ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

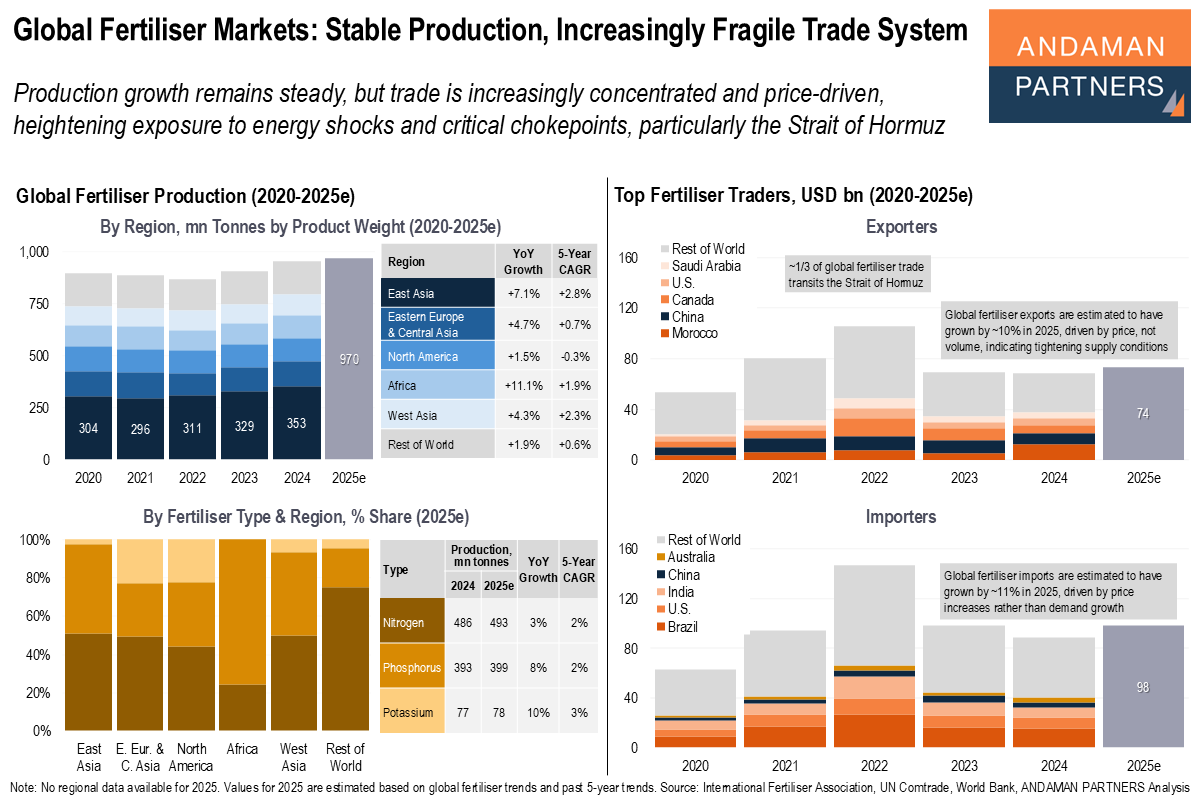

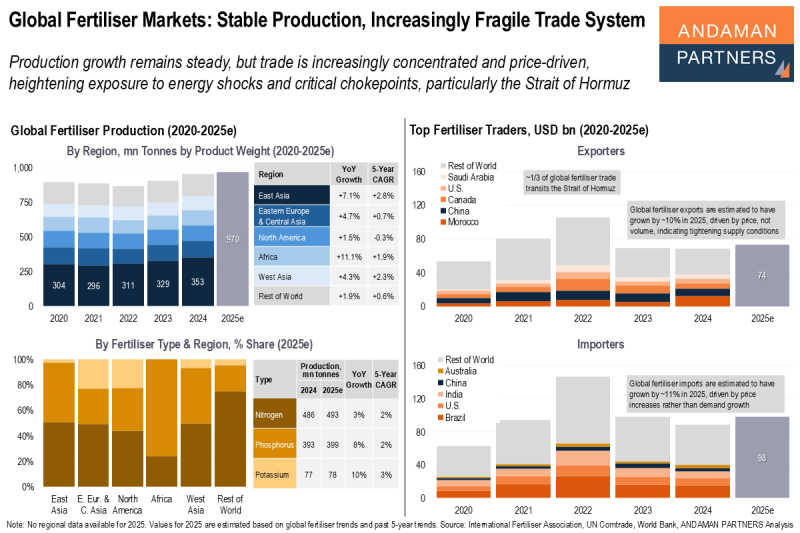

Global Fertiliser Markets: Stable Production, Increasingly Fragile Trade System

Production growth remains steady, but trade is increasingly concentrated and price-driven, heightening exposure to energy shocks and critical chokepoints.

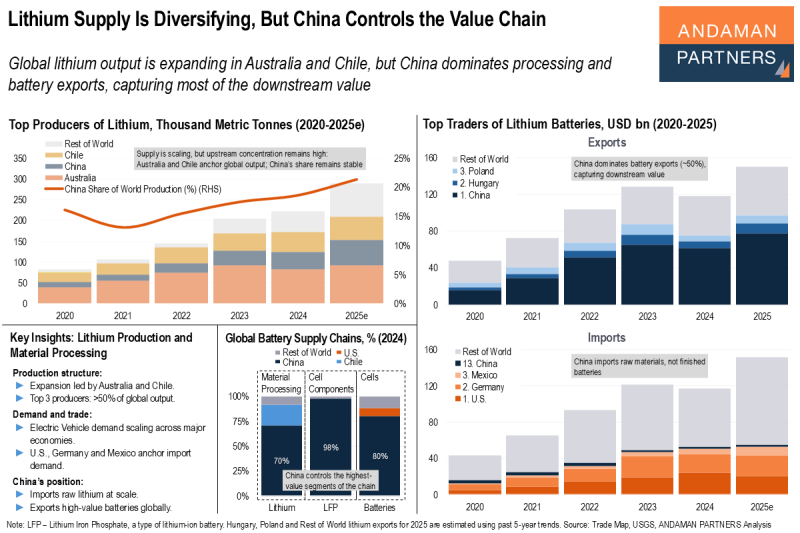

