ANDAMAN PARTNERS Wishes You a Happy and Prosperous Year of the Horse!

Compliments of the Chinese Lunar New Year to all our clients, customers, suppliers and partners.

ANDAMAN PARTNERS to Attend Investing in African Mining Indaba 2026 in Cape Town

ANDAMAN PARTNERS Co-Founders Kobus van der Wath and Rachel Wu will attend Investing in African Mining Indaba 2026 in Cape Town, South Africa.

Join ANDAMAN PARTNERS at Networking Event in Cape Town Ahead of Mining Indaba 2026

ANDAMAN PARTNERS is pleased to support and sponsor this popular Pre-Indaba event in Cape Town.

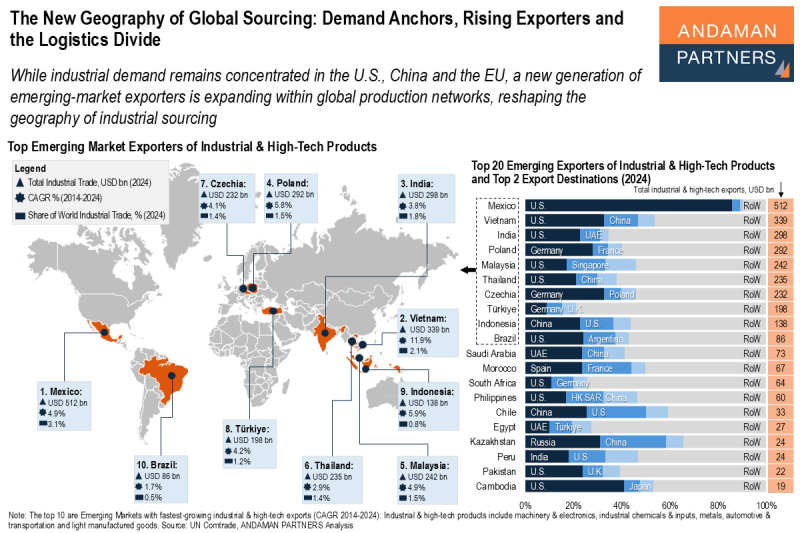

The New Geography of Global Sourcing: Demand Anchors, Rising Exporters and the Logistics Divide

Industrial demand is concentrated in the U.S., China and the EU, while a new generation of emerging markets is expanding in global production.

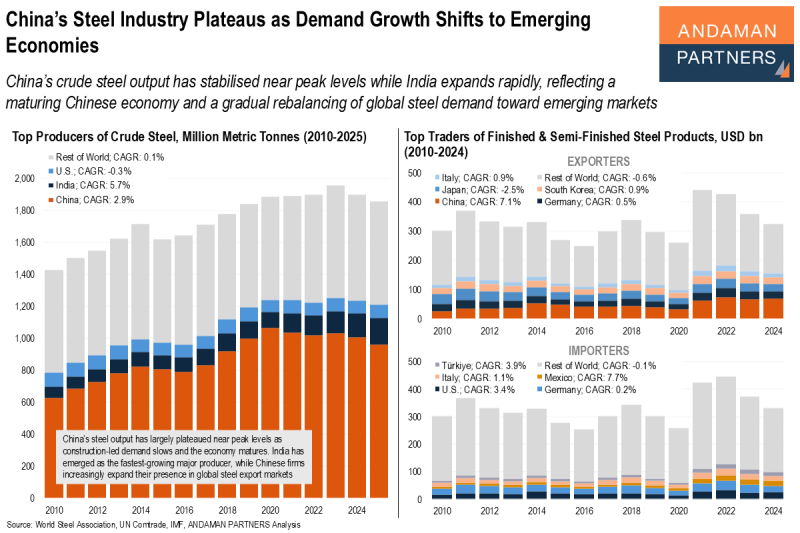

China’s Steel Industry Plateaus as Demand Growth Shifts to Emerging Economies

China’s crude steel output has stabilised near peak levels while India expands rapidly, reflecting a gradual rebalancing of global steel demand.

Supply Chains Are Digitising Rapidly as Automation Becomes the Next Technology Frontier

Surveys show that core digital systems are widely deployed across supply chains, and automation is expected to transform them in coming years.