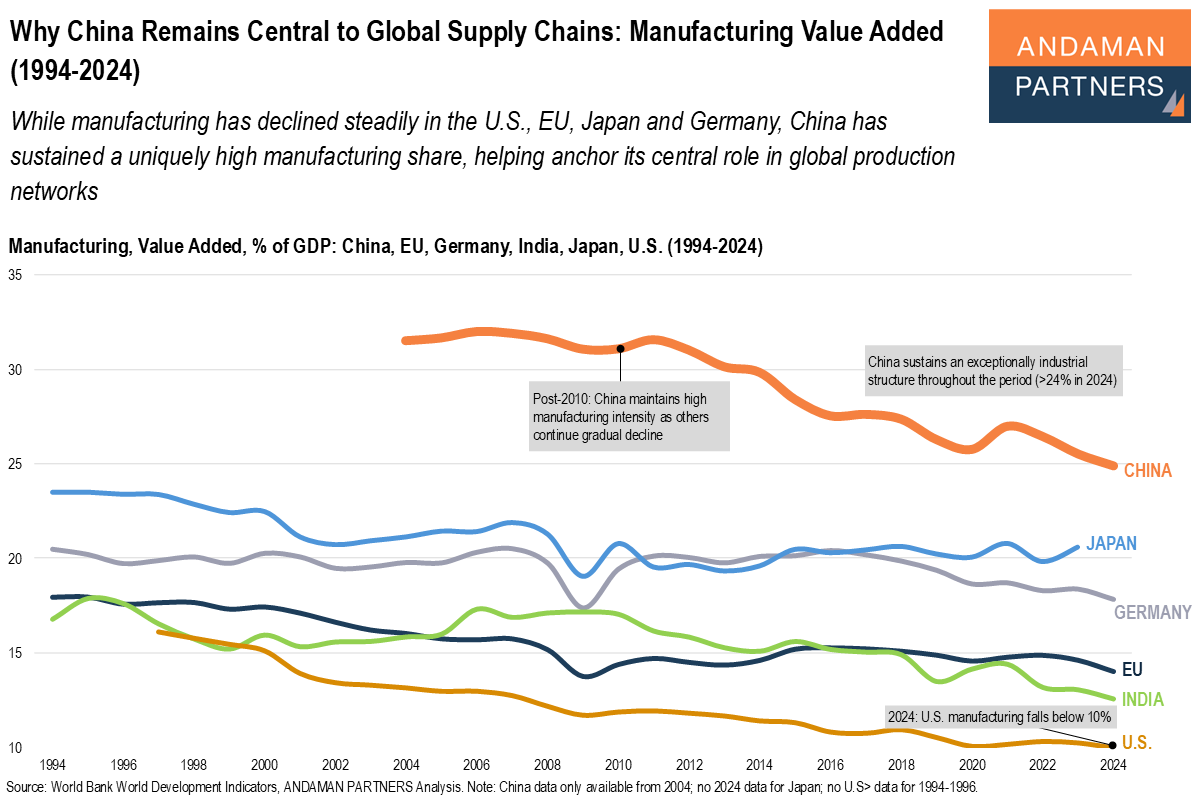

While manufacturing has declined steadily in the U.S., EU, Japan and Germany, China has sustained a uniquely high manufacturing share.