Lithium Supply Is Diversifying, But China Controls the Value Chain

Global lithium output is expanding in Australia and Chile, but China dominates processing and battery exports, capturing most of the downstream value.

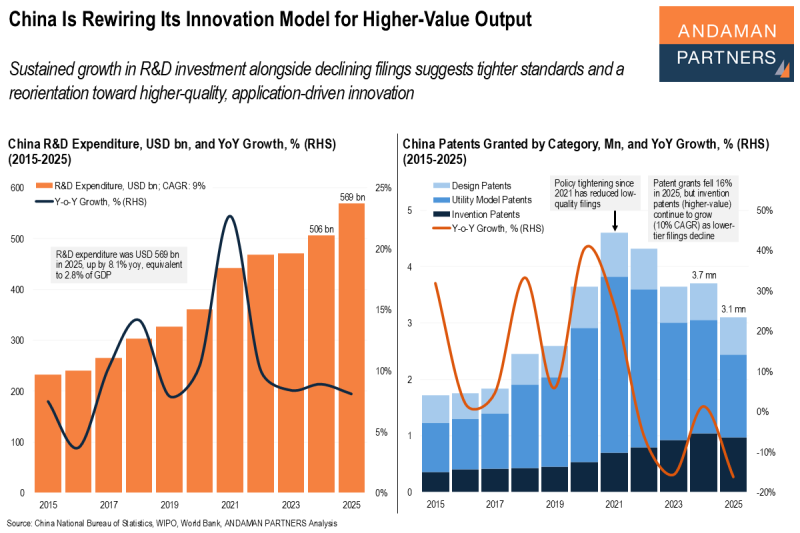

China Is Rewiring Its Innovation Model for Higher-Value Output

Sustained growth in R&D alongside declining filings suggests tighter standards and a reorientation toward higher-quality innovation.